10 soluciones de pago para comercios seleccionadas para 2026

Mejores Soluciones de Pago para Retail - Lista Corta

Las soluciones de pago para retail son sistemas y plataformas que permiten a tu negocio aceptar y procesar pagos de clientes en tiendas físicas, en línea y en canales móviles. Si estás buscando las mejores soluciones de pago para retail, probablemente te estés enfocando en encontrar herramientas que gestionen transacciones de manera confiable, respalden tus canales de venta y mantengan seguros los datos de tus clientes. Con tantas opciones y tendencias de pago en constante cambio, elegir el sistema adecuado puede impactar desde la rapidez del proceso de pago hasta tu capacidad para gestionar inventario y prevenir fraudes. Esta lista te ayudará a comparar las principales soluciones de pago para retail de 2026, para que puedas seleccionar la mejor opción según las necesidades y planes de crecimiento de tu negocio.

Por Qué Confiar en Nuestras Reseñas de Software

Hemos estado probando y revisando software y servicios de retail y comercio electrónico desde 2021. Como expertos minoristas, sabemos lo crítico y difícil que es tomar la decisión correcta al seleccionar un software. Invertimos en una investigación profunda para ayudar a nuestra audiencia a tomar mejores decisiones de compra de software. Hemos probado más de 2,000 herramientas para diferentes casos de uso en finanzas y contabilidad, y escrito más de 1,000 reseñas completas de software. Descubre cómo mantenemos la transparencia y nuestra metodología de revisión.

Resumen de las Mejores Soluciones de Pago para Retail

Esta tabla comparativa resume los detalles de precios de mis principales selecciones de soluciones de pago para retail, para que encuentres la mejor opción para tu presupuesto y necesidades de negocio.

| Tool | Best For | Trial Info | Price | ||

|---|---|---|---|---|---|

| 1 | Best for unified online and in-store transactions | Not available | From 2.9% + 30¢/transaction | Website | |

| 2 | Best for accepting digital wallets at checkout | Free plan + free demo available | From $0.30/transaction | Website | |

| 3 | Best for multi-location retail management | 14-day free trial + free demo available | From $89/month (billed annually) | Website | |

| 4 | Best for seamless ecommerce integration | 3-day free trial available | From $29/month (billed annually) | Website | |

| 5 | Best for custom gateway integrations | Free consultation available | Pricing upon request | Website | |

| 6 | Best for integrated hardware and software options | Free demo available | Pricing upon request | Website | |

| 7 | Best for extensive fraud detection tools | Not available | From $25/month | Website | |

| 8 | Best for enterprise-grade payment infrastructure | Free demo available | Pricing upon request | Website | |

| 9 | Best for quick setup in physical locations | Free plan available | From $35/month | Website | |

| 10 | Best for transparent interchange-plus pricing | Free demo available | From Interchange + 0.40% + 8¢ (varies by volume) | Website |

Reseñas de Soluciones de Pago para Retail

A continuación encontrarás mis resúmenes detallados de las soluciones de pago para retail que incluí en mi lista corta. Mis reseñas ofrecen una visión profunda de las funciones, integraciones y mejores casos de uso de cada plataforma para ayudarte a elegir la mejor para tu negocio.

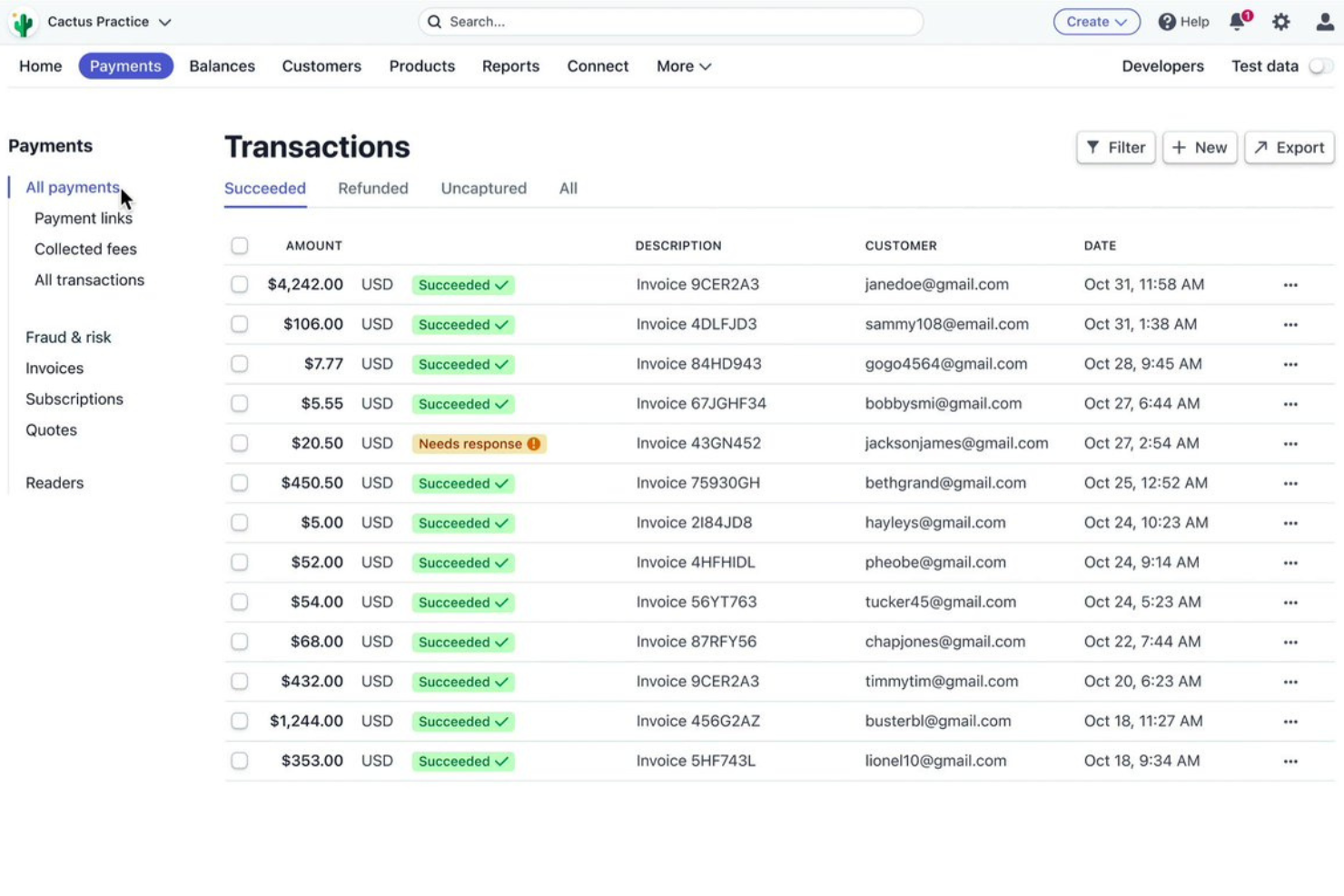

Stripe offers a unified payment platform for retailers who want to manage both online and in-person transactions from a single system. It’s a strong fit for businesses that need flexible payment acceptance across multiple channels and want to simplify reconciliation. Stripe helps retailers handle complex payment flows, including omnichannel sales and integrated reporting.

Why I Picked Stripe

I chose Stripe for its ability to unify online and in-store transactions within a single payment platform. Stripe’s terminal hardware connects directly to its cloud-based system, so you can manage ecommerce and point-of-sale payments together. I find its centralized dashboard especially useful for tracking sales and reconciling payments across channels. The platform also supports advanced payment flows, like buy online, pick up in store, which is important for omnichannel retail operations.

