30 Best Ecommerce Merchant Services Ranked for 2026

The Top 10 Ecommerce Merchant Services to Consider

Let’s see the leaderboard! Here are the best ecommerce merchant services providers and what they’re best at:

You’re here to find ecommerce merchant services that make online payments simple, secure, and cost-effective.

This guide ranks the best options for payment processing, merchant accounts, and payment gateways across credit cards, debit cards, mobile wallets, and both in-store and card-not-present checkout.

The pain points are familiar: confusing pricing, hidden fees, chargebacks, slow funding that chokes cash flow, and integrations that fight your ecommerce platform or point of sale systems.

You also need PCI compliance and fraud prevention that won’t dent conversion.

I’ve spent over a decade in ecommerce and retail—mostly back of house, inventory, warehousing, and shipping—so I judge providers on clear pricing, fast settlement by business day, reliable customer support, strong API and docs, and functionality that scales from small business to enterprise.

Use this guide three ways: scan the shortlist, compare the side-by-side chart, then dive into the picks to match a provider to your business needs.

Why Trust Our Software Reviews

Comparing the Best Ecommerce Merchant Services Side-by-Side

This table shows pricing, trial availability, and what each merchant services provider is best at—nothing else. Use it to shortlist payment processing options fast, then jump to the reviews for details.

| Service | Best For | Trial Info | Price | ||

|---|---|---|---|---|---|

| 1 | Best for steady volume merchants | Free quote available | From $99/month | Website | |

| 2 | Best for wholesale interchange pricing | 3-month free trial | From $79/month | Website | |

| 3 | Best for payments and banking | Free demo available | From 2.9% + $0.30/transaction | Website | |

| 4 | Best for local payment support | Free demo available | From 1.80% + €0.25 | Website | |

| 5 | Best for small businesses | Free consultation available | From/$49 | Website | |

| 6 | Best for secure transactions | Free demo available | From £29/month + £0.10/transaction | Website | |

| 7 | Best for emerging markets | Free consultation available | Pricing upon request | Website | |

| 8 | Best for global brands | Discovery call available | Pricing upon request | Website | |

| 9 | Best for fraud prevention | Free demo available | Pricing upon request | Website | |

| 10 | Best for online marketplaces | Free demo available | From 2.90% + $0.30/successful card transaction | Website |

The 10 Best Ecommerce Merchant Services Reviews

Below are my detailed overviews of each provider—core services, standout capabilities, and pros/cons—so you can match a payment processor to your ecommerce site and business needs.

