14 Affirm Alternatives for 2026

Affirm Alternatives Shortlist

Here’s my shortlist of Affirm alternatives:

A strong Affirm alternative offers flexible buy now, pay later options, broad acceptance, and features that fit your business model and customer needs. If you’re searching for an Affirm competitor or comparing pay later apps, you’re likely weighing payment flexibility, interest rates, and how these financial services integrate with your existing checkout and risk management systems. Many BNPL apps and other pay-later companies let customers split online purchases into monthly payments, set a clear due date, and sometimes access longer-term financing. These platforms may also include features like virtual cards, cash back rewards, and tools that connect to credit reports or consider a customer’s credit score when approving purchases. For small businesses, choosing the right BNPL option can improve conversion rates and expand access to flexible payment methods for shoppers focused on personal finance and budgeting.

This list will help you compare leading alternatives so you can choose the best solution for your checkout experience and growth strategy.

What Is Affirm?

Affirm is a financial technology service that lets customers split purchases into installment payments at checkout. It partners with retailers to offer buy now, pay later options, giving shoppers more flexibility in how they pay. Affirm handles credit checks, payment processing, and customer support, making it easier for businesses to offer financing without managing the risk or logistics themselves. This approach helps merchants reach more customers and increase average order values.

Best Affirm Alternatives Summary

This comparison chart summarizes pricing details for my top Affirm alternative selections to help you find the best one for your budget and business needs.

| Tool | Best For | Trial Info | Price | ||

|---|---|---|---|---|---|

| 1 | Best for developer-friendly APIs | 30-day free trial available | From 2.9% + 30¢ per transaction | Website | |

| 2 | Best for interest-free payment plans | Free plan available | Pricing upon request | Website | |

| 3 | Best for flexible installment options | Free demo available | Pricing upon request | Website | |

| 4 | Best with global payment acceptance | Not available | From 2.29% + $0.09 per transaction | Website | |

| 5 | Best for fast in-store approvals | Free demo available | Pricing upon request | Website | |

| 6 | Best for using existing credit cards | Free demo available | Pricing upon request | Website | |

| 7 | Best for transparent fee structures | Not available | From 5.9% plus $0.30 per transaction | Website | |

| 8 | Best for India-based installment services | Not available | Pricing upon request | Website | |

| 9 | Best for Middle East market coverage | Not available | Pricing upon request | Website | |

| 10 | Best for integrated store financing | Not available | Pricing upon request | Website |

Why Trust Our Software Reviews

Affirm Alternatives Reviews

Below are my detailed summaries of the Affirm alternatives that made it onto my shortlist. My reviews offer a detailed look at the features, best use cases, and integrations of each platform to help you find the best one for you.

Stripe is a strong choice for businesses that want to build custom payment experiences using flexible APIs. This platform appeals to e-commerce teams, SaaS providers, and marketplaces that need to embed payments, subscriptions, or buy now, pay later directly into their workflows. Stripe stands out from Affirm and similar solutions by giving developers granular control over payment logic, user flows, and integration with other business systems.

Why Stripe Is a Good Affirm Alternative

Unlike many BNPL providers, Stripe gives your developers direct access to a wide range of payment APIs, making it ideal for teams that want to customize every aspect of the checkout and payment experience. I picked Stripe because it lets you embed buy now, pay later, recurring billing, and one-time payments all within a single, unified platform. With Stripe’s API-first approach, you can tailor payment flows, automate financial operations, and connect payments to other business systems. This flexibility is especially valuable for businesses with unique workflows or advanced technical requirements.

Stripe Key Features

Some other features worth highlighting include:

- Prebuilt Payment UI Components: Use ready-made checkout forms and payment elements to speed up deployment.

- Dispute Management Tools: Access built-in workflows for handling chargebacks and customer disputes.

- Global Currency Support: Accept payments in over 135 currencies with automatic currency conversion.

- Fraud Detection With Stripe Radar: Leverage machine learning to identify and block fraudulent transactions in real time.

Stripe Integrations

Integrations include Synder, Commerce Sync, Zapier, Salesforce, QuickBooks Online, Churnkey, RevenueCat, and more.

Pros and Cons

Pros:

- Real-time fraud detection with Stripe Radar

- Supports multiple BNPL providers in checkout

- Developer-first APIs for custom payment flows

Cons:

- Requires technical resources for advanced setup

- No direct consumer financing or lending

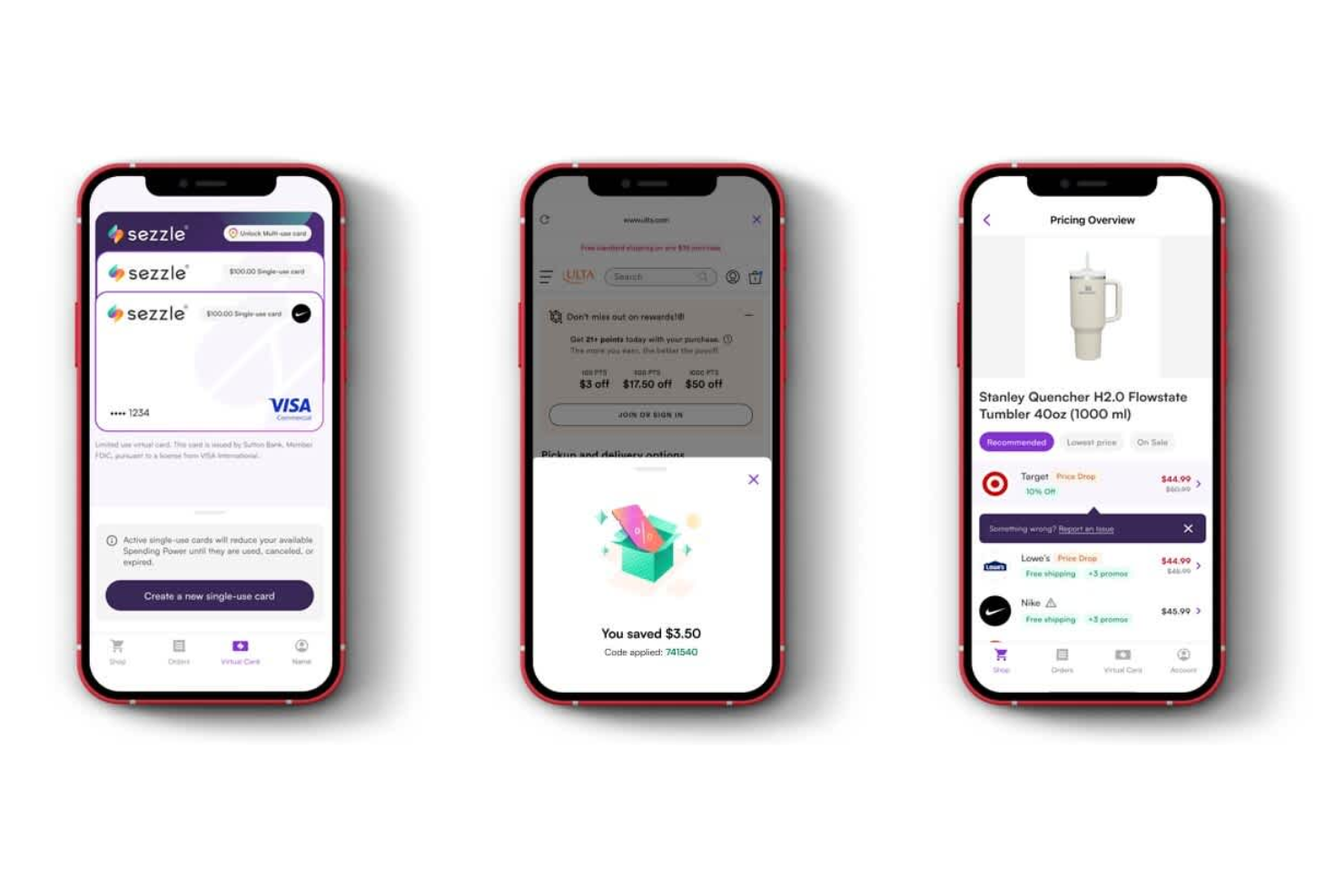

Sezzle gives retailers a way to offer interest-free payment plans at checkout, appealing to businesses that want to attract budget-conscious shoppers. This solution is especially useful for e-commerce brands and omnichannel retailers looking to reduce cart abandonment without adding financing costs for customers. Sezzle stands out from Affirm and similar services by focusing on short-term, no-interest installment options that help shoppers manage purchases responsibly.

Why Sezzle Is a Good Affirm Alternative

If you want to offer interest-free payment plans, Sezzle is a strong alternative to Affirm. I picked Sezzle because it lets your customers split purchases into four equal, interest-free payments over six weeks. The platform also provides instant approval decisions and does not require a hard credit check, making it accessible to a wider range of shoppers. Sezzle’s focus on short-term, no-interest plans helps you attract customers who want to avoid debt and manage their spending responsibly.

Sezzle Key Features

Some other features that caught my attention with Sezzle include:

- Merchant Analytics Portal: Track payment activity, order volume, and customer trends from a single dashboard.

- Automated Payment Reminders: Sezzle sends reminders to customers before each installment is due to help reduce missed payments.

- Customizable Checkout Integration: Add Sezzle as a payment option with branded buttons and messaging that fit your store’s design.

- Dispute Resolution Center: Manage chargebacks and customer disputes directly within the Sezzle platform.

Sezzle Integrations

Integrations include Shopify, WooCommerce, BigCommerce, Wix, Salesforce Commerce Cloud, Magento, CommentSold, and more.

Pros and Cons

Pros:

- Supports rescheduling of payment dates

- Instant approval decisions at checkout

- Soft credit checks do not impact scores

Cons:

- Not available for high-ticket purchases

- Limited to four installment payments

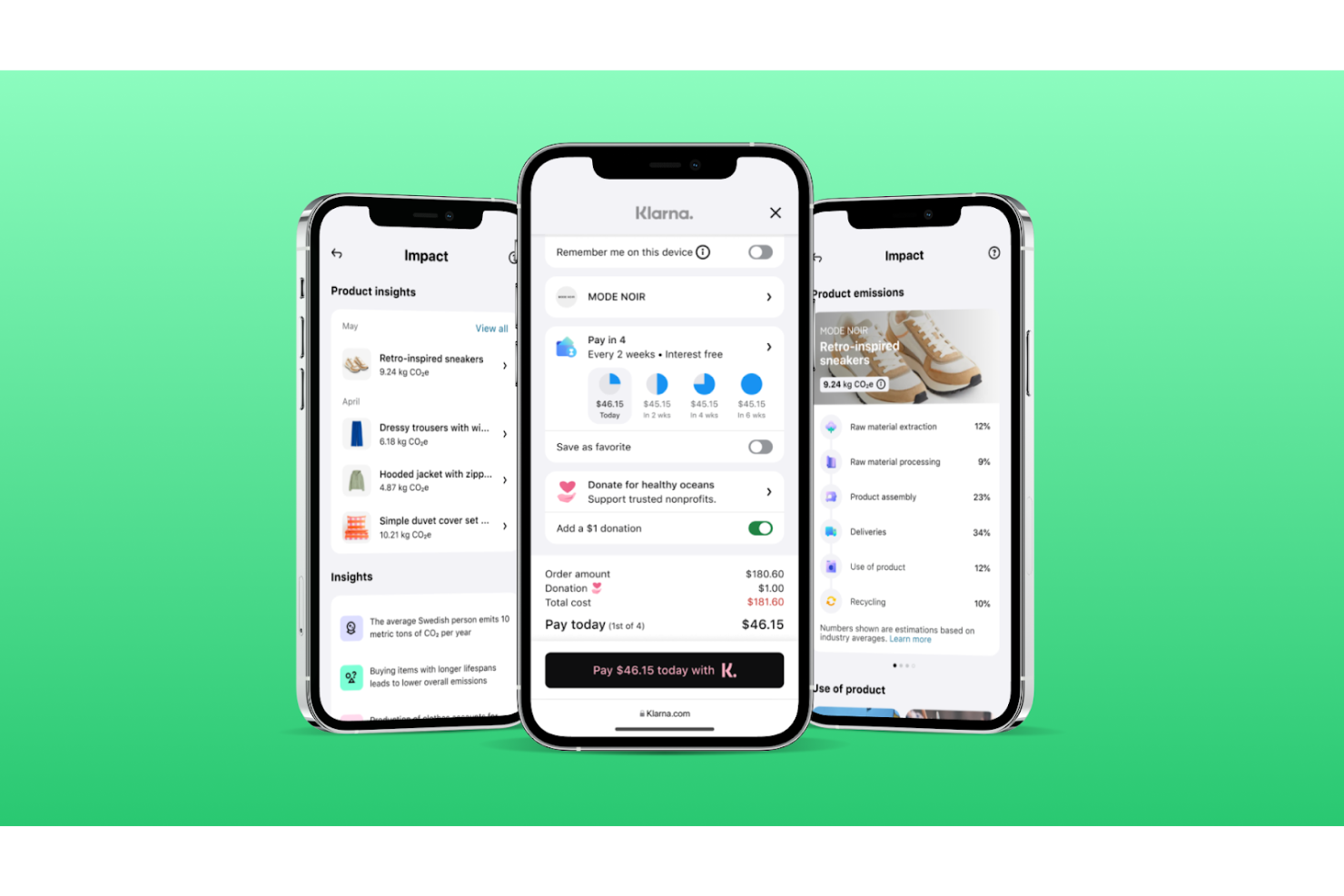

Klarna offers a wide range of flexible installment payment options for retailers looking to give customers more control at checkout. This platform appeals to e-commerce businesses and omnichannel retailers who want to offer pay-over-time choices without adding complexity to their operations. Klarna stands out for its variety of payment plans and its ability to support both online and in-store transactions.

Why Klarna Is a Good Affirm Alternative

Klarna stands out for its flexible installment options, making it a strong choice if you want to offer customers more ways to pay over time. I picked Klarna because it lets you provide multiple payment schedules, including pay in 4, monthly financing, and deferred payments. The platform also supports both online and in-store purchases, so you can create a consistent experience across channels. Klarna’s real-time credit checks and instant approvals help reduce friction at checkout for your customers.

Klarna Key Features

Some other features I noticed in Klarna that may interest you include:

- Merchant Analytics Dashboard: Access real-time sales data, payment statuses, and customer insights from a centralized dashboard.

- Automated Fraud Protection: Klarna uses machine learning to detect and prevent fraudulent transactions before they impact your business.

- Customizable Checkout Widgets: Add Klarna’s payment options to your site with branded widgets that match your store’s look and feel.

- Dispute Management Tools: Handle chargebacks and customer disputes directly within the Klarna platform, simplifying resolution processes.

Klarna Integrations

Integrations include Stripe, Shopify, WooCommerce, Adobe, Mollie, Kustom, Adyen, Checkout.com, and more.

Pros and Cons

Pros:

- Automated fraud detection tools

- Real-time credit checks at checkout

- Supports both online and in-store payments

Cons:

- Some users report delayed merchant payouts

- Limited control over approval decisions

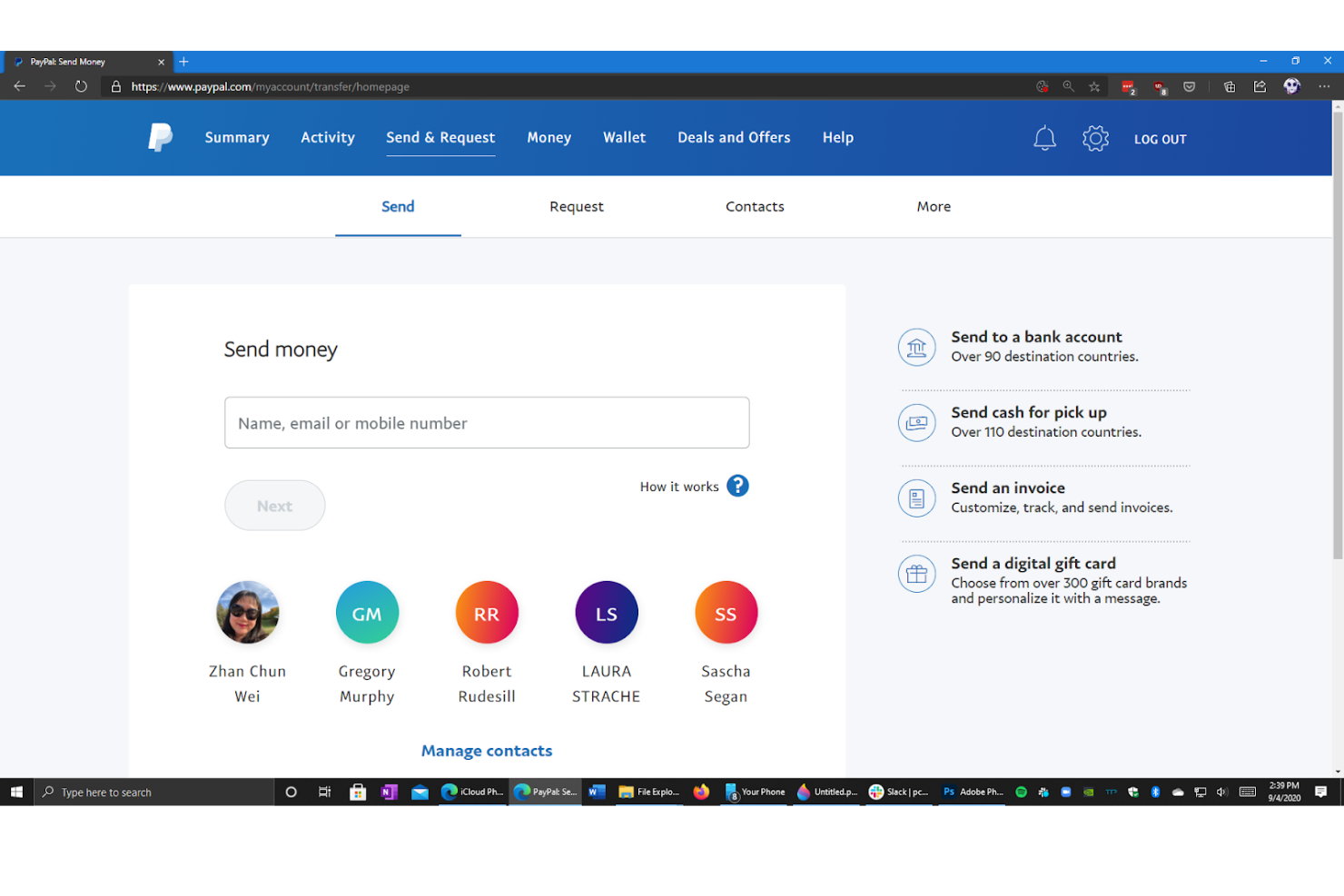

PayPal offers a way for businesses to accept payments from customers in over 200 countries and regions, making it a strong fit for retailers with global ambitions. This platform is especially useful for e-commerce teams and omnichannel merchants who need to support multiple currencies and payment methods. Unlike Affirm, PayPal stands out for its broad international reach and ability to handle cross-border transactions with built-in currency conversion.

Why PayPal Is a Good Affirm Alternative

For businesses that need to accept payments from customers around the world, PayPal offers a level of global reach that Affirm doesn’t match. I picked PayPal because it supports payments in over 100 currencies and automatically handles currency conversion at checkout. The platform also allows you to accept a wide range of payment methods, including credit cards, debit cards, and local payment options. This makes PayPal a strong choice for retailers focused on international growth and cross-border sales.

PayPal Key Features

Some other PayPal features worth noting include:

- One-Touch Checkout: Customers can pay with a single click without re-entering payment details.

- Fraud Detection Tools: PayPal uses automated monitoring and risk analysis to help identify suspicious transactions.

- Recurring Payments Support: Set up and manage subscription billing or installment plans for your customers.

- Dispute Management Center: Handle chargebacks and customer disputes directly within your PayPal account.

PayPal Integrations

Integrations include Venmo, Apple Pay, Google Pay, and more.

Pros and Cons

Pros:

- Supports recurring billing and subscriptions

- Built-in fraud detection and buyer protection

- Accepts payments in over 100 currencies

Cons:

- Chargeback process can favor buyers over sellers

- Account holds can delay merchant payouts

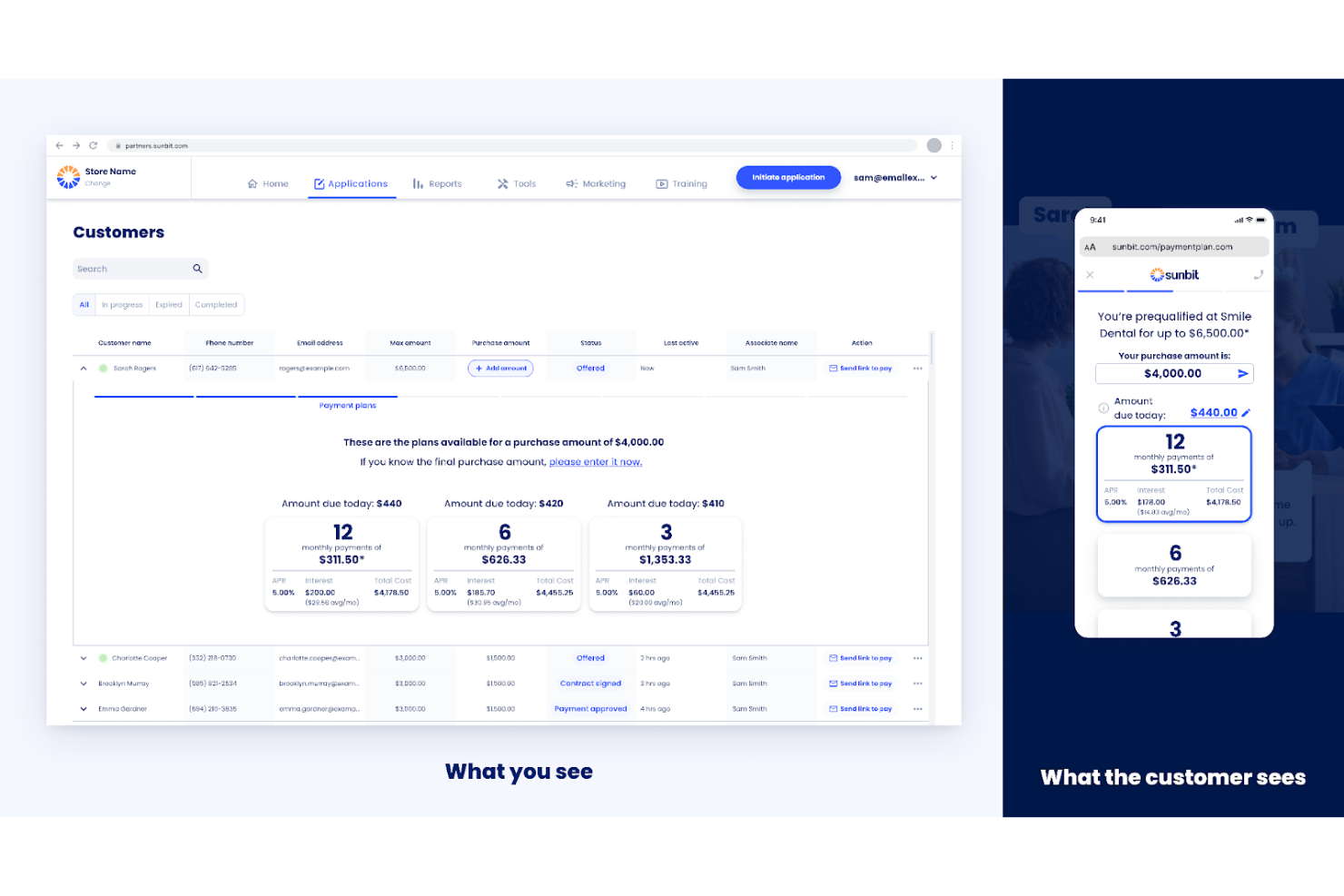

Sunbit is built for retailers and service providers who need a fast, frictionless way to offer financing at the point of sale. This tool stands out for its rapid in-store approval process, making it especially useful for businesses in automotive, dental, and healthcare settings where quick decisions matter. Unlike Affirm, Sunbit focuses on minimizing declines and delivering approvals in under a minute, helping merchants capture more sales without slowing down checkout.