Stripe Key Features

Some other features in Stripe that are useful for retail payment management include:

- Subscription Billing: Set up and manage recurring payments for retail memberships or subscription products.

- Customizable Checkout: Tailor the checkout experience with branding, payment methods, and localized options.

- Integrated Fraud Prevention: Use Stripe Radar to automatically detect and block suspicious transactions.

- Multi-Currency Support: Accept payments in over 135 currencies to serve international customers.

Stripe Integrations

Integrations include Shopify, WooCommerce, BigCommerce, Salesforce, NetSuite, Xero, QuickBooks, HubSpot, Magento, and Lightspeed.

Pros and Cons

Pros:

- Accepts a wide range of payment methods

- Offers advanced fraud detection tools

- Supports unified reporting for online and in-store sales

Cons:

- Dispute resolution process can be slow

- In-person hardware options are limited

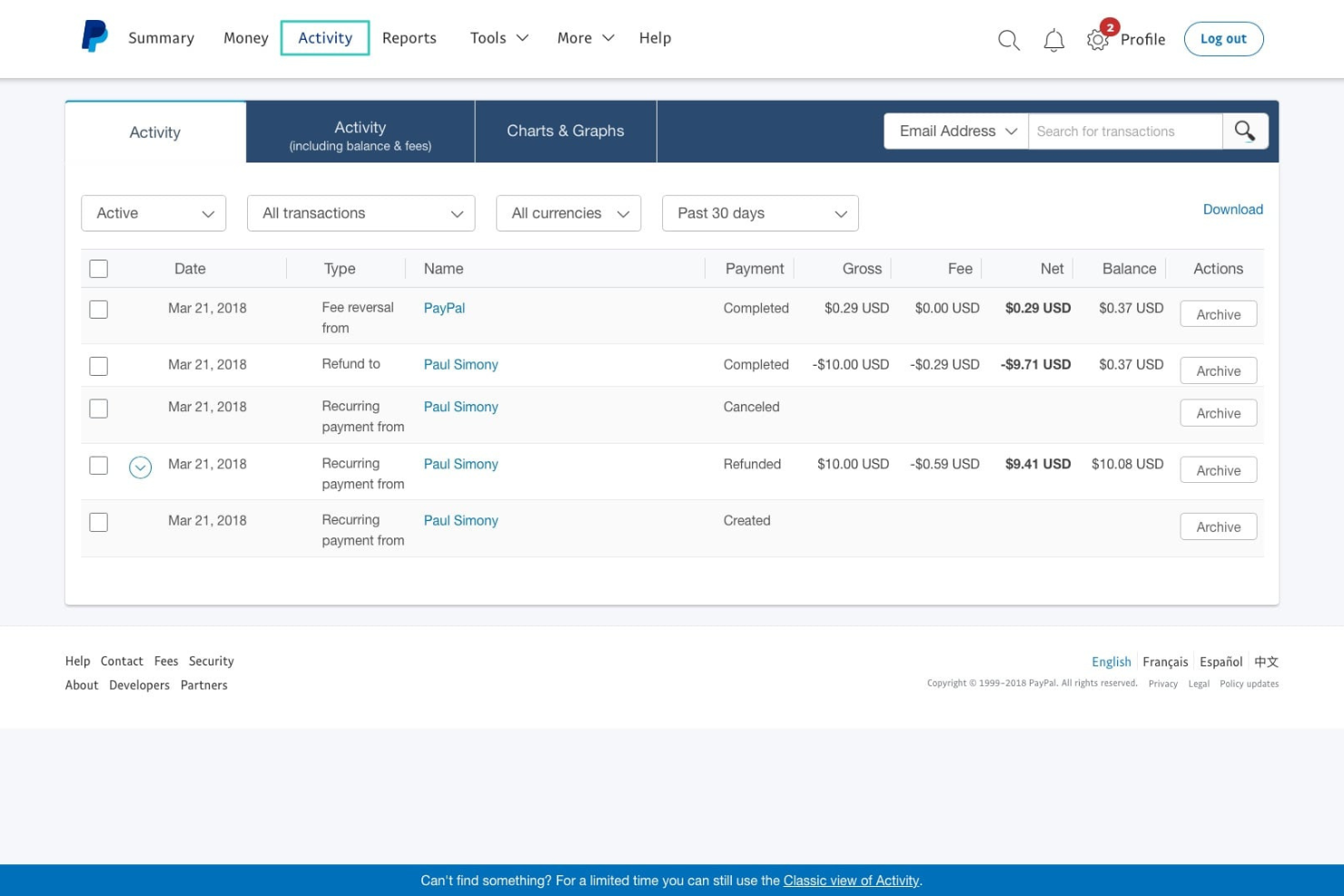

If your business wants to offer customers more ways to pay at checkout, PayPal’s POS system is designed for you. This solution is especially useful for retailers who want to accept digital wallets, contactless payments, and PayPal QR codes in-store. PayPal helps teams capture sales from shoppers who prefer mobile and digital payment methods over traditional cards or cash.

Why I Picked PayPal

PayPal stands out for retailers who want to prioritize digital wallet acceptance at checkout. I picked PayPal because it lets businesses accept a wide range of payment types, including PayPal, Venmo, Apple Pay, Google Pay, and contactless cards, all through one POS system. The platform also supports QR code payments, which can speed up in-person transactions and appeal to mobile-first shoppers. For retailers looking to capture sales from customers who prefer digital and mobile payments, PayPal offers a flexible and widely recognized solution.

PayPal Key Features

Some other features that make PayPal a strong option for retail payment solutions include:

- Multi-User Access: Allows multiple staff members to use the POS system with individual logins.

- Inventory Tracking: Lets you monitor stock levels and update inventory in real time.

- Sales Reporting Dashboard: Provides detailed sales analytics and transaction history within the platform.

- Integration With PayPal Working Capital: Offers access to business financing directly through your PayPal account.

PayPal Integrations

Integrations include QuickBooks, Shopify, WooCommerce, BigCommerce, Lightspeed, Xero, Revel Systems, Vend, Adobe Commerce, and Wix.

Pros and Cons

Pros:

- Integrates with major ecommerce and accounting platforms

- Includes built-in inventory management tools

- Offers instant access to received funds

Cons:

