28 Best UK Payment Gateways Providers in 2026

The Top 10 Payment Gateway Providers for the UK

Selling in the UK? This guide helps you choose a payment gateway fast.

I focus on the levers that move revenue: approval rates, clean checkout UX, PCI DSS compliance, fraud prevention, and transparent pricing—transaction fees, monthly fees, chargebacks, and cross-border costs.

If you’re multichannel, I cover online, POS, and mobile so you don’t bolt together a fragile payment system.

I evaluate providers on core functionality (card payments, digital wallets, bank transfers), multi-currency and international payments, payout speed, refund handling, and real-time reporting.

I also look at API quality and integrations with Shopify, Magento, and WooCommerce—plus support that actually answers when volume spikes. I’ve been in the retail and ecommerce space for over a decade. So, I know that without the right payments infrastructure, you’re struggling.

Why Trust Our Software Reviews

We’ve been testing and reviewing retail and ecommerce software and services since 2021.

As retail experts ourselves, we know how critical and difficult it is to make the right decision when selecting software. We invest in deep research to help our audience make better software purchasing decisions.

We’ve tested more than 2,000 tools for different finance and accounting use cases and written over 1,000 comprehensive software reviews. Learn how we stay transparent and our review methodology.

Comparing the Best UK Payment Gateway Providers, Side-by-Side

Use this chart to scan pricing, trial availability, and each provider’s “best for” so you can shortlist fast.

| Tool | Best For | Trial Info | Price | ||

|---|---|---|---|---|---|

| 1 | Best for secure transactions | Free consultation available | Pricing upon request | Website | |

| 2 | Best for currency exchange | Free plan available | From $9.99/month | Website | |

| 3 | Best for mobile payments | Free demo available | From 3.25% plus $0.15 per transaction | Website | |

| 4 | Best for European markets | Free demo available | From £29/month + £0.10/transaction | Website | |

| 5 | Best for small businesses | Free plan available | From $20/user/month (billed annually) | Website | |

| 6 | Best for card processing | Free demo available | Pricing upon request | Website | |

| 7 | Best for large enterprises | Free demo available | Pricing available upon request | Website | |

| 8 | Best for global reach | Not available | Pricing upon request | Website | |

| 9 | Best for cryptocurrency support | Free demo available | Pricing upon request | Website | |

| 10 | Best for easy integration | Free demo available | From £0.01/transaction | Website |

The 10 Best Payment Gateway Providers for the UK, Reviewed

These reviews focus on what operators need: payment methods, checkout, fraud tools, payouts, integrations, and the costs you’ll actually pay.