Why Sunbit Is a Good Affirm Alternative

If your business relies on quick approvals at checkout, Sunbit is worth considering as an alternative to Affirm. I picked Sunbit because it specializes in in-store financing with approvals that typically take less than a minute. The platform uses a soft credit check and boasts a high approval rate, which helps merchants serve more customers without lengthy delays. This makes Sunbit especially valuable for retailers and service providers who can’t afford to slow down the point-of-sale process.

Sunbit Key Features

Some other Sunbit features that caught my attention include:

- Digital Application Process: Customers can complete financing applications on tablets or smartphones in-store.

- Multiple Payment Plan Options: Merchants can offer a range of installment terms to fit different budgets.

- Automated Payment Reminders: The system sends reminders to customers before each payment is due.

- Merchant Dashboard: Businesses get access to a portal for tracking applications, approvals, and payment statuses.

Sunbit Integrations

Integrations include myKaarma, Workiz, Shepherd, Zuub, Xtime, Weave, and more.

Pros and Cons

Pros:

- Payment plans available for healthcare and auto

- High approval rates for subprime customers

- Approvals typically take less than a minute

Cons:

- Customer support response times can vary

- Some users report high APRs for customers

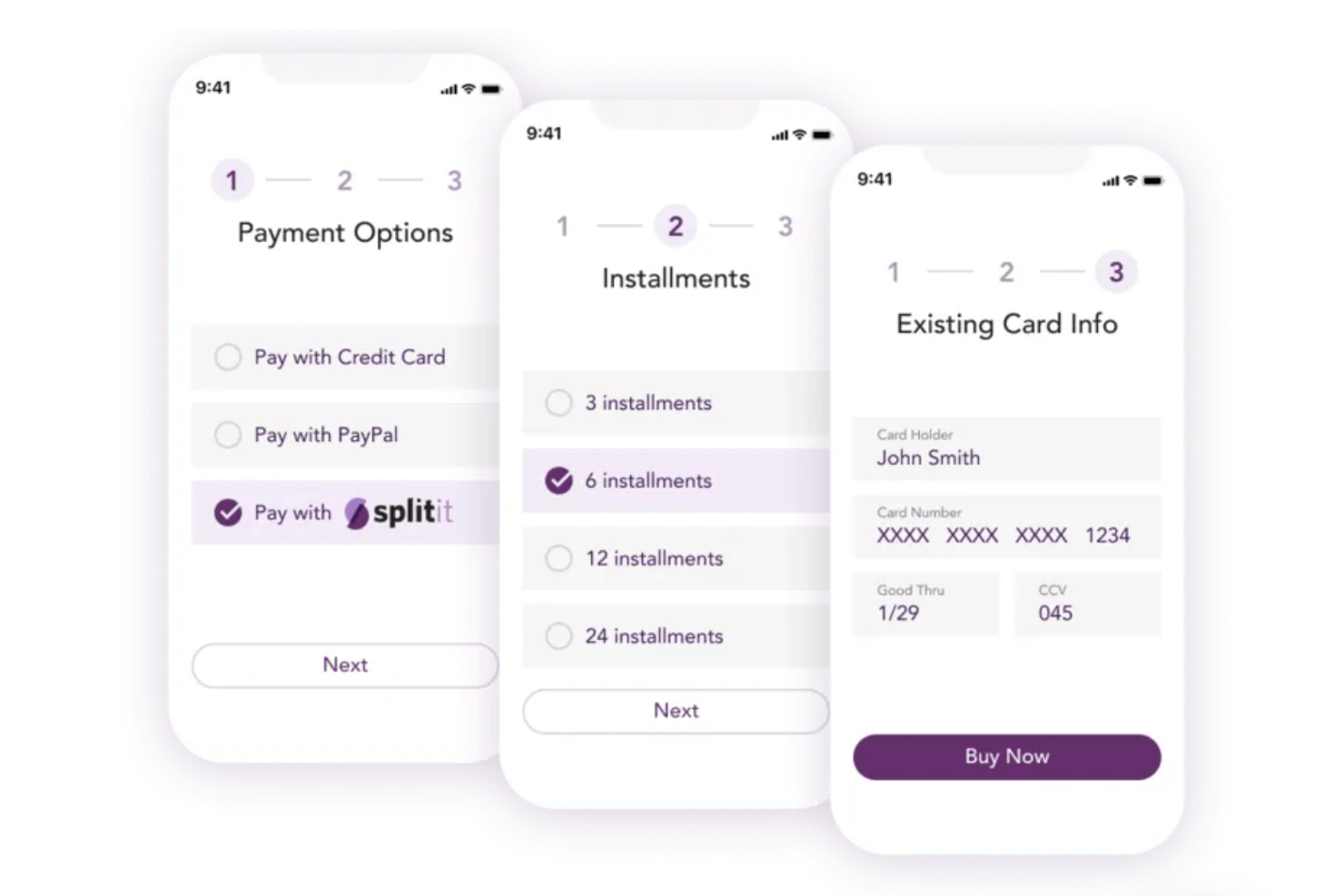

Splitit offers a unique approach for retailers who want to let customers pay in installments using their existing credit cards. This solution is a fit for e-commerce and omnichannel businesses that want to provide flexible payment options without requiring new lines of credit or additional applications. Unlike Affirm, Splitit leverages customers’ available credit, so shoppers can split payments without extra approvals or interest charges from a third party.