- Limited advanced POS hardware options available

- Chargeback process can favor buyers over sellers

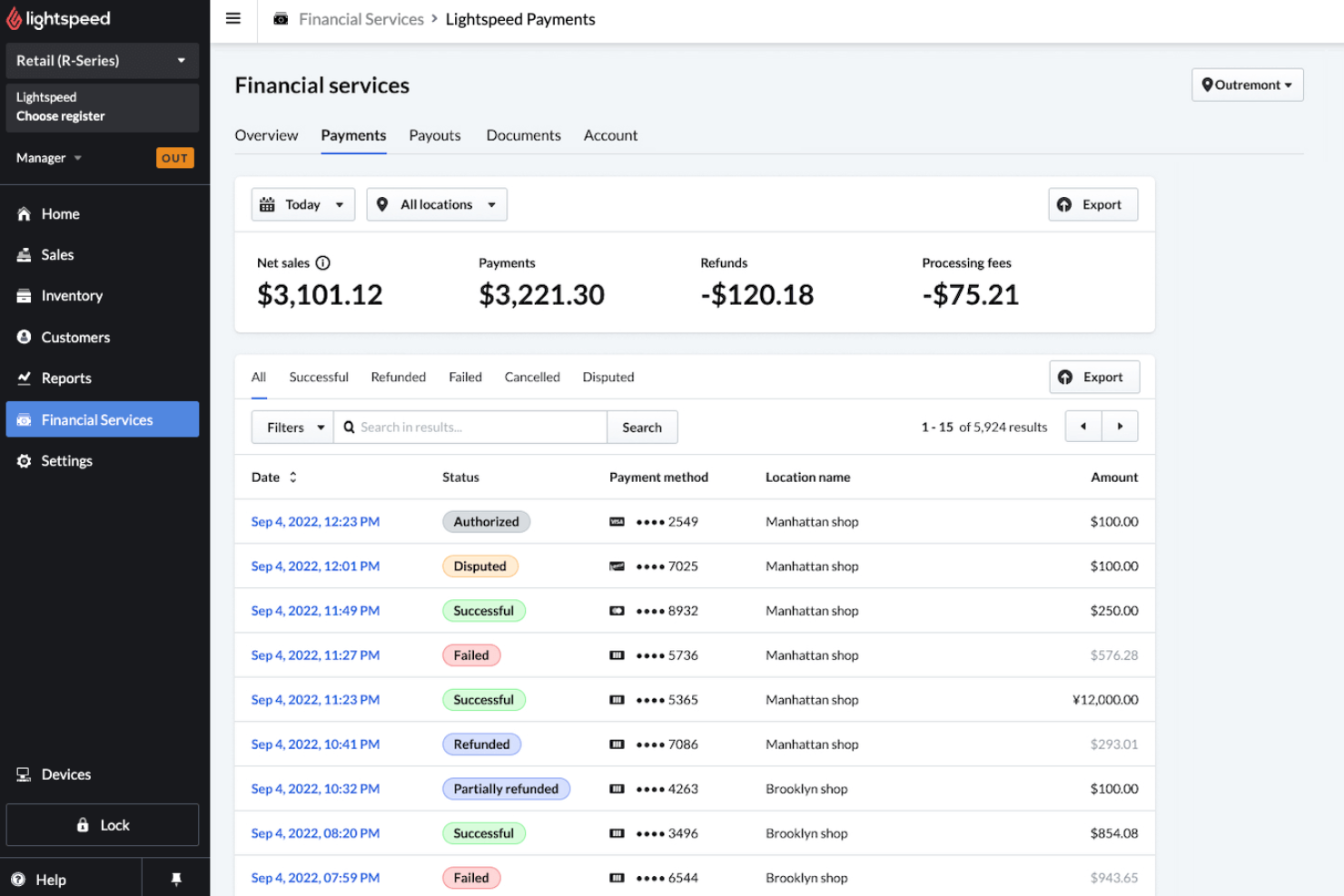

Lightspeed is built for retailers who need to manage multiple locations from a single platform. It’s especially useful for businesses juggling inventory, sales, and reporting across several stores or channels. With Lightspeed, you can centralize operations, standardize processes, and keep a close eye on performance at every site.

Why I Picked Lightspeed

Managing payments across several retail locations can get complicated, which is why I picked Lightspeed for multi-location retail management. Lightspeed lets you track inventory, sales, and customer data in real time across all your stores from a single dashboard. You can set up location-specific tax rules and payment workflows, making it easier to stay compliant and consistent. This centralized approach helps retailers maintain control and visibility, even as their business grows to new sites.

Lightspeed Key Features

Some other features that caught my attention include:

- Integrated Payment Processing: Accepts credit, debit, and contactless payments directly through the POS.

- Customizable Receipts: Lets you tailor printed or digital receipts with your branding and messaging.

- Employee Permissions: Allows you to set user roles and control access to sensitive payment functions.

- Gift Card Management: Issues, tracks, and redeems gift cards across all store locations.

Lightspeed Integrations

Integrations include QuickBooks, Xero, Shopify, BigCommerce, Mailchimp, Klaviyo, Deputy, 7shifts, WooCommerce, and Local Inventory on Google.

Pros and Cons

Pros:

- Provides customizable receipt options

- Integrates with major ecommerce platforms

- Offers built-in gift card management

Cons:

- Payment processing requires Lightspeed Payments

- Hardware compatibility can be restrictive

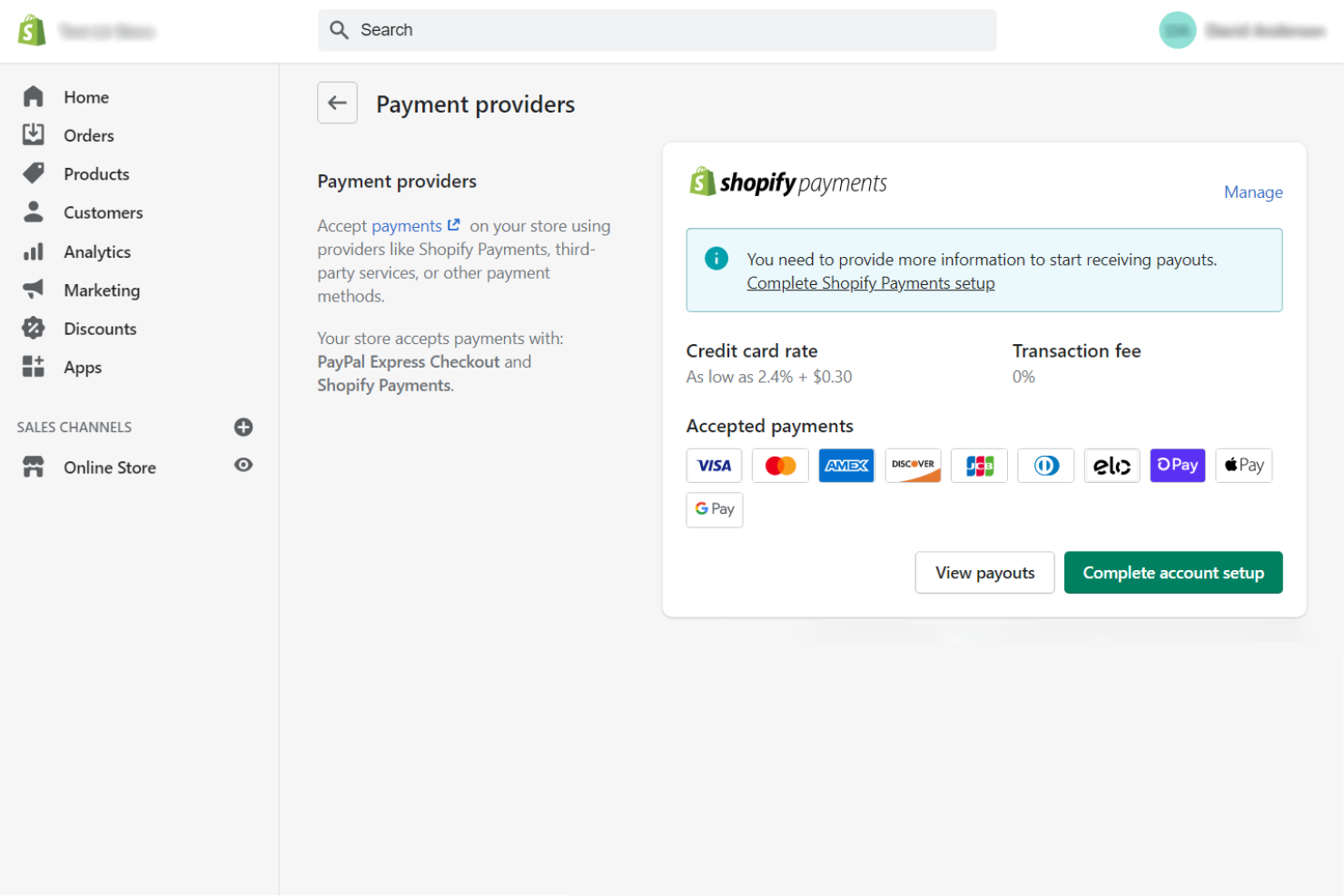

Shopify Payments is built directly into the Shopify platform, making it a natural choice for ecommerce retailers who want to manage payments and storefronts in one place. This solution appeals to teams looking to reduce friction between their online store and payment processing. With Shopify Payments, you can avoid third-party gateways and keep all transaction data within your Shopify dashboard.