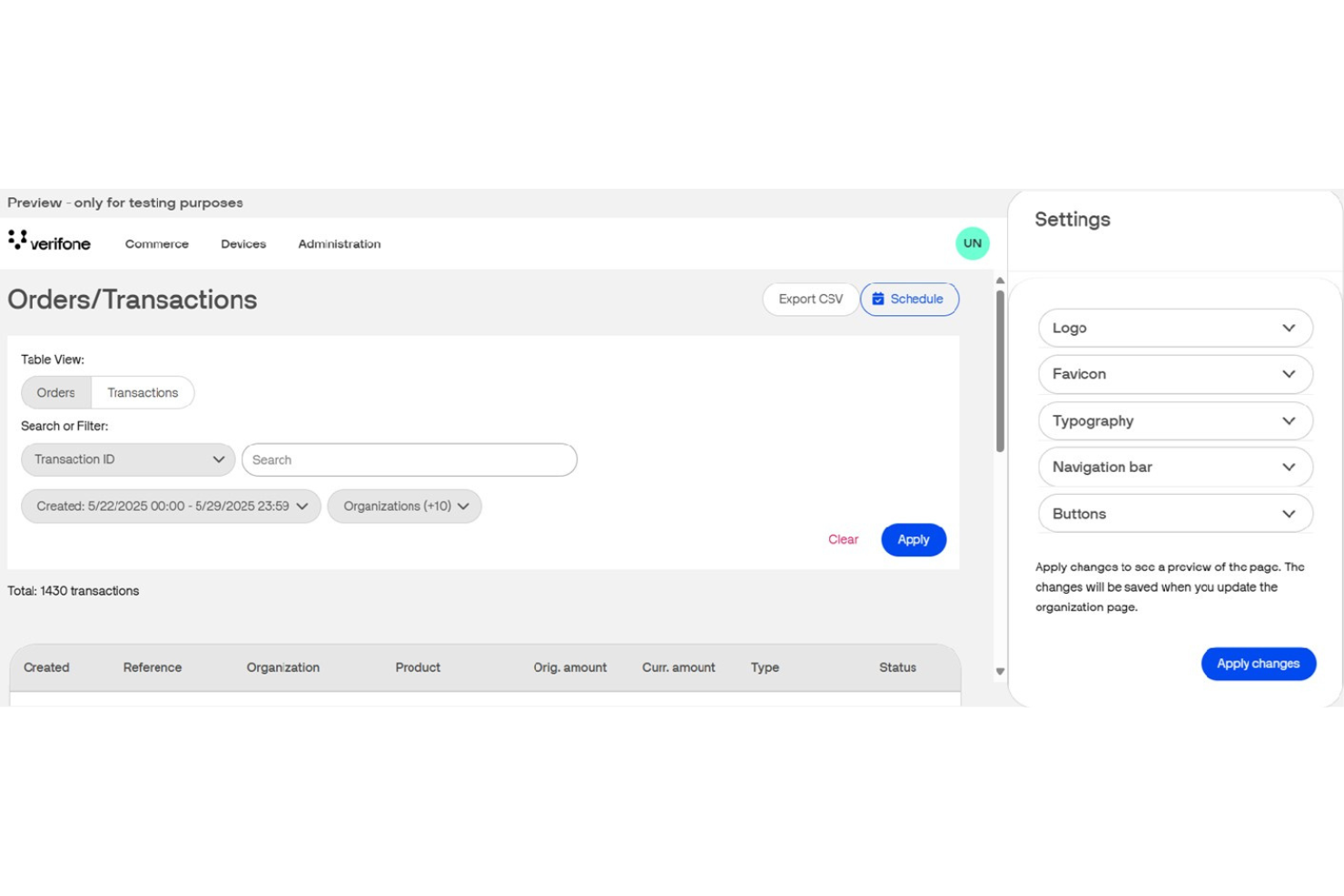

Verifone is a payment gateway solution focused on providing secure transaction processing for businesses across various sectors. It caters to enterprises looking for reliable payment solutions with a strong emphasis on security.

Why I picked Verifone: This UK payment gateway provider is recognised for its strong security measures that safeguard transactions and customer data. It supports EMV and NFC technologies, enabling UK businesses to process modern payment methods with confidence. With advanced fraud prevention tools and a customizable checkout interface, Verifone helps organisations reduce risk while tailoring the payment experience to their needs.

Standout features & integrations:

Features include advanced encryption that safeguards sensitive payment information. The platform provides comprehensive transaction monitoring, helping you keep track of payment activities. Verifone also offers multichannel payment solutions, allowing your team to accept payments online, in-store, and on mobile.

Integrations include Shopify, WooCommerce, Magento, PrestaShop, BigCommerce, Salesforce, SAP, Oracle, QuickBooks, and OpenCart.

Pros and Cons

Pros:

- Customizable payment interface

- Effective fraud prevention

- Support for EMV and NFC

Cons:

- Higher transaction fees

- Complex initial setup

Revolut is a versatile payment gateway solution designed for businesses that require efficient currency exchange capabilities. It serves companies looking to manage transactions and operations across multiple currencies seamlessly.

Why I picked Revolut: This UK payment gateway provider stands out for its competitive currency exchange and multi-currency accounts, helping businesses manage international payments with ease. Real-time exchange rates give UK companies up-to-date information to handle cross-border transactions efficiently. Its user-friendly interface simplifies payment management, making Revolut a strong choice for businesses expanding beyond the UK.

Standout features & integrations:

Features include a built-in budgeting tool that helps you track spending and manage finances. The platform supports instant transaction notifications, so you're always informed about your account activities. Revolut also offers virtual cards for added security in online transactions.

Integrations include Shopify, WooCommerce, Magento, PrestaShop, BigCommerce, Salesforce, SAP, Oracle, QuickBooks, and OpenCart.

Pros and Cons

Pros:

- Real-time exchange rate updates

- Multi-currency account support

- Competitive currency exchange rates

Cons:

- Higher fees for certain transactions

- Limited offline payment options

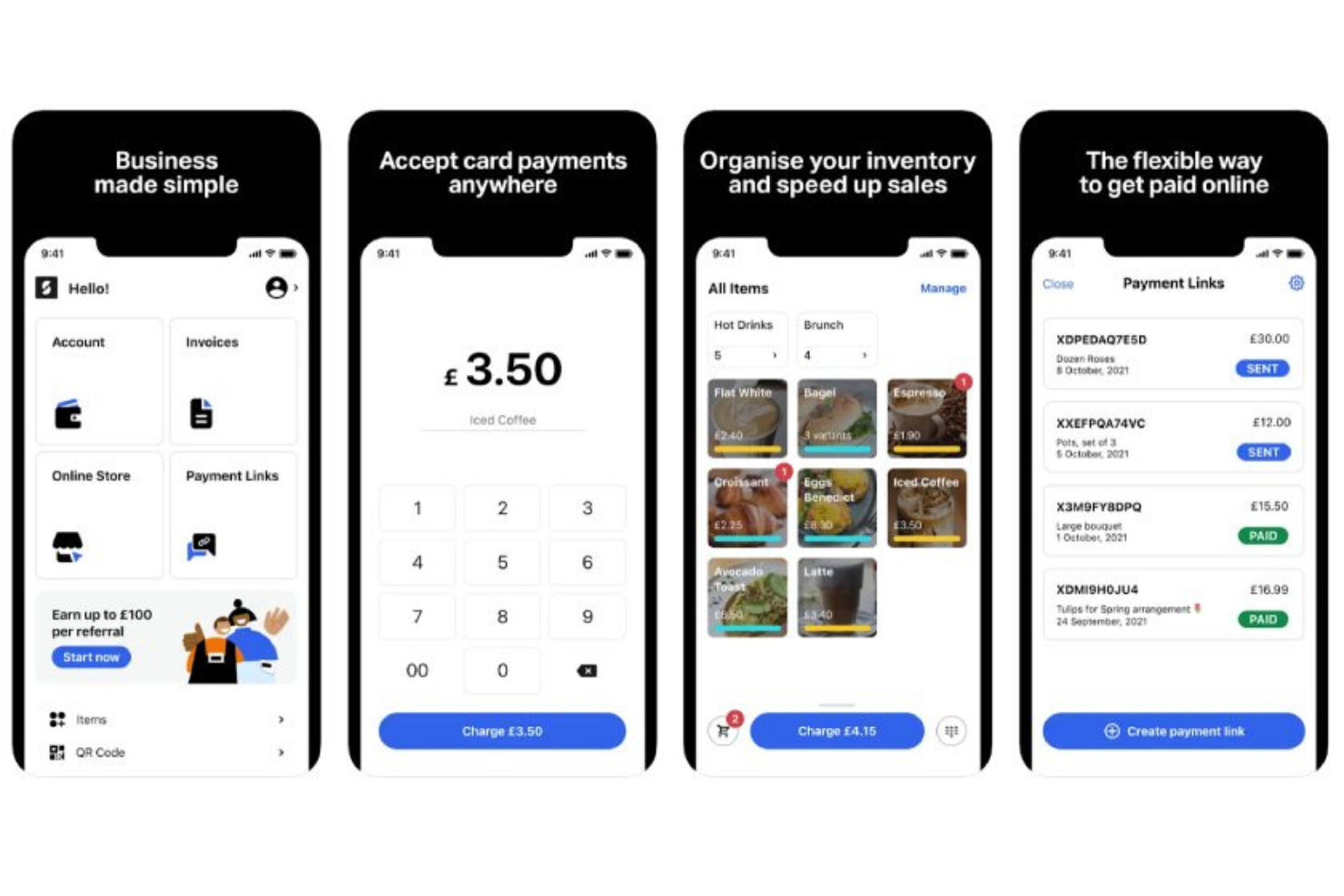

SumUp is a payment gateway solution tailored for businesses seeking efficient mobile payment processing. It primarily serves small to medium-sized enterprises that need a convenient way to handle transactions on the go.

Why I picked SumUp: This UK payment gateway provider is well known for mobile payments, offering portable card readers that connect easily to smartphones. It provides competitive transaction fees, making it a cost-effective option for small UK businesses. With a simple setup process, SumUp enables merchants to start accepting payments quickly, which is ideal for mobile and on-the-go operations.

Standout features & integrations:

Features include a virtual terminal that allows you to take payments over the phone. The platform also supports invoicing, enabling you to send professional-looking invoices directly to your clients. SumUp offers a dashboard for tracking sales and managing business performance, which is essential for busy entrepreneurs.

Integrations include Shopify, WooCommerce, Magento, PrestaShop, BigCommerce, Salesforce, SAP, Oracle, QuickBooks, and OpenCart.

Pros and Cons

Pros:

- Supports phone payments

- Competitive transaction fees

- Portable card reader options

Cons:

- Higher fees for international transactions

- Requires smartphone connectivity

Worldline is an online payment gateway solution designed for merchants across various sectors, including retail and digital goods. It supports multiple payment methods and enhances transaction security, making it ideal for businesses operating in European markets.

Why I picked Worldline: Worldline is tailored for European markets with its support for local and international payment methods. It offers advanced fraud management tools to secure your transactions. Features like one-click payments via tokenization provide convenience for your customers. The merchant portal allows you to track transactions and gain insights into payment performance.

Standout features & integrations:

Features include a business intelligence tool that helps you analyze transaction data. The Pay by Link feature allows you to send payment requests via email or text. Worldline also offers solutions for recurring payments, which can be beneficial for subscription-based services.

Integrations include Shopify, Magento, WooCommerce, PrestaShop, BigCommerce, Salesforce, SAP, Oracle, QuickBooks, and OpenCart.

Pros and Cons

Pros:

- Supports recurring payments

- One-click payment option

- Strong European market focus

Cons:

- Higher transaction fees

- Complex integration process

Elavon is a UK payment gateway provider that supports small businesses with reliable online transaction tools and payment acceptance services. It is designed to help smaller enterprises across the UK manage payments efficiently, offering straightforward solutions that reduce complexity and ensure smooth operations.

Why I picked Elavon: This gateway provides simple setup and transparent pricing tailored to UK businesses. Its virtual terminal and mobile payment options allow payments to be accepted anywhere, making it ideal for smaller teams with limited resources. With reporting tools to track transactions and fraud management features for added protection, Elavon helps UK businesses maintain secure payments and steady cash flow.

Standout features & integrations:

Features include a virtual terminal that allows you to process payments without a physical card reader. The mobile app lets your team accept payments on the go, which is ideal for businesses without a fixed location. Additionally, the platform offers detailed reporting tools to help you track and analyze your transactions.

Integrations include Shopify, WooCommerce, Magento, PrestaShop, BigCommerce, OpenCart, SAP, Oracle, QuickBooks, and Salesforce.