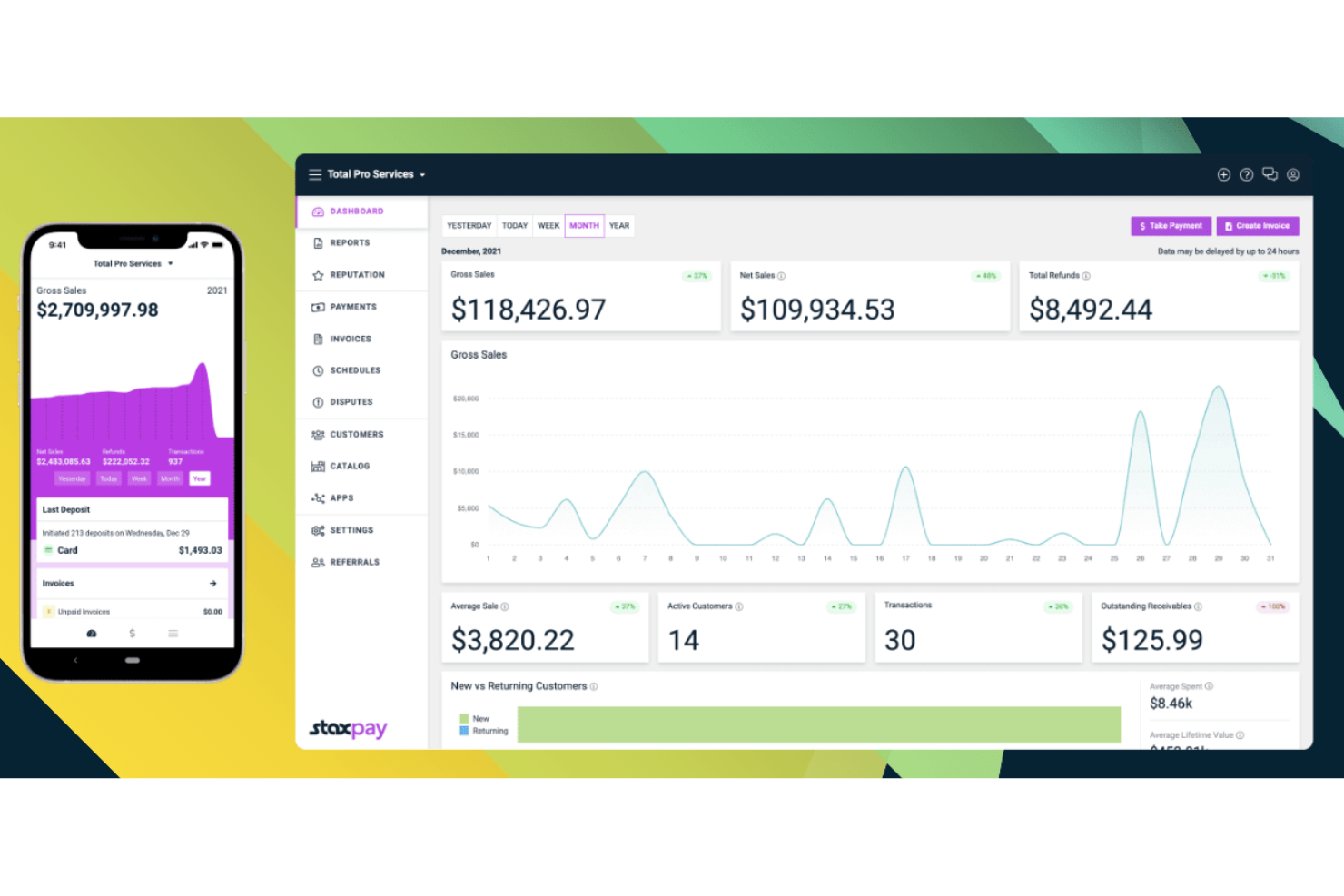

If you run an online store or an omni-channel retail business with consistent transaction volume and want a payment platform that combines card-processing, invoicing, shopping-cart/checkout tools and payment-analytics under one roof, Stax Pay gives you a single platform that fits many of those needs — whether you’re a subscription-brand owner, a retailer expanding online, or a services provider selling via recurring billing.

Why I Picked Stax Pay

I picked Stax Pay because its predictable subscription-based pricing, combined with interchange-plus (cost-plus) transaction fees, can meaningfully reduce costs — especially if your store handles a steady stream of transactions. Its ability to support both online and in-person payments, plus built-in features like hosted shopping carts and payment-links/invoicing, make it an attractive option for merchants who want a unified system that works for e-commerce and offline sales.

Stax Pay Key Features

Aside from the pricing model and core payment support, Stax Pay offers several additional features that make it well-suited for e-commerce and retail operations:

- Real-Time Reporting: Provides you with immediate access to transaction data, helping you to make informed business decisions quickly.

- Customer Management: Offers tools to manage customer information and payment preferences efficiently, enhancing the customer experience.

- Inventory and Catalog Management: Even though it’s basic, Stax Pay lets you manage catalog items and stock across online and offline channels, which helps if your business maintains both.

- Recurring Billing: Supports subscription-based models, ensuring that your business can handle regular payments seamlessly.

Stax Pay Integrations

Integrations include Shopify, WooCommerce, QuickBooks, Xero, Salesforce, Magento, BigCommerce, Stripe, PayPal, and Square.

Pros and Cons

Pros:

- Transparent subscription-plus-interchange pricing gives predictable costs.

- Supports various payment methods, including mobile processing.

- Ability to pass processing fees to customers where surcharge laws allow.

Cons:

- Next-day funding isn’t guaranteed and sometimes comes with extra cost.

- Subscription fee may outweigh savings for low-volume merchants.

New Product Updates from Stax Pay

Stax Processing: New End-to-End Payments Platform

Stax Payments introduces Stax Processing, an end-to-end payments platform offering an integrated transaction lifecycle and direct card network access. For more information, visit Stax Pay's official site.

.

.