Why I Picked Shopify Payments

Shopify Payments stands out for retailers who want payment processing that’s fully embedded within their ecommerce platform. I picked Shopify Payments because it eliminates the need for third-party gateways, so you can manage orders, payments, and refunds directly from your Shopify admin. The system automatically syncs transaction data with your store’s sales and inventory, which helps reduce manual reconciliation. For businesses focused on online sales, this level of integration keeps operations simple and minimizes the risk of errors between systems.

Shopify Payments Key Features

Some other features worth noting include:

- Chargeback Management: Provides built-in tools to track, respond to, and manage chargebacks directly from your Shopify dashboard.

- Multi-Currency Support: Lets you accept payments in multiple currencies, displaying prices and processing transactions in your customer’s local currency.

- Integrated Fraud Analysis: Uses automated risk assessment tools to flag suspicious orders before you capture payment.

- Instant Payouts: Offers the option to receive funds from sales within minutes using eligible bank accounts.

Shopify Payments Integrations

Integrations include Shop Pay, Shopify POS, Shopify Fulfillment Network, Shopify Flow, Shopify Inbox, Shopify Email, Shopify Shipping, Shopify Plus, Shopify App Store, and Shop.

Pros and Cons

Pros:

- Integrated fraud analysis on every transaction

- Multi-currency support for global selling

- Instant payouts available for eligible accounts

Cons:

- Cannot be used on non-Shopify websites

- Account holds can occur without warning

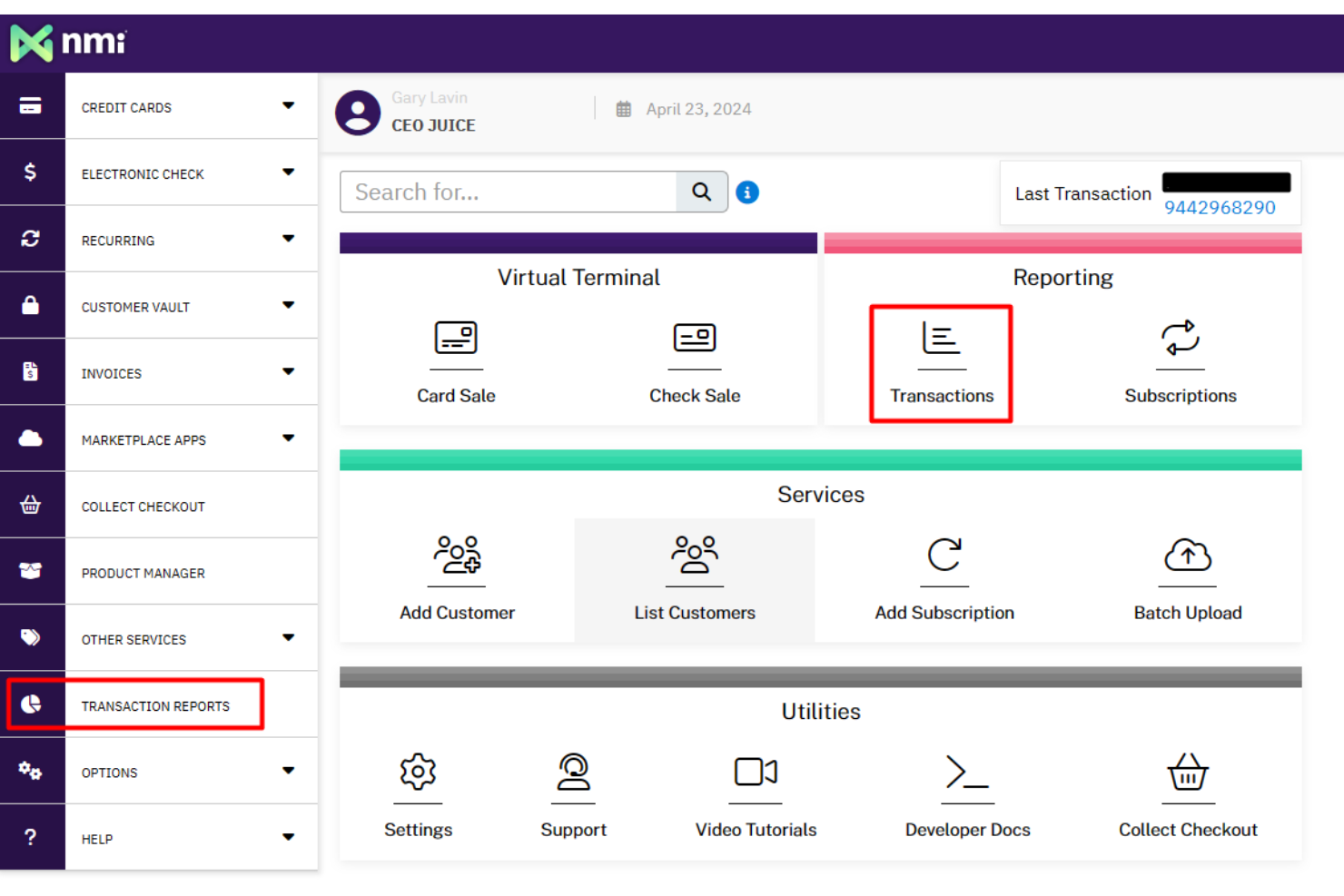

NMI is designed for retailers and technology providers who need flexible, custom payment gateway integrations. It’s a strong fit for businesses with complex payment environments or those looking to unify in-store, online, and mobile transactions under one platform. With NMI, you can connect to a wide range of processors and hardware, making it easier to tailor payment workflows to your specific needs.

Why I Picked NMI

When retailers need to connect multiple payment processors or hardware devices, NMI stands out for its custom gateway integrations. I picked NMI because it lets you build tailored payment experiences by supporting a wide range of terminals, shopping carts, and processor connections. The platform also offers advanced developer tools and APIs, so you can create unique checkout flows or embed payments into your own applications. This flexibility is especially valuable for businesses with complex or evolving payment requirements.

NMI Key Features

Some other features worth noting include:

- Tokenization and Vaulting: Secures customer payment data for recurring transactions and future purchases.

- Omnichannel Payment Support: Accepts payments across in-store, online, and mobile channels.

- Fraud Prevention Tools: Includes customizable rules and monitoring to help detect and prevent fraudulent transactions.

- White-Label Capabilities: Lets you brand the payment experience with your own logo and colors.

NMI Integrations

Native integrations are not currently listed. An API is available for custom integrations.

Pros and Cons

Pros:

- Omnichannel support for unified payments

- Advanced fraud detection and security tools

- White-labeling for branded payment experiences

Cons:

- Requires technical resources for full setup

- Native integrations are not clearly listed

If your retail business needs payment solutions that combine both hardware and software, NCR Voyix is built for you. This platform is a strong fit for retailers looking to unify their point-of-sale devices, payment processing, and back-end management under one provider. NCR Voyix helps teams simplify operations by offering integrated systems that support everything from checkout to reporting.