Pros and Cons

Pros:

- Effective fraud management

- Mobile payment options

- Easy setup process

Cons:

- Higher transaction fees

- Limited advanced features

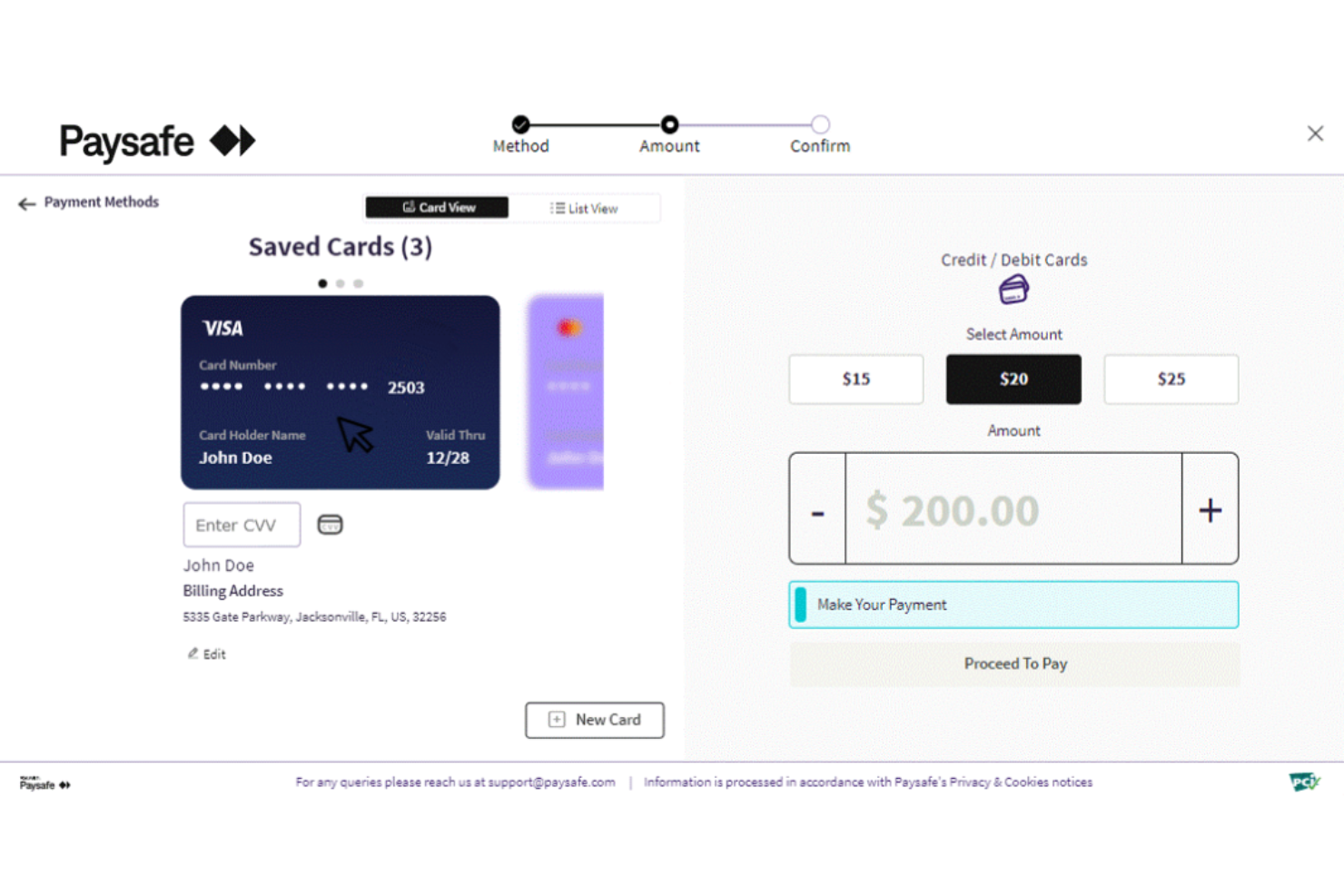

Paysafe is a payment gateway solution focused on card processing, catering to businesses that require efficient and secure transaction handling. It serves various industries, providing essential tools to manage credit card payments and related services.

Why I picked Paysafe: This UK payment gateway provider is known for strong card processing and a wide range of supported payment methods. It offers advanced fraud protection and secure transaction handling, giving UK businesses confidence in their payment operations. Flexible payment options and detailed reporting tools help organisations meet customer needs while maintaining full visibility over transactions.

Standout features & integrations:

Features include an easy-to-use virtual terminal for processing payments without a physical card reader. The platform supports recurring billing, which is great for subscription-based businesses. You also have access to detailed transaction reports that help you keep track of your financial performance.

Integrations include Shopify, WooCommerce, Magento, PrestaShop, BigCommerce, Salesforce, SAP, Oracle, QuickBooks, and OpenCart.

Pros and Cons

Pros:

- Advanced reporting tools

- Strong fraud protection

- Wide range of payment methods

Cons:

- Requires technical support

- Limited global reach

Global Payments is a leading UK payment gateway provider designed for large enterprises, offering robust tools to manage online transactions at scale. It supports UK businesses that require enterprise-level solutions to process high volumes of payments efficiently, both domestically and across international markets.

Why I picked Global Payments: This gateway is built for large UK enterprises, providing scalable infrastructure and reliable multi-currency support. Its advanced analytics tools help businesses make data-driven decisions while managing complex payment flows. With strong security and compliance features, it ensures safe and seamless transactions for organisations operating at scale.

Standout features & integrations:

Features include advanced fraud detection that helps safeguard your transactions. The platform's robust reporting tools offer insights into payment trends and performance. You also get 24/7 customer support, ensuring your operations run smoothly at all times.

Integrations include Salesforce, SAP, Oracle, Shopify, Magento, WooCommerce, BigCommerce, PrestaShop, QuickBooks, and OpenCart.