Why Splitit Is a Good Affirm Alternative

What sets Splitit apart is its ability to let customers use their existing credit cards for installment payments. I picked Splitit because it doesn’t require shoppers to open new credit lines or go through additional approval processes. The platform authorizes the full purchase amount on the customer’s card and then releases the hold as each installment is paid. This approach helps businesses offer flexible payments while reducing friction and credit risk compared to Affirm.

Splitit Key Features

Some other Splitit features worth noting include:

- White-Label Payment Experience: Merchants can fully brand the installment payment flow to match their store.

- Global Currency Support: Accept payments and offer installments in multiple currencies for international customers.

- Real-Time Payment Authorization: Instantly verify available credit and approve transactions at checkout.

- Merchant Analytics Dashboard: Access detailed reports on transaction volume, payment status, and customer usage.

Splitit Integrations

Integrations include Shopify, WooCommerce, Wix, Magento, Salesforce Commerce Cloud, PrestaShop, and more.

Pros and Cons

Pros:

- White-label option for branded checkout

- No interest or late fees applied

- No new credit checks for customers

Cons:

- No direct long-term financing options

- Only supports credit card installment payments

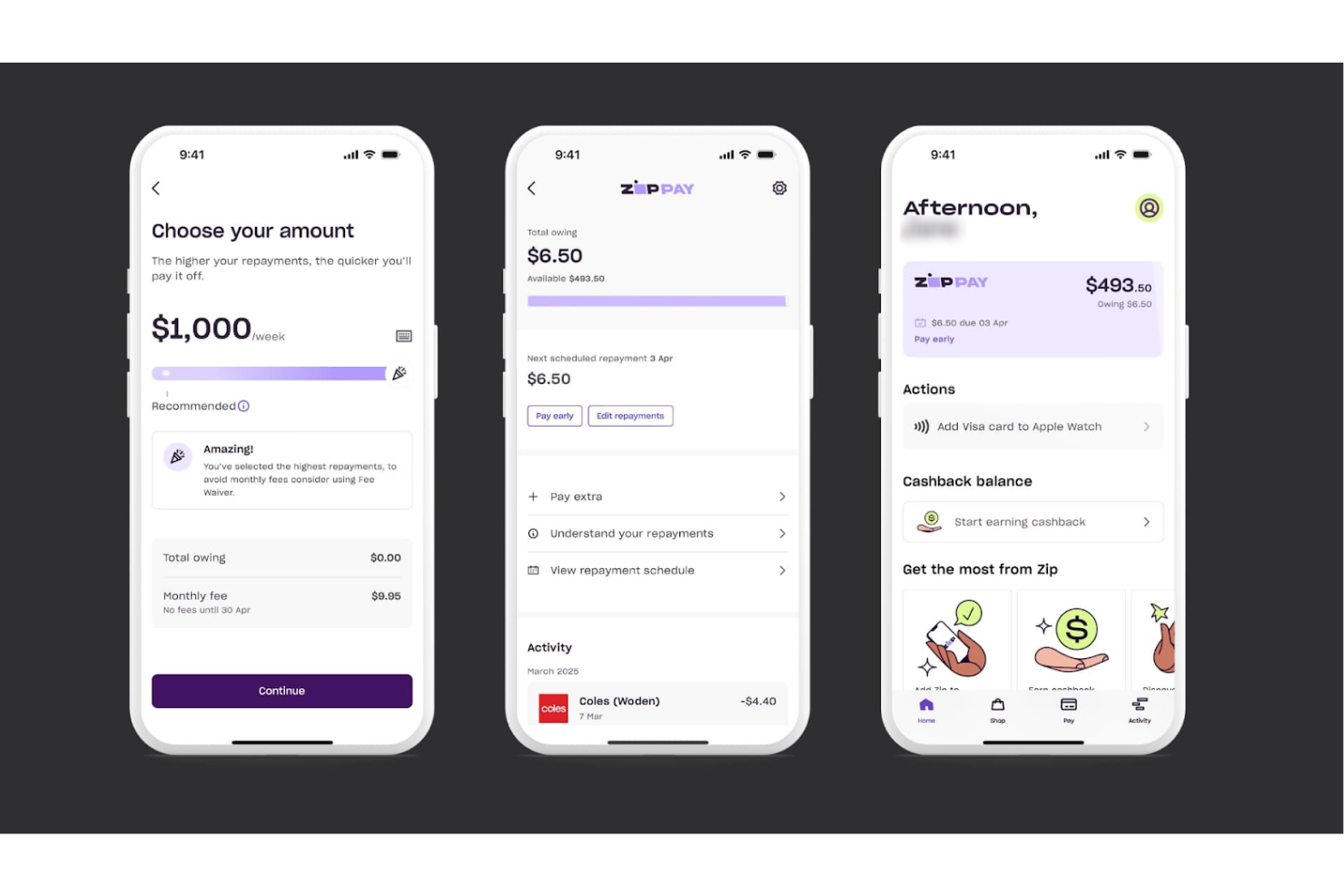

Retailers looking for a clear, upfront approach to buy now, pay later services may want to consider Zip. This platform appeals to e-commerce and omnichannel businesses that want to avoid hidden fees and complicated pricing. Unlike Affirm, Zip emphasizes transparent fee structures so you always know exactly what you’ll pay per transaction.

Why Zip Is a Good Affirm Alternative

If you want a payment solution with no surprises, Zip stands out for its transparent fee structure. I appreciate that Zip clearly displays its merchant fees upfront, so you always know the exact cost per transaction. The platform also avoids hidden charges and provides detailed reporting on all fees collected. This level of transparency helps businesses budget more accurately and avoid unexpected costs compared to Affirm.

Zip Key Features

Some other Zip features that caught my attention include:

- Flexible Repayment Schedules: Merchants can offer customers multiple installment options at checkout.

- Real-Time Transaction Tracking: Monitor all customer payments and order statuses from a single dashboard.

- Customizable Checkout Integration: Add Zip as a payment method to your site with branded elements and messaging.

- Automated Settlement Process: Receive funds directly to your business account without manual intervention.