Why I Picked NCR Voyix

What sets NCR Voyix apart is its ability to deliver both hardware and software as a unified payment solution for retailers. I picked NCR Voyix because it offers integrated point-of-sale terminals and payment processing software, which helps retailers manage transactions and in-store operations from a single provider. The platform also supports a range of payment types, including contactless and mobile payments, making it adaptable for modern retail environments. This combination of hardware and software integration is especially valuable for businesses that want to streamline their checkout experience and reduce vendor complexity.

NCR Voyix Key Features

Some other features that make NCR Voyix appealing for retail payment solutions include:

- EMV and PCI Compliance: Supports secure payment processing with EMV chip and PCI standards.

- Gift Card and Loyalty Program Support: Enables retailers to issue and manage branded gift cards and loyalty rewards.

- Remote Device Management: Lets IT teams monitor and update payment terminals from a central dashboard.

- Integrated Reporting Tools: Provides detailed sales and transaction analytics within the platform.

NCR Voyix Integrations

Native integrations are not currently listed.

Pros and Cons

Pros:

- Provides detailed transaction and sales reporting

- Built-in gift card and loyalty program support

- Includes remote device management capabilities

Cons:

- Customer support quality varies by region

- Hardware setup may require on-site installation

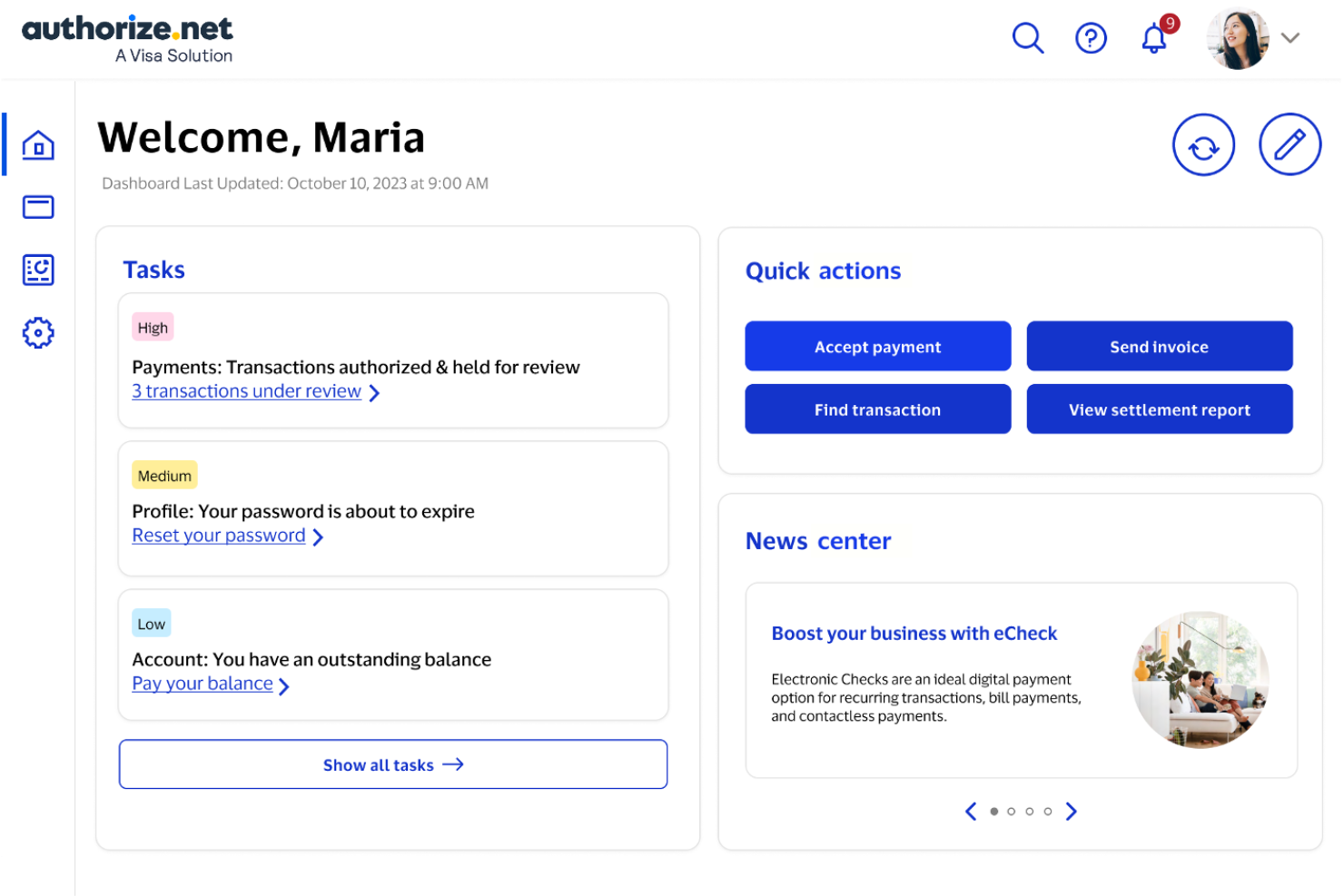

Retailers looking to minimize payment fraud often turn to Authorize.net for its advanced fraud detection capabilities. This payment gateway is a strong fit for businesses that need to process transactions securely across online, in-store, and mobile channels. Authorize.net helps teams reduce chargebacks and suspicious activity with customizable fraud filters and real-time monitoring.

Why I Picked Authorize.net

For retailers who need to prioritize fraud prevention, Authorize.net offers some of the most advanced tools in the payment space. I picked Authorize.net because its customizable Advanced Fraud Detection Suite lets you set rules for transaction monitoring, velocity filters, and IP address blocking. The platform also provides real-time alerts for suspicious activity, helping teams respond quickly to potential threats. If your business handles a high volume of transactions or operates in a high-risk category, these fraud controls can make a significant difference in protecting your revenue.

Authorize.net Key Features

In addition to its fraud detection capabilities, Authorize.net offers several other features that support retail payment operations:

- Recurring Billing: Lets you set up and manage automatic payment schedules for repeat customers.

- Virtual Terminal: Allows you to process payments manually from any internet-connected device.

- Customer Information Manager: Stores customer profiles securely for faster future transactions.

- Mobile Point of Sale App: Enables payment acceptance on smartphones and tablets for in-person sales.

Authorize.net Integrations

Integrations include Shopify, WooCommerce, Adobe Commerce, BigCommerce, Salesforce, NetSuite, Fishbowl, QuickBooks, X-Cart, and Volusion.