Pros and Cons

Pros:

- Advanced security measures

- Multi-currency support

- Extensive global reach

Cons:

- Higher monthly fees

- Complex setup process

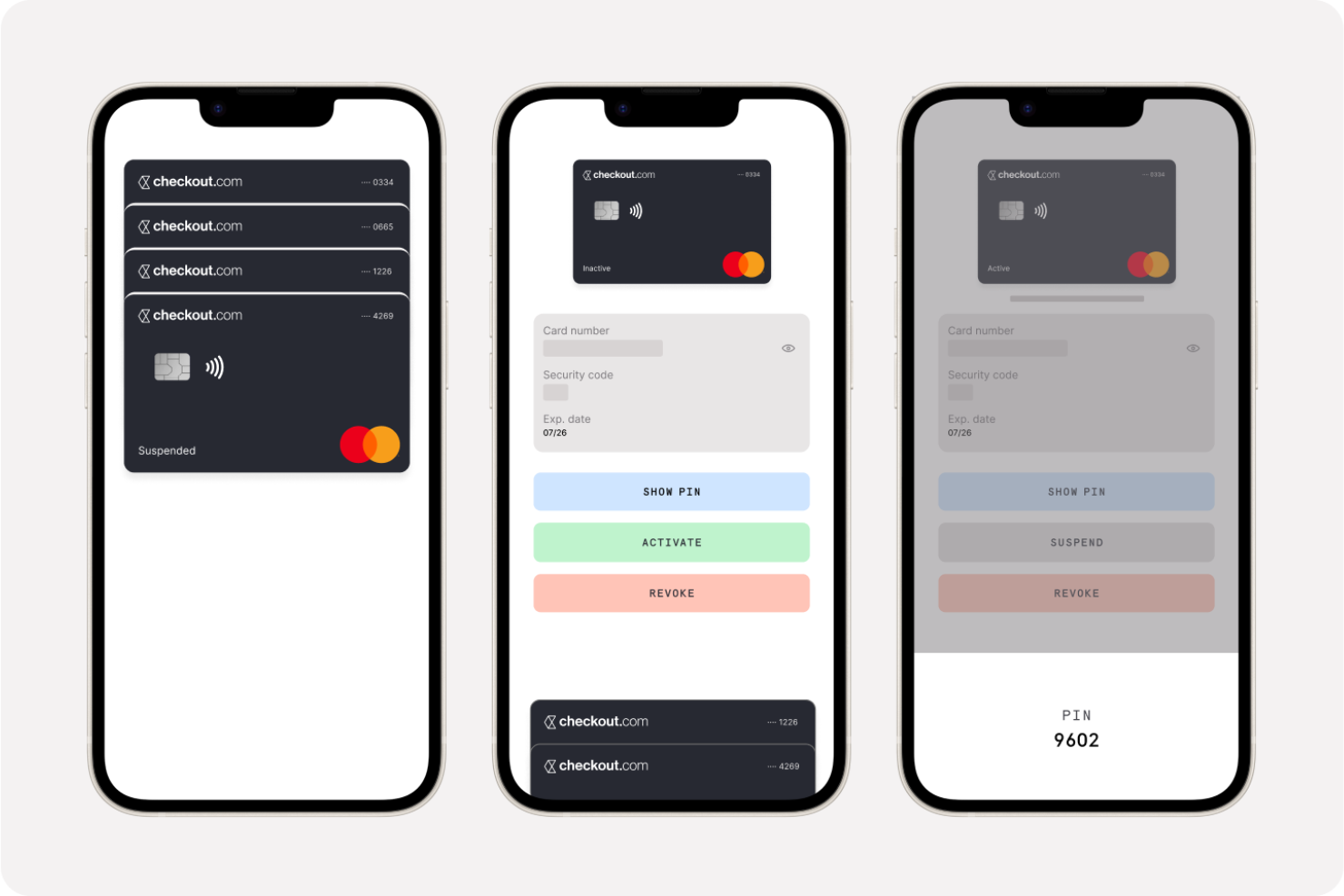

Checkout.com is a global payment processing platform designed for businesses to accept online payments through websites and mobile apps. It primarily serves ecommerce, fintech, and other industries looking for international payment solutions.

Why I picked Checkout.com: This gateway offers strong UK and European coverage with local acquiring and support for international payment methods. Its unified payments API lets UK businesses customize payment flows while staying compliant with domestic and cross-border rules. Advanced fraud protection, dispute management, and AI-driven acceptance ensure secure and high-performing transactions.

Standout features & integrations:

Features include a centralized dashboard for comprehensive money management. You can also benefit from mobile SDKs for native checkouts and hosted payment pages. The platform provides payment links for various channels, making it versatile for different customer preferences.

Integrations include WooCommerce, Shopify, Magento, BigCommerce, Salesforce, PrestaShop, OpenCart, SAP, Oracle, and QuickBooks.

Pros and Cons

Pros:

- Real-time transaction updates

- Customizable payment flows

- Global payment coverage

Cons:

- Limited cryptocurrency support

- Limited customer support hours

Nuvei is a UK payment gateway provider that supports diverse payment methods, including cryptocurrency. It helps enterprises expand their payment options and reach broader customer bases in the UK and internationally.

Why I picked Nuvei: This gateway stands out for enabling cryptocurrency transactions, giving UK businesses an edge in digital payments. Its multi-currency processing supports companies with international customers. Risk management tools and a customizable checkout ensure secure, flexible transactions that improve the customer experience.