Payment Depot offers a membership-based merchant services platform that gives e-commerce and retail sellers access to wholesale-level processing costs rather than the typical marked-up fees. If your business processes a fair volume of sales — whether online, in person, or both — this makes Payment Depot an appealing option to help you keep processing costs under control without hidden fees.

Why I Picked Payment Depot

I picked Payment Depot because it passes wholesale interchange rates directly to you rather than inflating them with percentage-based markups. Its membership (or interchange-plus) pricing model, where you pay a modest monthly (or transaction-based) fee plus actual interchange instead of a flat high-rate, can significantly lower your per-transaction cost if your volume is moderate to high. It includes essentials like a virtual terminal and online payment gateway out of the box, which means you get core e-commerce merchant services support without extra charges.

Payment Depot Key Features

In addition to its competitive pricing model, Payment Depot offers:

- Support for POS Hardware and Third-Party Terminals: You can use terminals from providers like Clover, Dejavoo or SwipeSimple — and Payment Depot supports reprogramming existing compatible hardware.

- Inventory Management: Keep track of stock levels and manage product availability directly through integrated tools.

- Invoicing: Generate and send invoices directly from the platform, simplifying the billing process.

- Recurring Billing: Automate regular payments for subscription-based services, enhancing customer experience and retention.

Payment Depot Integrations

Integrations include Clover, SwipeSimple, Vend, QuickBooks, Authorize.Net, WooCommerce, BigCommerce, Magento, Shopify, and Square.

Pros and Cons

Pros:

- 24/7 customer support provides reliable assistance for users.

- No long-term contracts offer flexibility for businesses.

- Transparent pricing with interchange-plus model attracts cost-conscious users.

Cons:

- Membership fees may be high for small or low-volume businesses.

- Not suitable for high-risk or international merchants.

Razorpay offers ecommerce merchant services that cover payment processing, banking, and payout solutions. They serve startups, small businesses, and enterprises that need flexible ways to manage online payments.

Why I picked Razorpay: Razorpay lets your team manage both payments and banking from one platform, which makes handling money simpler. You can use its APIs and no-code tools to set up custom payment flows without much effort. It also supports multiple local and global methods, giving you flexibility to serve different markets.

Standout Services: Razorpay provides payout management so your team can send money to vendors, employees, or partners quickly and track every transaction in one place. It also offers subscription billing that helps you manage recurring payments, making it easier to support membership or SaaS models.

Target industries: retail, travel, healthcare, education, and technology

Specialties: payouts, subscription billing, API integrations, local payment methods, and banking services

Pros and Cons

Pros:

- Strong API flexibility

- Useful payout features

- Wide support for local methods

Cons:

- Limited global coverage

- Support can be slow

Mollie offers ecommerce merchant services that focus on payment processing and checkout solutions. They serve small to mid-sized businesses and online retailers that need simple ways to accept payments.

Why I picked Mollie: Mollie makes it easy for your team to support local payment methods like iDEAL and Bancontact, which helps you meet customer preferences. You can set up integrations quickly with clear pricing that avoids hidden fees. It also supports subscriptions and recurring payments, making it useful if you run membership-based services.

Standout Services: Mollie provides checkout customization so your team can design payment flows that match customer needs and create smoother shopping experiences. It also offers subscription management that helps you handle recurring billing without heavy development work.

Target industries: retail, ecommerce, travel, education, and nonprofits

Specialties: local payment methods, recurring billing, checkout customization, online invoicing, and developer-friendly APIs

Pros and Cons

Pros:

- Useful for recurring billing

- Transparent pricing structure

- Strong support for local methods

Cons:

- Complex for non-European clients

- Fewer enterprise features

Chase Payment Solutions provides merchant services that cover credit and debit card processing for in-store, online, and invoicing payments. They serve small businesses in industries like retail, restaurants, and healthcare, offering solutions designed to make payment acceptance and management easier.

Why I picked Chase Payment Solutions: Chase Payment Solutions gives you same-day deposits at no extra cost, which helps your team keep cash flow steady. You can use its POS system and mobile payment tools to handle different types of sales. It also connects banking and analytics in one place, so you can manage finances more easily.

Standout Services: The point-of-sale (POS) system supports your business by offering flexible payment options and enhancing customer transactions. The advanced security features protect your payment data, ensuring secure transactions and building trust with your customers.

