Le 10 migliori piattaforme Compra Ora, Paga Dopo nel 2026

Le 10 migliori piattaforme BNPL, la tua pratica lista

Prezzi elevati possono far esitare gli acquirenti—e mettere in difficoltà anche i commercianti. Gli articoli costosi rallentano le conversioni, aumentano l’abbandono del carrello e riducono il ROI degli annunci.

Ma se la soluzione non fosse fare sconti, ma offrire flessibilità?

Le piattaforme buy now, pay later (BNPL) permettono ai clienti di respirare, consentendo di suddividere gli acquisti in rate gestibili, spesso senza interessi—mentre tu ricevi comunque il pagamento immediatamente.

È vantaggioso per entrambe le parti.

Il BNPL non è più solo per la fast fashion o gli acquisti d’impulso. Dagli articoli essenziali quotidiani ai lussi, sta cambiando il modo di pagare in diversi settori.

Ma con così tanti fornitori, funzionalità e particolarità locali, scegliere il partner BNPL giusto non è affatto semplice.

Questa guida ti aiuterà a fare chiarezza. Abbiamo recensito le migliori piattaforme BNPL per ecommerce, abbonamenti e altro ancora—così potrai trovare la soluzione perfetta sia per il tuo business che per i tuoi clienti.

Perché Fidarti delle Nostre Recensioni sui Software

Testiamo e recensiamo software e servizi per il retail e l’e-commerce dal 2021. In quanto esperti del settore, sappiamo quanto sia critico e difficile prendere la decisione giusta nella selezione di un software. Investiamo in ricerche approfondite per aiutare il nostro pubblico a compiere scelte più consapevoli nella selezione dei software. Abbiamo testato oltre 2.000 strumenti per diversi casi d’uso in ambito finanziario e contabile e scritto più di 1.000 recensioni dettagliate sui software. Scopri come rimaniamo trasparenti e la nostra metodologia di recensione.

Confronto tra le migliori piattaforme BNPL per negozi online

Sebbene il confronto dei prezzi qui sotto potrebbe non fare piena luce su questi top servizi buy now, pay later, clicca su u003cstrongu003eConfronta softwareu003c/strongu003e dopo la tabella per vedere il confronto tra tutte le altre funzionalità.

| Tool | Best For | Trial Info | Price | ||

|---|---|---|---|---|---|

| 1 | Ideale per aiutare i clienti a costruire credito | Piano gratuito disponibile | Prezzo su richiesta | Website | |

| 2 | Ideale per vendere su Amazon | Piano gratuito disponibile | Prezzi su richiesta | Website | |

| 3 | Ideale per rivenditori che offrono servizi essenziali | Demo gratuita disponibile | Prezzi su richiesta | Website | |

| 4 | Ideale per brand di moda e lusso | Demo gratuita disponibile | Prezzi su richiesta | Website | |

| 5 | Ideale per utenti PayPal | Not available | Website | ||

| 6 | Ideale per pagamenti globali | Not available | Prezzi su richiesta | Website | |

| 7 | Ideale per servizi su abbonamento | Not available | Prezzo su richiesta | Website | |

| 8 | Ideale per favorire una spesa responsabile | Non disponibile | Prezzi su richiesta | Website | |

| 9 | Ideale per acquisti di grande importo | Not available | Prezzi su richiesta | Website | |

| 10 | Miglior soluzione BNPL white-label | Demo gratuita disponibile | Prezzo su richiesta | Website |

Le 10 migliori piattaforme BNPL, recensione completa

Siamo arrivati al succo del post: le recensioni. Dai un’occhiata ai nostri 10 migliori servizi BNPL, ognuno con i motivi della nostra scelta, le caratteristiche che si fanno notare e le integrazioni disponibili, vantaggi e svantaggi, oltre a uno screenshot della piattaforma.

Sezzle offre servizi trasparenti che possono aiutarti a mettere i tuoi clienti nelle condizioni di prendere decisioni d'acquisto più consapevoli e di costruire il proprio credito.