Standout features & integrations:

Features include a global payouts service that allows you to send payments worldwide. The platform's chargeback management system helps you handle disputes efficiently. You can also access a detailed reporting suite to monitor your transaction data.

Integrations include Shopify, WooCommerce, Magento, Salesforce, PrestaShop, BigCommerce, SAP, Oracle, QuickBooks, and OpenCart.

Pros and Cons

Pros:

- Efficient chargeback management

- Customizable checkout

- Multi-currency processing

Cons:

- Requires technical expertise

- Limited customer support hours

Viva.com is a UK payment gateway provider designed to give businesses simple integration with their existing systems. It primarily supports small to medium-sized enterprises across the UK that want to improve their online payment processing capabilities.

Why I picked Viva.com: This UK payment gateway provider simplifies integration, making it accessible for businesses with limited technical resources. Its user-friendly API allows teams to quickly manage payments, while support for multiple payment methods gives customers more flexibility. Real-time reporting tools provide insights into transactions, helping UK businesses optimise operations and maintain control.

Standout features & integrations:

Features include a virtual terminal that lets you process payments without a physical card reader. The platform supports recurring billing, which is ideal for subscription services. You can also access detailed transaction reports, helping you monitor your financial performance.

Integrations include Shopify, WooCommerce, Magento, PrestaShop, BigCommerce, Salesforce, SAP, Oracle, QuickBooks, and OpenCart.

Pros and Cons

Pros:

- Real-time reporting features

- Supports multiple payment methods

- User-friendly API

Cons:

- Higher fees for certain transactions

- Limited advanced features

Other UK Payment Gateway Providers

Here are some additional payment gateway providers for the UK that didn’t make it onto my shortlist, but are still worth checking out:

- Rapyd.net

For local payments

- Cashflows

For flexible payments

- Stripe

For developer-friendly tools

- PayPal

For global brand recognition

- Braintree

For integration with PayPal

- Adyen

For omnichannel payments

- Cybersource

For fraud management

- Amazon Pay

For Amazon shoppers

- Worldpay

For multi-currency support

- Shopify Payments

For Shopify stores

- Square

For small business tools

- Mollie

For easy setup

- APEXX Global

For payment optimization

- CardStream

For white-label solutions

- Ecommpay

For custom payment solutions

- Trust Payments

For regulated industries

- DNA Payments

For flexible payment options

- Lloyds Bank Cardnet

For UK-based businesses

{kind=link}

How I Evaluate Payment Gateway Providers UK

I look at every UK payment gateway through two lenses: the non-negotiable baseline—FCA authorization, omnichannel acceptance, PCI-DSS compliance—and the differentiators that set the best apart.

Core Functionality (Table Stakes For This List)

When I'm selecting tools for my list, I rank each one on a scale from 0 (does not offer the functionality) to 5 (excels in this area) for each core functionality listed below. Then, I calculate the tool's total score into a percentage. Each tool needs to achieve a minimum total score of 65% to be considered for inclusion.

- UK Payment Processing: I check whether a provider settles in GBP to UK bank accounts and holds FCA authorization or partners with an FCA-regulated acquirer for direct domestic acquiring.

- Omnichannel Acceptance: Retailers selling across countertop tills, online stores, and mobile need unified acceptance, so I evaluate whether each gateway covers card-present, ecommerce, and MOTO channels.

- PCI-DSS Compliance & Security: I look for PCI-DSS Level 1 certification, tokenization, and 3D Secure 2 support to confirm the provider can handle SCA requirements under UK regulations.

- Multi-Method Payment Support: Beyond Visa and Mastercard, I evaluate whether providers accept Apple Pay, Google Pay, and at least one alternative method like Klarna or open banking at checkout.

- Retail System Integrations: Whether you're running Shopify, Magento, or WooCommerce alongside a POS like Zettle or Lightspeed, I look for documented prebuilt connectors and well-maintained APIs.

- Multi-Currency & International Acceptance: For UK retailers selling cross-border, I evaluate currency coverage, dynamic currency conversion options, and whether the gateway supports local acquiring in key markets.

Once I have a list of tools that meet this criteria, I consider what sets each platform apart.

Differentiating Factors (What Sets Vendors Apart)

Here's how I compare and contrast different vendors:

Standout Features

Smart transaction routing matters for high-volume retailers because it directs each payment through the acquirer most likely to approve it, reducing declines during peak periods like Black Friday. I also evaluate whether a gateway offers a unified reporting dashboard that reconciles in-store and online transactions in one view, which multi-store finance controllers rely on for end-of-day balancing. Settlement speed is another differentiator. Providers offering next-day or instant GBP payouts give independent retailers much better control over working capital.

Beyond Features

Pricing transparency is one of the first things I evaluate. I check whether a provider clearly discloses its model—interchange-plus vs. blended—and whether PCI fees or chargeback penalties are buried in the terms. Uptime reliability carries real weight too. A gateway outage on Boxing Day can cost a retailer thousands, so I look for published SLAs and transparent incident histories. I also consider how each provider handles SCA compliance under PSD2. UK retailers need automated dispute workflows and representment tools to keep their chargeback ratios healthy.

What Are UK Payment Gateway Providers?

UK payment gateway providers are services that connect your online store or app to card networks and banks to authorize, capture, and settle payments.