Target industries: Retail, restaurants, healthcare, and small businesses.

Specialties: Credit and debit card processing, same-day deposits, POS systems, mobile payment solutions, and advanced security.

Pros and Cons

Pros:

- Integrated banking and analytics

- 24/7 customer support

- Same-day deposits at no cost

Cons:

- Limited international payment options

- May not suit large enterprises

Worldline offers comprehensive e-commerce merchant services, including secure payment processing, fraud prevention, and customer insights. They cater to businesses of all sizes, providing solutions that enhance online sales and customer experiences across various global markets.

Why I picked Worldline: Worldline puts security first, which is useful if your team needs safe online payments. You can use features like dynamic currency conversion and support for many payment methods to serve different customers. It also offers local support and tailored services, so you can run operations smoothly in multiple markets.

Standout Services: The dynamic currency conversion feature allows your customers to pay in their preferred currency, enhancing their shopping experience. The 24/7 local support ensures that your team can quickly resolve any issues, maintaining smooth operations.

Target industries: Retail, ecommerce, financial services, hospitality, and travel.

Specialties: Secure payment processing, fraud prevention, customer insights, dynamic currency conversion, and localized support.

Pros and Cons

Pros:

- 24/7 local support

- Dynamic currency conversion

- Secure transaction focus

Cons:

- May not suit very small businesses

- Limited transparency on additional fees

PayU provides ecommerce merchant services with payment processing that supports multiple currencies and languages. They work with clients ranging from small businesses to large enterprises, focusing on making online payments efficient and secure across global markets.

Why I picked PayU: PayU is ideal for emerging markets due to its support for local and global payment methods, which helps your team cater to diverse customer needs. Their advanced features, like the Smart Routing Engine optimize payment flows to maximize approval rates. Additionally, PayU's emphasis on payment security and fraud protection ensures that your transactions are safe and compliant.

Standout Services: The Smart Routing Engine optimizes payment routing to increase transaction success rates, ensuring your payments are processed efficiently. The Instant Retry feature helps recover declined transactions, improving your revenue by capturing more successful payments.

Target industries: Retail, financial services, travel, telecommunications, and education.

Specialties: Payment processing, multiple currencies, Smart Routing Engine, fraud protection, and Buy Now Pay Later (BNPL).

Pros and Cons

Pros:

- Facilitates cross-border sales

- Innovative payment solutions like BNPL

- Optimizes payment approval rates

Cons:

- Limited focus outside emerging markets

- May require technical setup

Carat by Fiserv provides ecommerce merchant services that support payment processing, fraud management, and digital commerce solutions. They serve large enterprises and global retailers that need secure, flexible, and scalable transaction systems.

Why I picked Carat by Fiserv: Carat gives you a single platform for global payments, making it easier to accept transactions in different markets. Your team can use its fraud prevention tools to manage risks without slowing down checkout. It also supports cross-border payments and digital wallets, which fit well with the needs of global brands.

Standout Services: Carat offers omnichannel payment acceptance so you can handle transactions across in-store, online, and mobile channels through one system. It also provides fraud mitigation tools that let your team spot suspicious activity and protect revenue while maintaining a smooth checkout.

Target industries: retail, restaurants, travel, hospitality, and financial services

Specialties: global payments, fraud management, omnichannel commerce, digital wallets, and data-driven insights

Pros and Cons

Pros:

- Good for digital wallet adoption

- Supports complex enterprise needs

- Handles global payment methods

Cons:

- Best fit for larger scale operations

- Limited self-service resources

Cybersource offers ecommerce merchant services that cover payment processing, risk management, and digital commerce tools. They serve enterprises and online retailers that need secure and scalable systems for transactions.

Why I picked Cybersource: Cybersource gives your team advanced tools to identify and stop fraudulent activity before it impacts revenue. You can manage global payments through one platform, which helps reduce complexity across regions. It also supports digital wallets and tokenization, making it well-suited for organizations focused on fraud prevention.

Standout Services: Cybersource provides 3-D secure authentication that adds an extra layer of verification during checkout to protect your team from chargebacks. It also offers token management services that replace sensitive card details with secure tokens so you can reduce data exposure and simplify recurring billing.