Pros and Cons

Pros:

- PCI DSS compliance tools are included

- Accepts ACH and eCheck payments natively

- Virtual terminal enables remote payment processing

Cons:

- International card acceptance is limited

- No built-in hardware for in-person payments

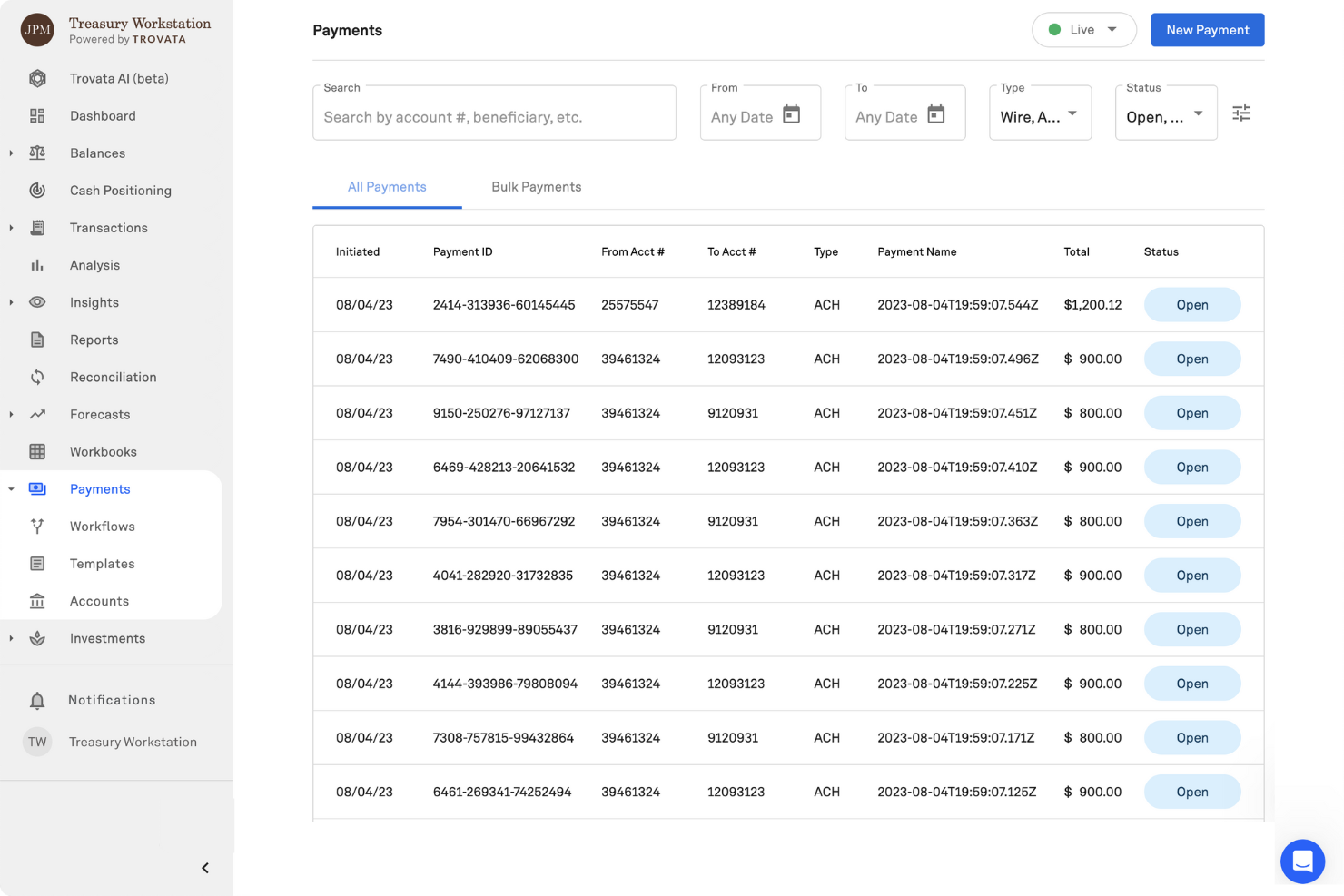

For retailers managing high transaction volumes and complex global operations, J.P. Morgan offers enterprise-grade payment infrastructure built for scale and security. This solution is designed for large retailers and omnichannel businesses that need advanced fraud protection, multi-currency support, and integration with existing financial systems. J.P. Morgan helps enterprise teams centralize payment processing and gain deeper visibility into payment data across regions and channels.

Why I Picked J.P. Morgan

When enterprise retailers need payment infrastructure that can handle scale, complexity, and security, J.P. Morgan is a clear choice. I picked J.P. Morgan because it offers advanced fraud detection tools and multi-currency processing, which are essential for global retail operations. The platform also provides centralized payment management, allowing finance and operations teams to monitor and control transactions across multiple channels and regions. These features make J.P. Morgan especially well-suited for large retailers with demanding payment requirements.

J.P. Morgan Key Features

Some other features in J.P. Morgan that are valuable for retail payment solutions include:

- Omnichannel Payment Acceptance: Accept payments across in-store, online, and mobile channels with unified reporting.

- Tokenization Services: Replace sensitive payment data with secure tokens to reduce PCI scope.

- Real-Time Payment Tracking: Monitor payment status and settlement in real time through a centralized dashboard.

- Customizable Reporting Tools: Generate detailed, configurable reports for transaction analysis and reconciliation.

J.P. Morgan Integrations

Native integrations are not currently listed.

Pros and Cons

Pros:

- Customizable reporting for transaction-level insights

- PCI-compliant tokenization for sensitive data protection

- Real-time payment tracking and settlement visibility

Cons:

- Not suitable for small or mid-sized retailers

- Limited information on native third-party integrations

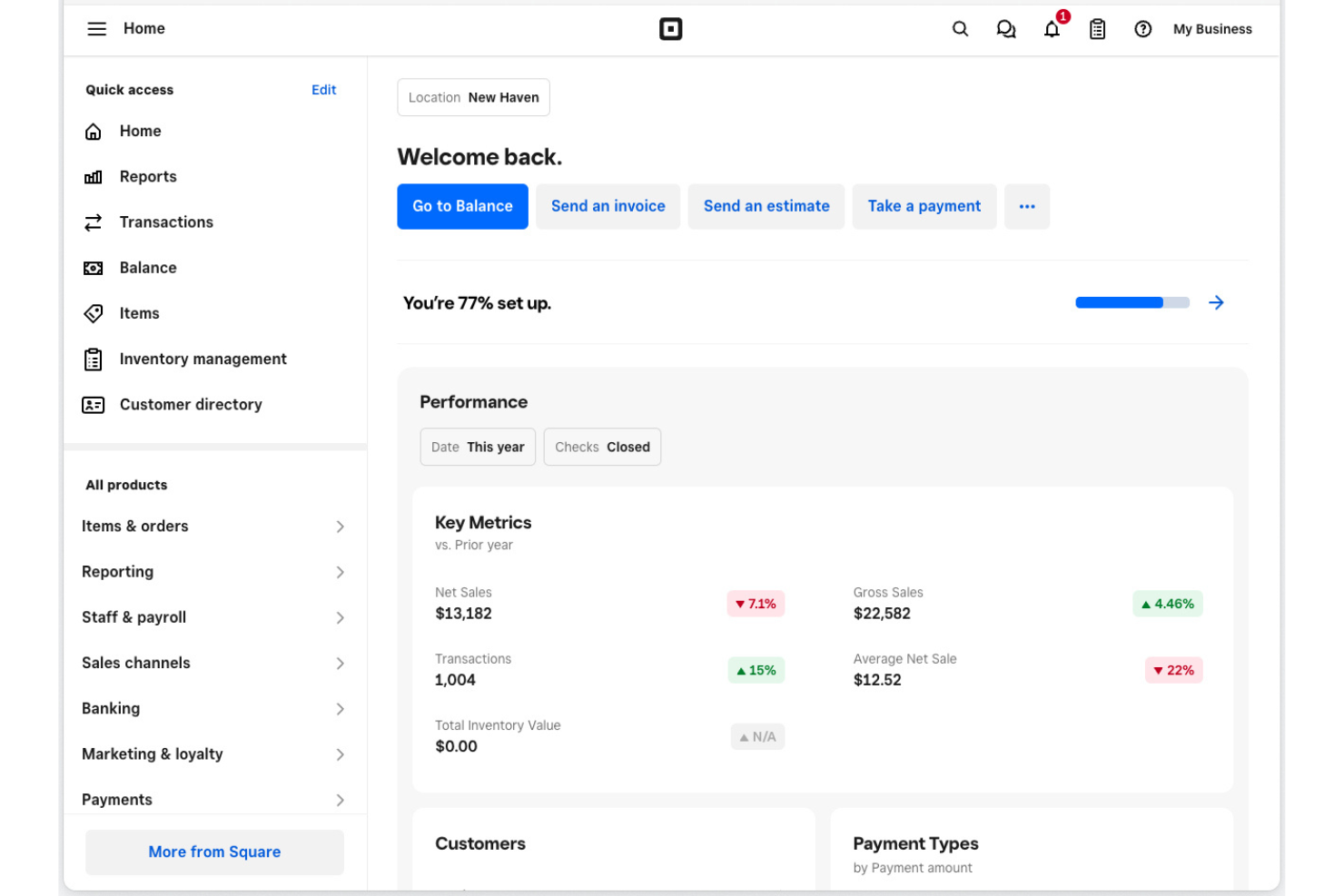

If you need to start accepting payments in a physical retail space quickly, Square offers a straightforward solution. It’s especially useful for small businesses and pop-up shops that want to get up and running with minimal hardware and setup. Square helps retailers handle in-person transactions, inventory, and receipts without complex onboarding or technical requirements.