They route card payments, digital wallets, and bank transfers; support recurring payments; enforce SCA and PCI DSS compliance; and layer in fraud prevention and chargeback tools.

For UK retailers and ecommerce teams, gateways power checkout, enable multi-currency and international payments, and—when paired with a processor/acquirer—bridge online and in-person POS.

Most offer APIs, hosted payment pages, payment links, and real-time dashboards for refunds, payouts, and reconciliation.

Pick the right one and you’ll raise approval rates, trim processing fees, speed up payouts, and protect cash flow with clearer pricing and better visibility.

How to Choose a UK Payment Gateway Provider

Start with your real payment mix and cash flow, then pressure-test pricing, approvals, fraud, and the API. The right UK payment gateway should lift checkout conversion, keep PCI DSS/SCA tight, and make payouts predictable across ecommerce, POS, and mobile.

| Step | What to check | Pro tip |

|---|---|---|

| Map your payment flows end to end | Online, in-person, subscriptions, refunds, partials, international payments | Sketch the happy path and the edge cases before you shortlist |

| Match payment methods to customers | Cards, digital wallets, bank transfers, direct debit, buy now/pay later | Use actual tender data; don’t add methods your shoppers won’t use |

| Pressure-test approval rates | Authorization benchmarks by market, MCC, and AOV | Ask for UK/EU rates and 3-D Secure orchestration options |

| Model total cost, not just the headline | Blended vs interchange++, transaction fees, monthly fees, chargebacks, FX | Run a 3-month scenario with your real volume and mix |

| Lock down payout timing | Settlement schedule, next-day options, weekends/holidays handling | Confirm cut-off times and bank holidays in the United Kingdom |

| Set your fraud posture | Risk scoring, rules, machine learning, alerts, chargeback tools | Start conservative, then tune after 2–4 weeks of real data |

| Define compliance scope early | PCI DSS level, SCA flows, tokenization, data retention | Minimize PCI scope with hosted fields or a hosted payment page |

| Test the API like an engineer | Docs, SDKs, webhooks, rate limits, sandbox realism | Build a tiny checkout, then break it; judge error clarity and logs |

| Verify integrations you’ll rely on | Shopify, WooCommerce, Magento, accounting, POS systems | Check native apps, version support, and who owns maintenance |

| Check reporting and reconciliation | Real-time dashboard, exports, payouts vs deposits, fee line items | Download sample reports and reconcile a mock month |

| Trial the checkout UX | Load time, mobile UX, accessibility, localization, multi-currency | A/B your current payment page vs the new flow for a week |

| Nail the contract and support | Term length, minimums, SLAs, status page, escalation path | Ask for a named account manager once you hit target volume |

Features of UK Payment Gateway Providers

Pick features that raise approval rates, cut fees, and keep you compliant across ecommerce and POS. The best UK payment providers make checkout clean, reporting reliable, and payouts predictable.

- Broad payment methods. Accept credit cards, debit cards, Apple Pay, Google Pay, PayPal, bank transfers, and direct debit.

- Strong SCA and PCI DSS. Handle PSD2 with 3-D Secure 2, exemptions, and tokenization while reducing your compliance scope.

- Recurring and subscriptions. Support retries, dunning, proration, and account updaters to protect subscription revenue.

- Fraud prevention. Combine rules, device signals, and risk scoring with clear controls for chargeback reduction.

- Checkout flexibility. Use hosted payment pages, drop-in UI, or API-led custom flows that keep UX fast on mobile.

- Multichannel support. Run online, in-person, and mobile payments with one dashboard and unified settlement.

- International and multi-currency. Price in GBP while settling cleanly across EUR, USD, and more with transparent FX.

- Real-time reporting. Get live dashboards, exportable fee line items, and payout reconciliation your finance team trusts.

- Developer-ready APIs. Rely on good docs, SDKs, webhooks, and a realistic sandbox that speeds up integration.

- Disputes tooling. Generate evidence packs, track outcomes, and spot patterns before they drain margin.

Benefits of UK Payment Gateway Providers

The right gateway should improve conversion today and unit economics over time. Here’s what you gain when the plumbing is right.

- Higher conversion at checkout. Faster pages, better SCA flows, and local payment options reduce abandonment.

- Lower total processing cost. Smarter routing and clear pricing help you manage transaction fees, monthly fees, and FX.

- Faster, steadier cash flow. Predictable payouts—often next-day—keep inventory and payroll on schedule.

- Less fraud and fewer chargebacks. Strong risk controls cut losses and admin time for your team.

- Cleaner ops for finance. Real-time reporting and tidy exports make reconciliation and audits straightforward.

- True multichannel visibility. One provider across ecommerce and POS simplifies settlement and support.

- Global reach without chaos. Multi-currency and international payments unlock growth while staying compliant.

- Developer velocity. Solid APIs and webhooks shorten build time and reduce brittle custom code.

- Better customer experience. Familiar payment methods and a user-friendly flow increase trust and repeat purchases.