Target industries: retail, travel, hospitality, financial services, and healthcare

Specialties: fraud prevention, tokenization, risk management, cross-border payments, and digital wallets

Pros and Cons

Pros:

- Flexible fraud rules engine

- Supports global operations

- Useful tokenization features

Cons:

- Learning curve for fraud tools

- Setup can be complex

BlueSnap is a Global Payment Orchestration Platform that offers services like global payment acceptance, fraud prevention, chargeback management, and compliance solutions. It serves various industries such as software, education, healthcare, retail, logistics, and manufacturing with customizable technology.

Why I picked BlueSnap: BlueSnap lets your team customize payment solutions with its modular setup, which works well for online marketplaces. You can take advantage of its global payment acceptance and fraud prevention to keep transactions secure and efficient. It also connects with more than 200 regions, helping you expand your reach worldwide.

Standout Services: The payment optimization tools help improve authorization rates and reduce costs for your business. The embedded payments solutions, such as BlueSnap Dash™ and BlueSnap Relay™, enhance your invoicing and billing processes by automating accounts receivable.

Target industries: Software, education, healthcare, retail, logistics, and manufacturing.

Specialties: Global payment acceptance, fraud prevention, chargeback management, compliance solutions, and invoicing.

Pros and Cons

Pros:

- Enhances revenue generation

- Supports multiple currencies

- Strong fraud prevention tools

Cons:

- Requires tailored solutions

- Complexity of the modular system

Other Ecommerce Merchant Services

Here are some additional ecommerce merchant services providers that didn’t make it onto my shortlist, but are still worth checking out:

- Global Payments

For large enterprises

- Checkout.com

For fast integrations

- NMI

For custom payment solutions

- Nuvei

For flexible payment options

- Stripe

For tech-focused startups

- Verifone

For secure payment terminals

- Helcim

For transparent pricing

- Braintree

For mobile app integration

- Elavon

For hospitality businesses

- Adyen

For global retail brands

- Payoneer

For freelancers and contractors

- PayPal

For quick online payments

- Amazon Pay

For Amazon shoppers

- Authorize.net

For small business security

- Stax

For subscription billing

- Worldpay

For high-volume sales

- Shopify Payments

For ecommerce websites

- Paysafe

For digital wallet options

- Square

For in-person transactions

- Rapyd

For fintech solutions

{kind=link}

Our Selection Criteria For Ecommerce Merchant Services

We score providers against real-world ecommerce needs—security, speed, and clarity—so you can choose a merchant services provider with confidence.

Core services (25% of total score)

We start with the must-haves for any ecommerce merchant account and payment processor.

- Broad payment acceptance, covering credit card payments, debit cards, wallets, and card-not-present transactions.

- Gateway and API quality, reliable payment gateway uptime, clean docs, and stable SDKs.

- Security and PCI compliance, encryption, tokenization, and 3-D Secure without wrecking checkout.

- Fraud prevention, rules plus machine learning that reduce chargeback rates.

- Multi-currency and cross-border, smooth FX, local methods, and clear settlement to your bank account.

- Recurring billing, subscription tools, dunning, and stored credentials that pass network checks.

- Omnichannel support, in-store POS, mobile payments, and a virtual terminal when needed.

- Checkout performance, strong authorization rates and fast page loads that protect conversion.

Additional standout services (25% of total score)

Then we reward functionality that moves the needle for online business growth.

- Local payment options, iDEAL, Bancontact, and regional wallets to lift acceptance.

- Payment orchestration, smart routing, retries, and network tokens to reduce declines.

- Dispute management, clear chargeback workflows and representment tools.

- Payouts and marketplaces, split payments, vendor onboarding, and compliant KYC.

- Analytics and reporting, revenue insights by channel, cohort, and payment method.

- Prebuilt integrations, apps for ecommerce platforms like Shopify and common shopping carts.

- Invoicing and virtual terminal, B2B and remote payment options without custom builds.

Industry experience (10% of total score)

We verify a track record that maps to ecommerce businesses at your stage.

- Proven scale, years operating, uptime history, and card transaction volumes handled.

- Vertical fit, retail, subscriptions, and high-risk tolerance where applicable.

- Global acquiring, regional coverage that supports international expansion.

- Certifications, compliance scope and audit cadence that reduce vendor risk.

Onboarding (10% of total score)

We favor fast, low-drama setup that doesn’t stall your launch.