Perché ho scelto Sezzle: Offre ai clienti trasparenza ed educazione finanziaria per aiutarti a potenziare il tuo pubblico di riferimento. Ti consente di offrire ai tuoi clienti l'opportunità di evitare commissioni di mora e permette agli acquirenti più giovani di costruire credito mediante il programma Sezzle Up. Sezzle segnalerà i loro pagamenti rateali puntuali alle agenzie di credito quando i tuoi clienti si iscriveranno a questo programma.

Sezzle offre una soluzione BNPL semplice per i tuoi clienti. È disponibile solo un piano di pagamento: il piano in 4 rate, che include un acconto del 25% al momento dell'ordine da parte dei tuoi clienti e altri tre pagamenti. I tuoi clienti sono tenuti a completare tutti i pagamenti entro sei settimane.

Caratteristiche distintive e integrazioni di Sezzle

Caratteristiche includono l'elaborazione di carte di credito e di debito, la segnalazione alle agenzie di credito, la riprogrammazione dei pagamenti e conti di risparmio con interessi.

Integrazioni includono Shopify, CommentSold, WooCommerce, Magento, BigCommerce, Littledata, 3dcart, ResponseCRM, Cybersource, BuyItLive e Salesforce Commerce Cloud.

Sezzle offre prezzi personalizzati su richiesta.

Pros and Cons

Pros:

- Alta percentuale di approvazione dei clienti.

- Facile da configurare.

- Aiuta ad attirare clienti.

Cons:

- Le commissioni possono essere elevate.

- Problemi con l'assistenza clienti.