Costs & Pricing of Payment Gateway Providers in the UK

Gateway pricing in the UK is mostly pay-as-you-go or IC++ with optional monthly fees. Model total cost using your real mix—card type, cross-border, refunds, and chargebacks—then line it up against payout timing and support.

| Plan | Average price | Common features | Best for |

|---|---|---|---|

| Pay-as-you-go | 1.4%–3.25% + £0.20–£0.25 per online card; no monthly fee | Hosted checkout, basic fraud tools, standard support | Startups and small businesses with low to moderate volume |

| Subscription (monthly) | £20–£45/month gateway; ~0.75%–1.5% + £0.05–£0.20 per transaction | Advanced reports, payment links, priority support | Growing online businesses needing predictable tools |

| Interchange++ (IC++) | Interchange + scheme fees + ~0.60%–0.80% markup + ~£0.10–£0.12 processing | Detailed fee transparency, better card routing, real-time reporting | Mid-market and multichannel retailers with higher volume |

| Enterprise custom | Quote-based IC++; typical markup ~0.30%–0.60% + ~£0.11 processing; monthly minimums apply | Dedicated account team, SLA, tailored fraud stack, premium APIs | Large retailers and high transaction volume operators |

Additional cost considerations

- Cross-border and FX. Non-GBP cards and conversions add scheme and conversion costs—model by country mix.

- Card mix matters. Commercial and Amex price higher than UK consumer Visa/Mastercard; BNPL and wallets have separate rates.

- 3-D Secure, disputes, instant payouts. Expect per-event fees (e.g., ~£0.03 per 3DS attempt, ~£15–£20 dispute fee, ~1% for instant payouts).

- Refund economics. Many keep processing fees on refunds and may charge a separate refund fee—check the policy.

- Payout speed. Next-day or same-day settlement can carry an extra fee or higher markup.

- Minimums and MMSC. Monthly minimum service charges can bite if volume dips.

- PCI scope and tools. Hosted fields or SAQ-A reduce compliance cost; some providers bill a PCI programme fee.

Implementation and add-ons. Premium support, marketplace splits, recurring billing, and advanced fraud features may be extra.

UK Payment Gateway Providers FAQs

These FAQs cut to the decisions that affect approval rates, costs, compliance, and cash flow for UK retail and ecommerce teams.

Do I need a separate merchant account or an all-in-one provider?

Both work. All-in-one payment providers (e.g., aggregators) bundle the gateway, payment processor, and merchant account—fast setup, simple pricing, less control.

A dedicated merchant account plus gateway can unlock Interchange++ (IC++), sharper pricing at scale, and more knobs for risk and routing. Under £250k annual card volume, all-in-one is usually fine.

Above that—or with complex use cases (multi-currency, in-person + online, subscriptions)—a direct merchant account often pays off.

How can I maximize approval rates in the UK and EU without wrecking checkout?

Use local acquiring, enable 3-D Secure 2 with exemptions (low-risk, TRA, trusted beneficiaries), and keep address/CVV checks tuned to your fraud profile.

Tokenize cards, use account updater, and pass the right flags for card-on-file and recurring payments. Monitor soft declines in real time, retry intelligently, and route high-risk traffic differently.

Cut friction on mobile—fast pages, clear error states, and native wallets at the top of the payment page.

What’s the difference between a gateway, a processor, and an acquirer—and why should I care?

Prevention first: strong SCA, clear descriptors, delivery confirmation, and responsive support. For representment, automate evidence packs (order info, AVS/CVV results, delivery proof, customer comms) and track win rates by reason code.

Use alerts to catch disputes before they hit. Train support to issue refunds quickly when you’re likely to lose. Watch thresholds to avoid network monitoring programs—and bake expected loss into pricing.

How should I model total cost beyond the headline rate?

Start with your mix: domestic vs cross-border, Visa/Mastercard vs Amex, debit vs credit, BNPL and wallets. Compare blended pricing to IC++ (interchange + scheme fees + markup).

Add line items: monthly fees, setup fees, PCI programme fees, refund fees (many keep the original processing fee), dispute fees, FX and conversion, payout/instant payout fees, and any monthly minimum service charge.

Run a three-month scenario using your real transaction volume.

What’s a practical chargeback strategy for UK merchants?

Prevention first: strong SCA, clear descriptors, delivery confirmation, and responsive support. For representment, automate evidence packs (order info, AVS/CVV results, delivery proof, customer comms) and track win rates by reason code.

Use alerts to catch disputes before they hit. Train support to issue refunds quickly when you’re likely to lose. Watch thresholds to avoid network monitoring programs—and bake expected loss into pricing.

Can I run multiple UK payment providers at once?

Yes—and often you should. Dual providers give you failover, better uptime, and leverage in pricing. Use smart routing to send traffic by card type, region, or risk score, and keep a backup PSP for peak trading.

Standardize your integration through your platform or a lightweight abstraction layer so reconciliation and reporting stay clean. Negotiate out of exclusivity clauses, and keep SLAs visible on your dashboard.

Pick Your Gateway, Protect Your Margin

You’ve got the shortlists, the side-by-side pricing, and the operator-grade criteria.

Now run the play: pick 2–3 UK payment gateway providers, push a real checkout test, and model total cost with your actual mix—card type, cross-border, refunds, chargebacks, and payout timing.

Don’t overthink it. Start with what your customers use, confirm the API and reporting fit your stack, then negotiate fees against volume and risk.

If you're in the process of researching payment gateway providers UK, connect with a SoftwareSelect advisor for free recommendations.

You fill out a form and have a quick chat where they get into the specifics of your needs. Then you'll get a shortlist of software to review. They'll even support you through the entire buying process, including price negotiations.

Retail never stands still—and neither should you. Subscribe to our newsletter for the latest insights, strategies, and career resources from top retail leaders shaping the industry.