- Flexible integration, no-code, low-code, and full api paths with sample apps.

- Clear documentation, sandbox access, test cards, and step-by-step guides.

- Time to live, quick merchant approval and go-live within a predictable window.

- Data migration, token vaulting and card updater support for seamless switchovers.

- Implementation help, solutions engineers and checklists that reduce surprises.

Customer support (10% of total score)

When payments break, we want real humans and real SLAs.

- 24/7 coverage, phone, chat, and email with documented response targets.

- Proactive comms, status page, incident posts, and alerts during outages.

- Dedicated care, account management for roadmap, pricing, and escalations.

- Dispute assistance, practical guidance on evidence and win rates.

Value for price (10% of total score)

We judge the total cost of acceptance—not just the headline rate.

- Transparent pricing, interchange-plus, flat rate, or subscription clearly explained.

- No hidden fees, honest terms on chargebacks, refunds, and cross-border costs.

- Contract flexibility, month-to-month options and fair termination terms.

- Cash flow impact, funding speed by business day and next-day deposit options.

- Volume breaks, predictable discounts as your ecommerce store scales.

Customer reviews (10% of total score)

Finally, we sanity-check the experience from teams like yours.

- Consistent satisfaction, themes around reliability, support quality, and ease of use.

- Real-world issues, visibility into disputes, outages, or integration friction.

- Operational fit, feedback from small business owners through enterprise operators.

What Are Ecommerce Merchant Services?

Ecommerce merchant services are the providers and tools that let an online business accept and settle payments—linking checkout, a payment gateway, and a merchant account so funds reach your bank account.

They handle credit card processing, debit cards, digital wallets, and card-not-present transactions, with support for subscriptions, mobile payments, and a virtual terminal or POS when you sell in-person.

The good ones tighten security and PCI compliance, add fraud prevention and chargeback management, and improve authorization rates.

You also get multi-currency support, payout options, clear reporting, and usable api docs to connect your ecommerce platform or shopping cart. Net result: faster funding by business day, fewer failed payments, and a simpler path to scale.

How to Choose an Ecommerce Merchant Services Provider

Use this quick path to match a merchant services provider to your online store—work the actions, then pressure-test pricing, funding, and support before you sign.

| Action | Pro tip |

|---|---|

| Map payment processing across your ecommerce website, in-store POS, and mobile; capture peak volume and risk profile. | Prioritize card-not-present checkout speed and reliability; plan for any high-risk SKUs. |

| Confirm platform fit with your shopping cart, ecommerce platforms, payment gateway, and APIs. | Run a full sandbox flow—auth, capture, refund, webhooks—and test Shopify, Stripe, PayPal, Braintree, or Authorize.net connectors. |

| Verify security and compliance for secure payment acceptance. | Require PCI compliance scope, tokenization, and 3-D Secure; ask how fraud prevention impacts conversion. |

| Model pricing across flat rate, interchange-plus, and subscription. | Include transaction fees, cross-border costs, AmEx surcharges, refunds, chargebacks, and any hidden fees. |

| Align merchant account setup and funding terms with cash flow. | Get next-day deposit timing, business-day cutoffs, reserve policies, and bank account verification in writing. |

| Test authorization and acceptance by payment methods and regions. | Measure approval rates for Visa, Mastercard, American Express, Apple Pay, and local rails; A/B against a second payment processor. |

| Stress-test customer support and SLAs. | Confirm 24/7 channels, escalation paths, incident comms, and a named account manager. Time a real ticket. |

| Plan dispute and chargeback management. | Enable alerts, set evidence templates, and track win-rate reporting; run a mock representment. |

| Confirm international coverage and local payment options. | Validate multi-currency, settlement currency, and dynamic currency conversion; check iDEAL, Bancontact, and regional wallets. |

| Map implementation and migration details. | Define API path, token vaulting, card updater, virtual terminal, and card reader needs; use a go-live checklist with rollback steps. |

Key Ecommerce Merchant Services

These are the services that matter day to day for an online store—no brochure fluff.

- Acceptance orchestration. Cover credit card payments, debit cards, wallets, and local methods across your ecommerce website, in-store POS systems, and mobile for both card-present and card-not-present checkout.

- Gateway and APIs. Expect fast, stable payment gateway uptime with clean docs, webhooks, retries, and SDKs that fit common ecommerce platforms and shopping carts.