Why I Picked Square

For retailers who need to get up and running fast in a physical location, Square stands out for its plug-and-play hardware and instant account activation. I picked Square because you can start accepting card payments with just a mobile device and a card reader, without waiting for lengthy approvals or complicated installations. The system also includes built-in inventory tracking and digital receipt options, which help small retailers manage daily operations from day one. This makes Square a practical choice for pop-ups, seasonal shops, and new storefronts that want to launch quickly.

Square Key Features

Some other features in Square that are useful for retail payment solutions include:

- Employee Management: Track employee hours, permissions, and sales performance directly from the Square dashboard.

- Gift Card Support: Sell and redeem physical or digital gift cards through your Square system.

- Customer Directory: Build and manage a customer database for marketing and loyalty programs.

- Sales Analytics: Access real-time sales reports and insights to monitor business performance.

Square Integrations

Integrations include QuickBooks, Xero, Wix, WooCommerce, BigCommerce, Ecwid, FreshBooks, Mailchimp, Homebase, and Zoho Books.

Pros and Cons

Pros:

- Built-in gift card and loyalty program features

- Supports offline payments for unreliable connections

- Free POS app included with hardware purchase

Cons:

- International payment acceptance is not supported

- Hardware compatibility is restricted to Square devices

New Product Updates from Square

Square Improves Restaurant Service With Gratuity, Table, and Cart Updates

Square introduced updates for restaurant service, including pre-discount auto-gratuity calculations, table merging, and a real-time cart preview during item configuration. The enhancements help staff manage orders, checks, and pricing more efficiently. For more information, visit Square’s official site.

.

.

Helcim offers retail businesses a payment solution with transparent interchange-plus pricing and no monthly fees. This approach appeals to merchants who want clear, predictable costs and need to process both in-person and online payments. With Helcim, you can access features like automatic volume discounts and integrated invoicing without worrying about hidden charges.

Why I Picked Helcim

For retailers who want to avoid hidden fees and unpredictable costs, Helcim’s transparent interchange-plus pricing model is a clear advantage. I picked Helcim because it publishes its rates openly and automatically applies volume discounts as your sales grow. The platform also provides detailed fee breakdowns for every transaction, so you always know exactly what you’re paying. This level of transparency helps retail teams manage margins and make informed decisions about payment processing.

Helcim Key Features

Some other features worth highlighting include:

- Hosted Payment Pages: Lets you create secure, customizable checkout pages for online sales.

- Integrated Invoicing: Allows you to send invoices and accept payments directly through the platform.

- Customer Management Tools: Stores customer profiles and payment details for recurring billing or future purchases.

- Mobile Card Reader: Supports in-person payments with a wireless card reader that connects to your phone or tablet.

Helcim Integrations

Integrations include QuickBooks Online and Xero. An API is available for custom integrations.

Pros and Cons

Pros:

- Supports both in-person and online payments

- Integrated invoicing and recurring billing tools

- Free virtual terminal for phone orders

Cons:

- Pricing structure can be complex

- Transaction fees can be pricey for certain business types

{kind=link}

How I Evaluate Retail Payment Solutions

I split my evaluation into two layers: baseline capabilities a solution must have to qualify, and the differentiators that separate the right fit for a high-volume chain from a single-store retailer.

Core Functionality (Table Stakes For This List)

When I'm selecting tools for my list, I rank each one on a scale from 0 (does not offer the functionality) to 5 (excels in this area) for each core functionality listed below. Then, I calculate the tool's total score into a percentage. Each tool needs to achieve a minimum total score of 65% to be considered for inclusion.

- Multi-Method Payment Acceptance: I check whether the solution handles EMV chip, contactless tap, magstripe, and mobile wallets like Apple Pay and Google Pay at checkout.

- POS Hardware Integration: Supported terminals matter—I look at whether a platform works with its own readers and third-party hardware like Verifone or Ingenico.

- PCI DSS Compliance & Security: Every solution I evaluate should offer PCI DSS-compliant infrastructure with encryption and tokenization to protect cardholder data.

- Omnichannel Payment Processing: Retailers selling in-store, online, and via mobile need unified processing, so I look for a single system across all channels.

- Transaction Reporting & Reconciliation: Real-time settlement tracking and dispute tools help multi-store operators close their books faster, so I evaluate reporting depth.

- POS & Retail System Integrations: I look for native connectors to major POS platforms, inventory tools, and accounting software like QuickBooks or Xero.

Once I have a list of tools that meet this criteria, I consider what sets each platform apart.

Differentiating Factors (What Sets Vendors Apart)

Here's how I compare and contrast different vendors:

Standout Features

Offline payment mode matters more than most buyers realize—I look for solutions that queue transactions locally so a busy checkout lane doesn't grind to a halt during an internet outage. Smart routing and interchange optimization is another area I evaluate closely, since multi-location retailers processing thousands of transactions daily can see meaningful cost reductions when the platform routes each transaction to the lowest-cost network. I also consider AI-powered fraud detection, especially for omnichannel sellers where card-present and card-not-present risk profiles differ.

Beyond Features

Pricing transparency is the first thing I check—whether a vendor offers flat-rate, interchange-plus, or tiered pricing, I want to see the full fee structure upfront with no buried PCI or early termination charges. Settlement speed also weighs heavily, because a retailer restocking inventory weekly needs next-day or same-day funding, not a three-day hold. Hardware flexibility rounds out my evaluation; I consider whether a platform supports countertop terminals, mPOS readers, and self-checkout kiosks so you can mix form factors as your store footprint evolves.

Cómo Elegir Soluciones de Pago para Retail

Es fácil perderse entre largas listas de funciones y estructuras de precios complejas. Para que puedas mantener el enfoque durante tu proceso único de selección de software, aquí tienes una lista de factores a tener en cuenta:

| Factor | Qué considerar |

|---|---|

| Escalabilidad | ¿La solución apoyará tu crecimiento hacia nuevas ubicaciones, canales o mayores volúmenes de transacciones sin grandes actualizaciones? |

| Integraciones | ¿La herramienta se conecta de manera nativa con tu POS, comercio electrónico, contabilidad y sistema de inventario? Verifica si es compatible con tu infraestructura tecnológica. |

| Personalización | ¿Puedes adaptar los flujos de trabajo, recibos y opciones de pago para que coincidan con tu marca y necesidades operativas? |

| Facilidad de uso | ¿Tu personal aprenderá el sistema rápidamente? Busca interfaces intuitivas y requisitos mínimos de formación, especialmente para equipos con alta rotación. |

| Implementación y puesta en marcha | ¿Cuánto tiempo llevará la configuración y qué recursos se requieren? Pregunta sobre soporte de migración, capacitación, y posibles periodos de inactividad. |

| Costo | ¿Todas las tarifas son transparentes, incluidas las de transacción, hardware e integración? Compara mínimos mensuales y términos del contrato. |

| Medidas de seguridad | ¿La solución cumple con PCI y ofrece herramientas de prevención de fraude? Pregunta sobre cifrado, tokenización y respuesta ante violaciones de seguridad. |

| Disponibilidad de soporte | ¿Qué canales de soporte se ofrecen y en qué horarios? Considera si necesitas ayuda 24/7 o gestión de cuenta dedicada. |

¿Qué Son las Soluciones de Pago para Retail?