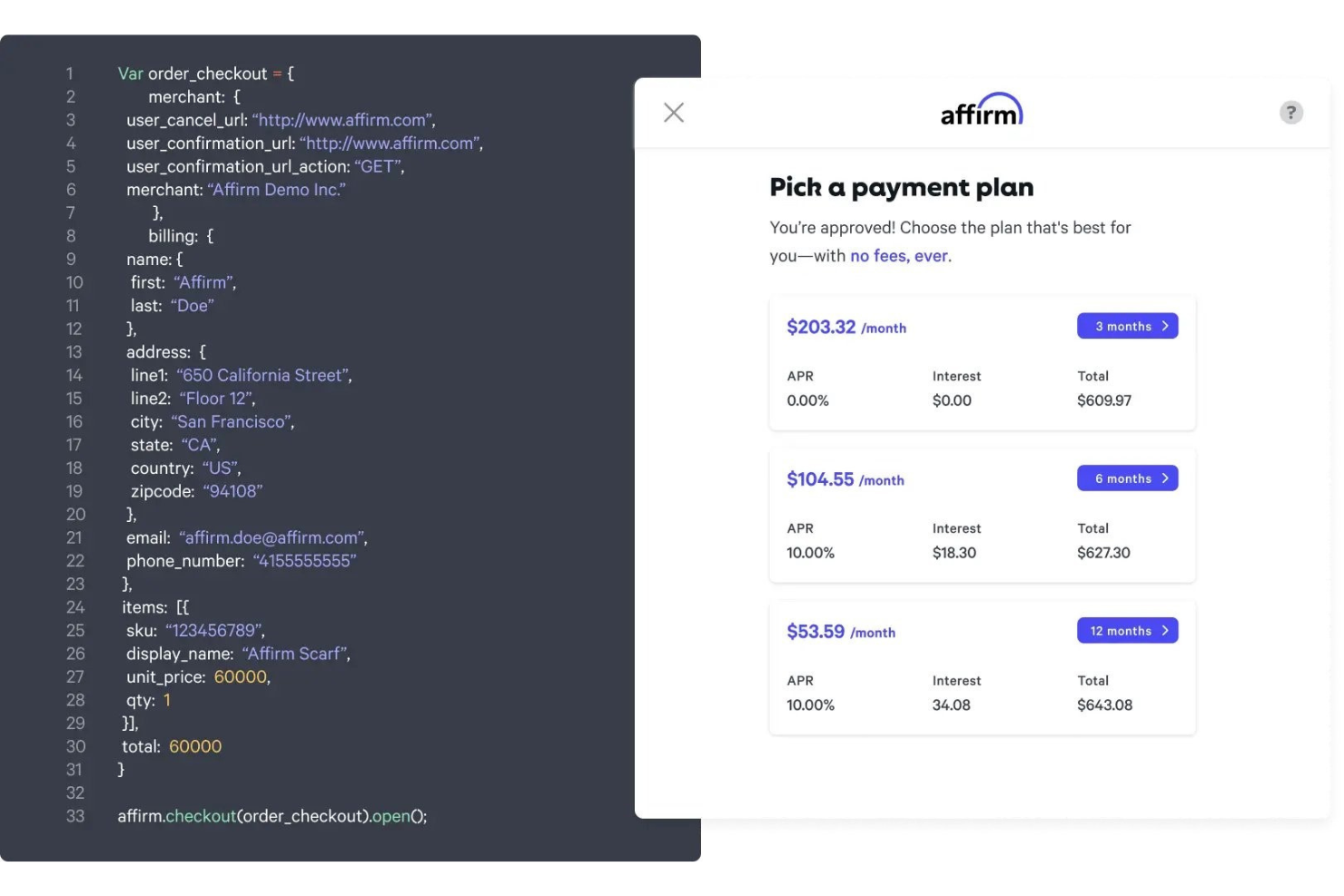

Affirm aiuta la tua azienda a offrire opzioni di pagamento flessibili ovunque i tuoi clienti acquistino i tuoi prodotti.

Perché ho scelto Affirm: La piattaforma è vantaggiosa per le transazioni ecommerce, in negozio e tramite teleselling. È la soluzione scelta da Amazon per il BNPL. Affirm permette alle aziende di integrare soluzioni di acquisto rateale per i clienti, ovunque essi effettuino l'acquisto. Puoi usare Affirm per mostrare ai tuoi clienti termini di pagamento flessibili su tutto il tuo sito ecommerce, inclusa ogni pagina prodotto e il checkout, così che sia facile per loro acquistare.

Affirm dà ai rivenditori il controllo totale sull'importo minimo che i clienti devono spendere per poter accedere al pagamento a rate. Puoi scegliere se offrire ai clienti un finanziamento con tasso d’interesse allo 0%, dove mostrare i messaggi di pagamento di Affirm e quanto tempo hanno i tuoi clienti per effettuare il pagamento. La piattaforma offre anche uno strumento chiamato Adaptive Checkout. Questa soluzione unica può aggiornare le opzioni di rimborso del prestito del tuo cliente quando aggiunge articoli al carrello, consentendo di visualizzare l'importo dell'acquisto in rate personalizzate durante la navigazione sul tuo sito.

Caratteristiche salienti e integrazioni di Affirm

Caratteristiche includono portale business, elaborazione di carte di credito, elaborazione pagamenti ACH, dashboard delle attività, pagamenti mobili, fatturazione ed emissione fatture, app mobile e analisi in tempo reale.

Integrazioni includono Wix, Shopify, WooCommerce, Magento, BigCommerce, OpenCart, 3dcart, NetSuite SuiteCommerce, AmeriCommerce, Volusion, Web Shop Manager, PlanetScale e Lightspeed eCommerce.

Affirm offre prezzi personalizzati su richiesta.

Pros and Cons

Pros:

- Dashboard intuitiva.

- Limiti di acquisto elevati per i clienti.

- Nessuna penale per ritardi di pagamento dei clienti.

Cons:

- Disponibile solo negli USA.

- La concorrenza potrebbe offrire tariffe migliori.