Zip Integrations

Integrations include WooCommerce, BigCommerce, CartHook, Adyen, Stripe, Salesforce, Shopify, and more.

Pros and Cons

Pros:

- Instant approval decisions at checkout

- Flexible installment plans for customers

- Flat merchant fees with no hidden charges

Cons:

- No long-term financing options for customers

- Limited availability outside select countries

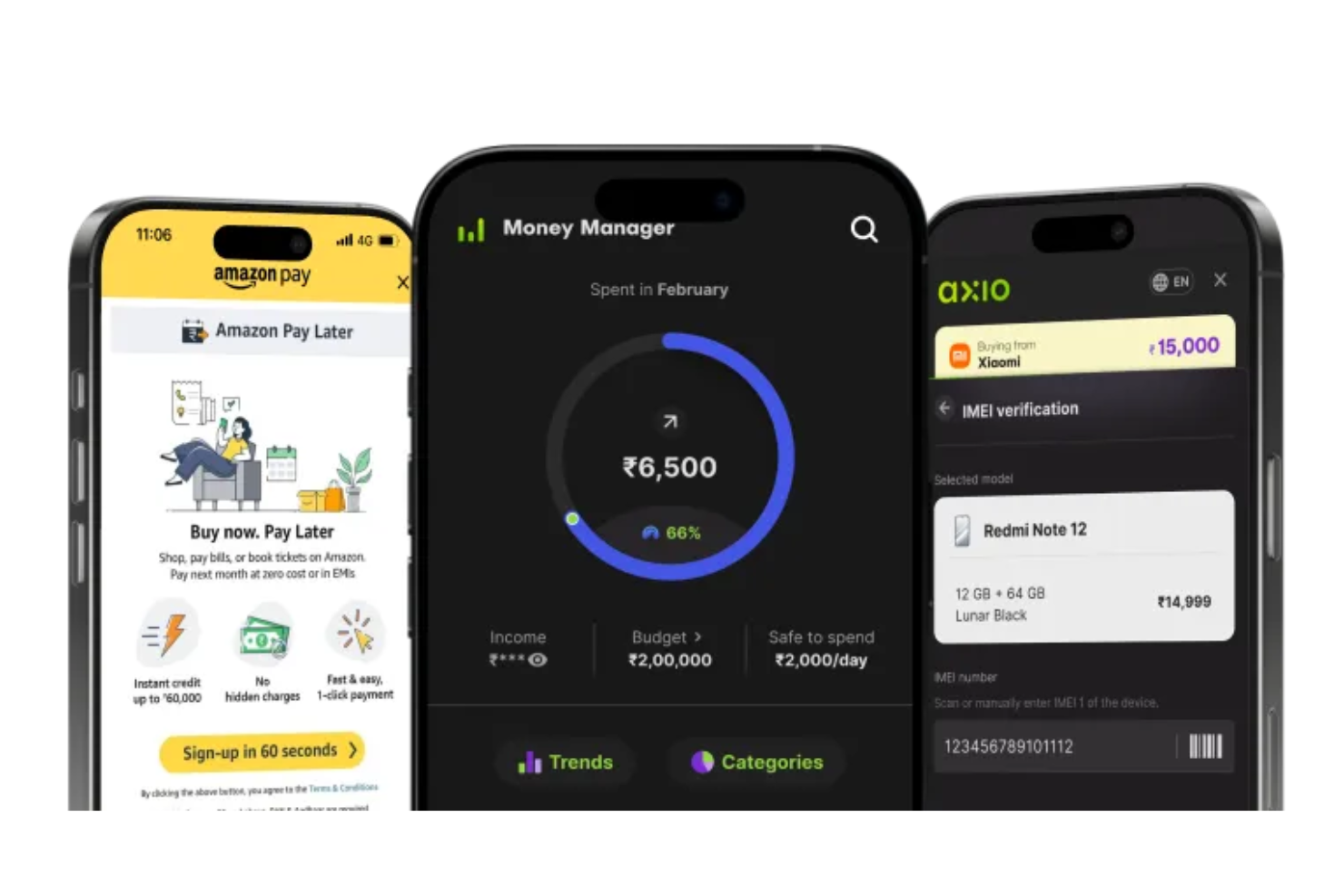

For businesses focused on the Indian market, axio offers installment-based payment solutions tailored to local consumer needs. This platform is especially relevant for e-commerce retailers and merchants looking to provide flexible pay-later options at checkout. Unlike Affirm and other global providers, axio specializes in India-specific credit products and integrations with major Indian payment networks.

Why axio Is a Good Affirm Alternative

If your business serves customers in India, axio stands out for its focus on installment services designed specifically for the Indian market. I picked axio because it offers pay-later and EMI options that align with local consumer credit habits and regulatory requirements. The platform supports instant credit decisions and integrates with major Indian payment gateways, making it easy to offer flexible financing at checkout. This local specialization gives axio an edge over global providers like Affirm when it comes to meeting the needs of Indian merchants and shoppers.

axio Key Features

Some other features worth noting include:

- Customizable Repayment Schedules: Merchants can configure repayment timelines to match their business model.

- Automated KYC Verification: The platform handles digital identity checks for faster onboarding.

- White-Label Branding Options: Businesses can present axio’s services under their own brand.

- Detailed Transaction Analytics: Access real-time data on installment usage and customer payment behavior.

axio Integrations

Native integrations are not currently listed.

Pros and Cons

Pros:

- White-label branding for merchant flexibility

- Instant digital KYC for customer onboarding

- EMI options tailored for Indian consumers

Cons:

- Limited public documentation for developers

- Only available for India-based merchants

Retailers and e-commerce businesses looking to serve customers across Saudi Arabia, the UAE, and the wider Middle East often turn to Tamara for localized buy now, pay later solutions. Tamara stands out by supporting Arabic language, regional payment methods, and compliance with local regulations, making it a strong fit for merchants targeting this market. Unlike Affirm, Tamara is purpose-built for the unique needs and preferences of Middle Eastern shoppers and businesses.