- Risk controls. Layer fraud prevention—rules, machine learning, 3-D Secure, velocity checks, and chargeback alerts—so you cut fraud without crushing conversion.

- Auth optimization. Use smart routing, network tokens, account updater, and brand-level tuning for Visa, Mastercard, American Express, and Apple Pay to lift approval rates.

- Billing and invoicing. Run subscription management, dunning, pay-by-link, and a virtual terminal tied cleanly to your merchant account and bank account.

- Settlement and payouts. Get predictable funding by business day, multi-currency settlement, marketplace split payments, and transparent transaction fees from your payment processor.

- Reporting and reconciliation. See deposit summaries, interchange details, dispute statuses, and payout ledgers that map cleanly to your GL.

- Security and compliance. Shrink PCI compliance scope with tokenization and hosted fields, plus P2PE for POS systems and card readers when you sell in-person.

- Implementation and support. Demand sandbox access, token migration help, go-live checklists, and 24/7 customer support with real SLAs from your merchant services provider.

Benefits of Ecommerce Merchant Services

Real advantages you can measure, not vague “solutions.”

- Higher conversion. Faster checkout and modern payment options boost completed orders on your ecommerce site and mobile.

- Better approval rates. Smart routing and tokens reduce soft declines across card transactions and wallets.

- Lower total cost. Transparent pricing models expose hidden fees, optimize interchange, and cut cross-border surprises.

- Faster cash flow. Next-day funding, reliable cutoff windows by business day, and fewer reserves stabilize operations.

- Fewer chargebacks. Targeted 3-D Secure, alerts, and strong representment workflows keep disputes in check.

- Global reach. Local payment options and multi-currency support unlock new markets without rebuilding your ecommerce store.

- Simpler compliance. Tokenization and hosted fields keep sensitive data out of scope while maintaining secure payment acceptance.

- Omnichannel clarity. Unify online payments, in-store POS, and mobile for consistent refunds, reporting, and customer experience.

- Operational resilience. Redundant gateways, clear incident comms, and named escalation paths keep checkout up when it counts.

- Cleaner insights. Granular reporting by method, region, and channel informs pricing, promos, and inventory planning for business owners.

Costs & Pricing Structures of Ecommerce Merchant Services

You pay for payment processing in a few standard ways. Use this table to model total cost—then pressure-test quotes against your actual mix of card-not-present transactions, refunds, and chargebacks.

| Plan | Average Price | Common Features | Best for |

|---|---|---|---|

| Flat rate | ~2.6%–2.9% + $0.10–$0.30 per transaction | Simple statements, bundled PCI compliance, basic fraud tools, fast setup with popular ecommerce platforms | New or small business, straightforward online payments and checkout |

| Interchange-plus | Interchange + 0.10%–0.50% + $0.05–$0.10 | Pass-through pricing, clearer fees, stronger reporting, better at scale, works with most payment gateways | Growing ecommerce site aiming to lower effective rate |

| Subscription (membership) | $79–$199+/mo + interchange, ~$0.05–$0.10 per transaction | Low markup, predictable costs, good for high volume, virtual terminal options | High-volume online store optimizing margins |

| Tiered (qualified/mid/non-qual) | Varies widely by tier | Bundled “buckets,” easy quotes, may mask transaction fees and downgrade rules | Legacy setups or when a processor mandates tiering |

| Custom/enterprise | Quote only | Volume discounts, blended rates, multi-currency, dedicated support, fraud prevention add-ons, SLAs | Enterprises, marketplaces, high-risk or complex merchant account needs |

Caveats to keep in mind:

- Model effective rate. Include cross-border fees, refunds, network tokens, and chargeback costs—plus any “hidden fees.”

- Confirm funding terms. Get next-day deposit timing, business-day cutoffs, reserves, and bank account verification in writing.

- Check AmEx specifics. American Express often prices and settles differently from Visa/Mastercard.

- Verify add-ons. Tokenization, vaulted cards, and advanced fraud tools may carry extra line items.

- Test real flows. Run sandbox auth/capture/refund through your shopping cart and point of sale systems to spot gotchas early.

Key factors that influence pricing

- Transaction volume and ticket size. Higher volume and stable averages usually unlock better margins.