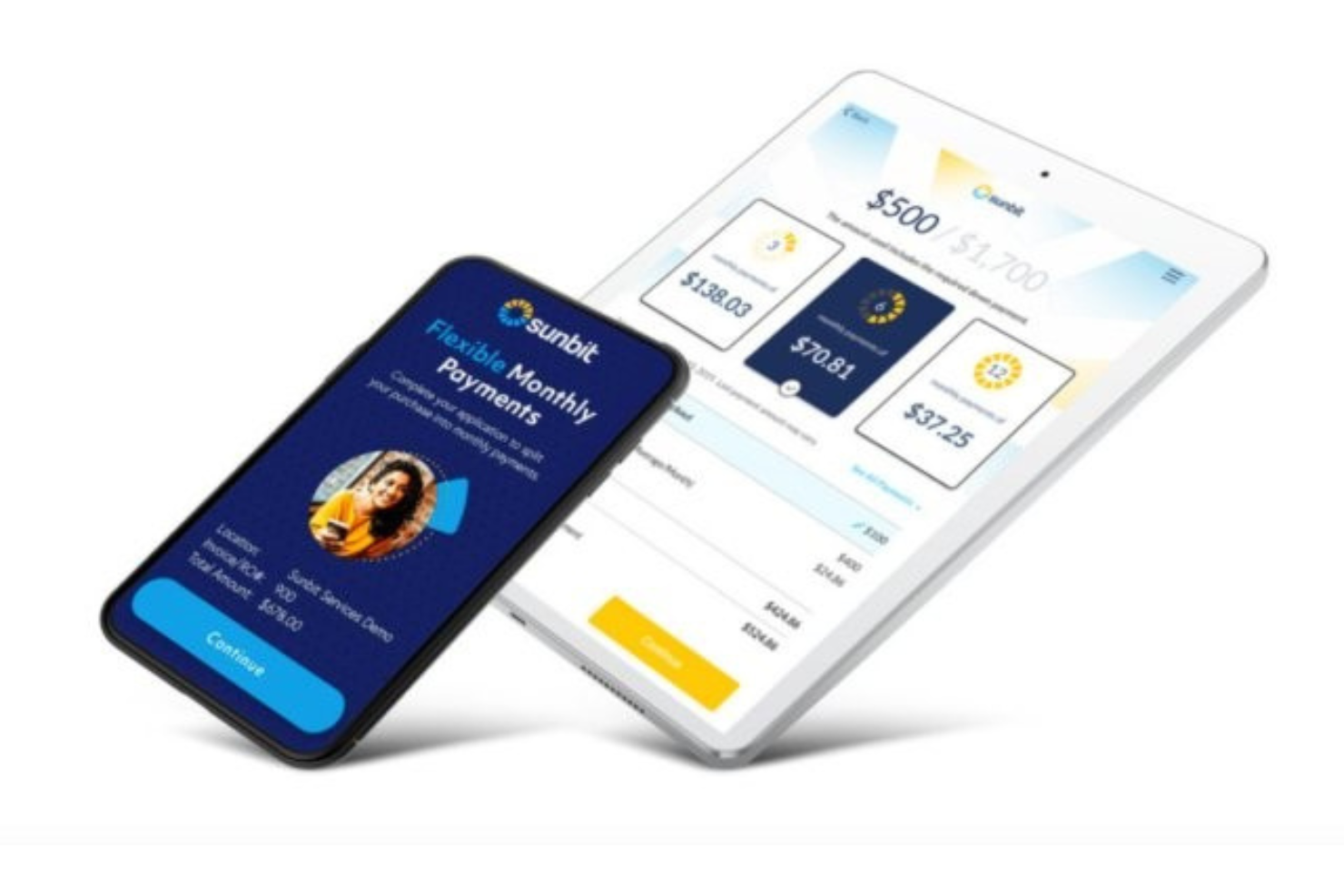

Sunbit ti aiuta a suddividere i pagamenti dei tuoi servizi essenziali per i clienti.