Why Tamara Is a Good Affirm Alternative

For businesses focused on the Middle East, Tamara offers a level of regional coverage that Affirm doesn’t match. I picked Tamara because it supports Arabic language interfaces and works with popular local payment methods like Mada and Tabby, which are essential for serving customers in Saudi Arabia and the UAE. The platform also complies with local financial regulations, helping merchants avoid compliance headaches. These features make Tamara a strong choice for retailers and e-commerce brands looking to build trust and drive conversions in Middle Eastern markets.

Tamara Key Features

Some other Tamara features worth noting include:

- Split Payment Option: Customers can divide purchases into multiple payments at checkout.

- Merchant Portal: Businesses get access to a dashboard for tracking transactions and settlements.

- Automated Settlement Process: Funds are transferred to merchants automatically on a set schedule.

- Order Management Tools: Merchants can view, manage, and refund orders directly within the platform.

Tamara Integrations

Integrations include Shopify, WooCommerce, Magento, Salla, Zid, Paymob, Salesforce Commerce Cloud, and more.

Pros and Cons

Pros:

- Dedicated support for Saudi and UAE businesses

- Fast onboarding for Middle East merchants

- Local payment methods like Mada accepted

Cons:

- Merchant dashboard lacks advanced analytics

- Limited installment plan flexibility reported

Synchrony’s Pay Later solution is designed for retailers and brands that want to offer integrated financing options at checkout, both online and in-store. This platform appeals to businesses looking for a single provider that can support revolving credit, installment loans, and promotional financing under one roof. Unlike Affirm, Synchrony specializes in embedding financing directly into the store experience, helping merchants manage everything from application to payment processing within their own ecosystem.

Why Synchrony Is a Good Affirm Alternative

For businesses that want financing deeply embedded in their store experience, Synchrony offers a level of integration that Affirm doesn’t match. I picked Synchrony because it supports revolving credit, installment loans, and promotional financing all within a single platform. Merchants can manage customer applications, approvals, and payments directly through Synchrony’s system, keeping the financing process closely tied to their brand. This approach is especially useful for retailers who want to offer flexible payment options without sending customers to a third-party site.

Synchrony Key Features

Some other Synchrony features worth highlighting include:

- Customizable Financing Promotions: Merchants can set up special financing offers tailored to specific products or sales events.

- Omnichannel Application Process: Customers can apply for financing both online and in-store using the same system.

- Fraud Detection Tools: Built-in risk management features help identify and prevent fraudulent transactions.

- Dedicated Merchant Support Portal: Access resources, training, and support for managing financing programs.

Synchrony Integrations

Native integrations are not currently listed.

Pros and Cons

Pros:

- Customizable promotional financing for merchants

- In-store and online financing application options

- Offers both revolving credit and installment loans

Cons:

- Application process may redirect customers offsite

- Consumer credit checks required for most products

Other Affirm Alternatives

Here are some additional Affirm alternatives that didn’t make it onto my shortlist, but are still worth checking out:

- equipifi

With banking core integration

- HES FinTech

For customizable white-label solutions

- commercetools

With modular commerce integrations

- TransUnion

For credit risk assessment tools

{kind=link}

Affirm Alternatives Selection Criteria

When selecting the best Affirm alternatives to include in this list, I considered common buyer needs and pain points related to financial technology service products, like offering flexible payment options and ensuring fast, reliable credit decisions. I also used the following framework to keep my evaluation structured and fair:

Core Functionality (25% of total score)

To be considered for inclusion in this list, each solution had to fulfill these common use cases:

- Offer buy now pay later options

- Provide instant credit decisioning

- Integrate with e-commerce platforms

- Support multiple payment methods

- Manage customer repayment schedules

Additional Standout Features (25% of total score)

To help further narrow down the competition, I also looked for unique features, such as:

- White-label branding capabilities

- Automated KYC verification

- Advanced fraud detection tools

- Customizable installment plans

- Real-time transaction analytics

Usability (10% of total score)

To get a sense of the usability of each system, I considered the following:

- Simple and intuitive user interface

- Clear navigation for merchants and customers

- Responsive design for mobile and desktop

- Minimal steps to complete transactions

- Accessible dashboard for monitoring activity

Onboarding (10% of total score)

To evaluate the onboarding experience for each platform, I considered the following:

- Availability of training videos and guides

- Step-by-step product tours

- Pre-built templates for quick setup

- Access to onboarding webinars

- In-app chatbots for real-time help

Customer Support (10% of total score)

To assess each software provider’s customer support services, I considered the following:

- 24/7 support availability

- Multiple support channels offered

- Fast response times to inquiries

- Access to a knowledge base

- Dedicated account management

Value For Money (10% of total score)

To evaluate the value for money of each platform, I considered the following:

- Transparent pricing structure

- Flexible contract terms

- No hidden fees or charges

- Discounts for annual billing

- Features included at each price tier

Customer Reviews (10% of total score)

To get a sense of overall customer satisfaction, I considered the following when reading customer reviews:

- Positive feedback on reliability

- Reports of successful integrations

- Satisfaction with customer support

- Ease of implementation experiences

- Value delivered compared to cost

Why Look For An Affirm Alternative?

While Affirm is a good choice of financial technology service, there are a number of reasons why some users seek out alternative solutions. You might be looking for an Affirm alternative because…

- You need support for markets outside the US

- Your business requires more flexible installment plans

- You want white-label branding for your checkout

- You need deeper integration with local payment gateways

- Your customers expect faster credit decisioning

- You want more transparent or negotiable pricing

If any of these sound like you, you’ve come to the right place. My list contains several financial technology service options that are better suited for teams facing these challenges with Affirm and looking for alternative solutions.

Affirm Key Features

Here are some of the key features of Affirm, to help you contrast and compare what alternative solutions offer:

- Buy now, pay later installment plans

- Instant credit decisioning at checkout

- No late or hidden fees for customers

- Integration with major e-commerce platforms

- Customizable payment terms for merchants

- Real-time fraud detection and risk assessment

- Transparent pricing and merchant fees

- In-app and online account management for customers

- Automated repayment scheduling and reminders

- Support for both online and in-store purchases