Las soluciones de pago para el comercio minorista son sistemas de software y hardware que permiten a las empresas aceptar, procesar y gestionar los pagos de los clientes tanto en tienda física como en línea. Estas soluciones gestionan transacciones a través de diversos métodos de pago, incluyendo tarjetas de crédito, monederos móviles y opciones sin contacto. Suelen incluir herramientas para el seguimiento de ventas, gestión de reembolsos y garantizar la seguridad de los pagos, ayudando a los minoristas a ofrecer una experiencia de pago consistente y fiable en todos los canales.

Características

Al seleccionar soluciones de pago para el comercio minorista, presta atención a las siguientes características clave:

- Aceptación de pagos en múltiples canales: Admite transacciones en tienda, en línea y desde dispositivos móviles, para que puedas atender a los clientes dondequiera que compren.

- Procesamiento de pagos integrado: Se conecta directamente con los procesadores de pago para gestionar pagos con tarjeta de crédito, débito y sin contacto, sin intervención manual.

- Informes de ventas y transacciones: Ofrece informes en tiempo real e históricos sobre ventas, tipos de pago y volúmenes de transacciones para ayudarte a monitorear el desempeño del negocio.

- Gestión de devoluciones y reembolsos: Permite procesar reembolsos y devoluciones de manera eficiente, garantizando registros precisos y una experiencia fluida para el cliente.

- Sincronización de inventario: Actualiza automáticamente los niveles de inventario a medida que se realizan ventas, reduciendo errores y ayudando a prevenir faltantes o sobreventa.

- Recibos personalizables: Permite adaptar los recibos impresos o digitales con la imagen de tu marca, políticas de devolución y mensajes promocionales.

- Permisos para empleados: Te permite establecer roles de usuario y restringir el acceso a funciones sensibles de pago, mejorando la seguridad y la responsabilidad.

- Soporte para tarjetas de regalo y programas de fidelización: Emite, rastrea y canjea tarjetas de regalo y recompensas de fidelidad, fomentando la repetición de compras y la retención de clientes.

- Cumplimiento PCI y herramientas de seguridad: Garantiza que todas las transacciones cumplan con los estándares de seguridad de la industria, incluyendo funciones como encriptación y detección de fraudes para proteger los datos del cliente.

Beneficios

Implementar soluciones de pago para el comercio minorista aporta varios beneficios a tu equipo y negocio. Aquí algunos de los que puedes esperar:

- Experiencias de pago más rápidas: El procesamiento integrado y la aceptación en múltiples canales ayudan a reducir los tiempos de espera y agilizan las filas.

- Mayor visibilidad de las ventas: Los informes en tiempo real sobre ventas y transacciones te dan una visión clara del rendimiento del negocio en todas las ubicaciones y canales.

- Mejor seguridad en los pagos: El cumplimiento PCI, la encriptación y las herramientas de detección de fraudes ayudan a proteger los datos sensibles del cliente y a reducir riesgos.

- Gestión simplificada de devoluciones y reembolsos: Las funciones integradas para devoluciones y reembolsos facilitan la resolución de incidencias del cliente y el mantenimiento de registros precisos.

- Mayor control de inventario: La sincronización automática de inventario garantiza que los niveles de stock estén siempre actualizados, minimizando errores y sobreventas.

- Fidelización de clientes más sólida: El soporte de tarjetas de regalo y programas de fidelidad incentiva las visitas recurrentes y ayuda a construir relaciones duraderas con los clientes.

- Mejor control operativo: Los permisos para empleados y los recibos personalizables te permiten gestionar el acceso y adaptar la experiencia de pago a las necesidades de tu marca.

Costos y Precios

Seleccionar soluciones de pago para el comercio minorista requiere entender los diferentes modelos y planes de precios disponibles. Los costos varían según las características, el tamaño del equipo, los complementos y más. La siguiente tabla resume los planes comunes, sus precios promedio y las funciones típicas incluidas en las soluciones de pago para retailers:

Tabla Comparativa de Planes para Soluciones de Pago en Retail

| Tipo de Plan | Precio Promedio | Características Comunes |

| Plan Gratuito | $0 | Acepta pagos básicos, ofrece reportes limitados, soporta un solo usuario y brinda atención básica. |

| Plan Personal | $20-$40/user/month | Incluye aceptación de pagos en múltiples canales, rastreo básico de inventario, recibos personalizables y soporte estándar. |

| Plan Business | $60-$120/user/month | Agrega informes avanzados, permisos para empleados, integraciones con comercio electrónico y contabilidad, y soporte para programas de fidelidad. |

| Plan Enterprise | $150-$300+/user/month | Ofrece integraciones personalizadas, gestión dedicada de cuentas, herramientas de seguridad avanzadas, soporte prioritario y gestión multi-sede. |

Preguntas frecuentes sobre soluciones de pago para comercios minoristas

Aquí tienes respuestas a algunas preguntas comunes sobre las soluciones de pago para comercios minoristas:

¿Pueden las soluciones de pago para comercios minoristas gestionar tanto transacciones en tienda como en línea?

Sí, la mayoría de las soluciones de pago para comercios minoristas admiten tanto transacciones en tienda como en línea. Esto te permite gestionar los pagos en ubicaciones físicas y canales de comercio electrónico desde un solo sistema, facilitando el seguimiento de ventas e inventario.

¿Qué métodos de pago admiten las soluciones de pago para comercios minoristas?

Las soluciones de pago para comercios minoristas suelen admitir tarjetas de crédito, tarjetas de débito, billeteras móviles, pagos sin contacto y, en algunos casos, tarjetas de regalo. Algunos sistemas también permiten pagos divididos o tipos de pago personalizados, dependiendo de las necesidades de tu negocio.

¿Cómo ayudan las soluciones de pago para comercios minoristas con la seguridad y el cumplimiento normativo?

Las soluciones de pago para comercios minoristas utilizan cifrado, tokenización y estándares de cumplimiento PCI para proteger los datos de pago sensibles. Muchas también incluyen herramientas de detección de fraudes y actualizaciones de seguridad regulares para ayudar a reducir el riesgo de filtraciones de datos.

¿Están disponibles las integraciones con otros sistemas empresariales?

Sí, la mayoría de las soluciones de pago para comercios minoristas ofrecen integraciones con plataformas de comercio electrónico, software de contabilidad, herramientas de gestión de inventarios y sistemas CRM. Esto te ayuda a centralizar la información y automatizar los flujos de trabajo en tu negocio.

¿Qué debo considerar al elegir una solución de pago para comercios minoristas con varias sucursales?

Busca soluciones que ofrezcan informes centralizados, gestión de múltiples ubicaciones y permisos de usuario. Estas características te ayudarán a monitorear el rendimiento, controlar el acceso y mantener la coherencia en todas tus tiendas.