- Payment mix and regions. Wallets, card-present vs. card-not-present, and international cards shift approval rates and costs.

- Risk profile and disputes. High-risk categories and chargeback ratios increase underwriting scrutiny and fees.

- Integration and functionality. Custom APIs, orchestration, and marketplace payouts add complexity—and line items.

- Settlement and currencies. Multi-currency, DCC, and cross-border interchange impact totals and cash flow.

- Contract length and terms. Early-termination clauses, auto-renewals, and hardware leases can trap budget.

- Support and SLAs. Dedicated account management and 24/7 coverage often carry premium pricing—but reduce downtime costs.

Ecommerce Merchant Services FAQs

Here are some answers to common questions about ecommerce merchant services:

What’s the difference between a gateway, processor, and merchant account?

A payment gateway moves encrypted checkout data from your shopping cart to the networks. A payment processor (often your acquirer) runs the card transactions, talks to Visa/Mastercard/AmEx, and returns approvals or declines.

A merchant account is the underwriting and settlement relationship where funds land before hitting your bank account.

Many payment solutions bundle these—Stripe, PayPal, Square—while traditional merchant services separate them. Pick the model that fits your risk, pricing, and control needs.

How do I lift approval rates for card-not-present payments?

Feed better data and route smarter.Use network tokens, account updater, AVS/CVV, and the right transaction indicators for subscriptions and stored credentials.

Add smart retries based on decline codes, then route by BIN, card brand, and region to the best gateway or acquirer. Apply 3-D Secure selectively for high-risk flows, and tune fraud prevention rules so you don’t block good customers.

Wallets like Apple Pay also boost authorization in ecommerce.

What contract red flags should I watch for?

Lock in the economics before you sign. Watch for auto-renew terms, early-termination fees, non-cancellable hardware leases, monthly minimums, and “liquidated damages.”

Scrutinize add-ons—PCI compliance fees, chargeback handling, cross-border markups, statement and batch fees, and dynamic currency conversion you didn’t ask for.

Get interchange-plus or flat-rate math in writing, including refund costs and funding timing by business day. Tie SLAs and customer support to credits, not promises.

How do I support international customers without breaking finance?

Use a merchant services provider with local acquiring, multi-currency, and popular local methods (iDEAL, Bancontact, etc.). Present prices and process online payments in the shopper’s currency, but settle to your bank account in your preferred currency.

Ensure SCA/3-D Secure coverage for Europe, align tax settings, and confirm chargeback workflows per region. Test payout timing, fees, and reporting so reconciliation doesn’t devolve into spreadsheets.

What’s the safest way to switch providers without downtime?

Plan a dual-run. Secure token migration—network token portability or a PCI-compliant PAN-to-token transfer—so you don’t re-collect cards.

Stand up the new payment gateway and APIs in parallel, A/B traffic, and verify auth, capture, refunds, and webhooks.

Keep the old merchant account open for trailing refunds and chargebacks, match descriptors, and cut over after a clean reconciliation. Document rollback steps and owners—no heroics.

How do I keep PCI scope manageable and still offer a slick checkout?

Push card data out of your environment. Use hosted fields or a secure iFrame, tokenize everything, and avoid storing PANs.

For in-store, use P2PE-certified point of sale systems and card readers. Enforce TLS 1.2+, rotate keys, and segment systems that touch payment processing.

Aim for SAQ A or A-EP with your merchant services provider, and review fraud prevention and logging without ever handling raw card data.

Choose Payments That Fit, Not Fight You

Pricing puzzles, chargebacks, compliance scope, and clunky integrations slow checkout and squeeze cash flow.

The right ecommerce merchant services setup tightens security, lifts approval rates, and funds on time—without drama.

Use this guide to move fast: scan the shortlist, compare the side-by-side chart (pricing, trial info, best-for), then dive into the reviews to match a merchant services provider, payment gateway, and merchant account to your business needs.

If you're in the process of researching ecommerce merchant services, connect with a SoftwareSelect advisor for free recommendations.

You fill out a form and have a quick chat where they get into the specifics of your needs. Then you'll get a shortlist of software to review. They'll even support you through the entire buying process, including price negotiations.

Retail never stands still—and neither should you. Subscribe to our newsletter for the latest insights, strategies, and career resources from top retail leaders shaping the industry.