Perché ho scelto Sunbit: A differenza di altre piattaforme che si concentrano sui commercianti che vendono prodotti non essenziali, Sunbit si distingue permettendo alle aziende di offrire opzioni di pagamento rateale per servizi in presenza, come riparazioni auto, appuntamenti dall’oculista o visite veterinarie. Ti aiuta ad alleggerire il peso finanziario dei tuoi servizi essenziali per i tuoi clienti. Ma il vero punto di forza è che la tua attività avrà un vantaggio competitivo poiché potrai offrire servizi anche a clienti che potrebbero non avere un buon credito.

Sunbit aiuta le aziende che forniscono servizi essenziali ai loro clienti a renderli più accessibili. Con questa piattaforma puoi permettere ai clienti di pagare più servizi, fino a $10.000, con una durata delle rate da 3 a 12 mesi.

Funzionalità distintive di Sunbit

Funzionalità includono alti tassi di approvazione, una procedura di richiesta rapida, un team dedicato al successo dei partner, risorse di marketing digitale e approfondimenti utili.

Sunbit offre prezzi personalizzati su richiesta. Sunbit offre una demo gratuita.

Pros and Cons

Pros:

- Eccellente soluzione omnicanale.

- Pensato per le attività in presenza.

- Facile da usare.

Cons:

- Richiede un acconto.

- È necessario fare richiesta per scoprire i costi.

Klarna offre diverse opzioni BNPL che si adattano perfettamente ai brand di moda e lusso.

Perché ho scelto Klarna: La piattaforma è una scelta popolare tra le generazioni più giovani che generalmente acquistano da molti brand di moda e lusso. Questo grazie all'opzione di finanziamento 'Paga in 30 giorni' di Klarna, che permette ai tuoi clienti di provare gratuitamente i prodotti, tenere quelli che preferiscono e restituire quelli che non vogliono entro 30 giorni. Ti consente di offrire un'opzione senza pressione ai tuoi clienti e di incentivarli a completare gli ordini.

Klarna ti permette anche di offrire opzioni di checkout rapido sulle tue pagine prodotto, il che significa che puoi creare un'esperienza di acquisto in un solo clic. Tieni però presente che, utilizzando questa opzione, sarà applicata una commissione aggiuntiva per la tua azienda. Potrebbe comunque essere vantaggioso per ridurre lo sforzo richiesto ai clienti per concludere l'acquisto e diminuire la possibilità che cambino idea.

Funzionalità e integrazioni principali di Klarna

Funzionalità includono responsabilità zero per le frodi, pagamento anticipato, soluzioni globali, protezione venditore, aggiornamenti automatici, soluzioni pubblicitarie, ricerca prodotto, gestione degli ordini, strumenti di reportistica, analisi dei dati e un portale per i commercianti.

Integrazioni includono LogiCommerce, Desktop.com, Shopaccino, PremierCashier, Happy Returns, Cloud Funnels, 29 Next, Elixir, SendOwl, Centra, BetterCommerce e Adyen.

Klarna offre prezzi personalizzati su richiesta.

Pros and Cons

Pros:

- Nessuna limitazione sui prestiti.

- Opzioni di checkout multiple.

- Molto riconosciuta.

Cons:

- Assistenza clienti scadente.

- Alte commissioni per ritardi ai clienti.

La piattaforma BNPL “Pay-in-Four” di PayPal offre ai commercianti che già utilizzano PayPal Pay la possibilità di fornire ai clienti opzioni di pagamento alternative.

Perché ho scelto il “Pay-in-Four” di PayPal: La piattaforma PayPal è il sistema di pagamento più popolare e sicuro, e ha portato le proprie capacità anche nell’ambito BNPL. Possiede un livello di fiducia a livello globale che può aiutarti a trasformare potenziali clienti indecisi in acquirenti effettivi. I commercianti che già accettano PayPal come metodo di pagamento per i clienti possono implementare facilmente il sistema Pay-in-Four.

La piattaforma “Pay-in-Four” di PayPal può adattarsi a qualsiasi tipologia di azienda e aiutarti ad offrire ai tuoi clienti diverse opzioni di finanziamento. Tutto ciò che devi fare è aggiungere un pulsante “Paga Dopo” come ulteriore opzione di pagamento nel tuo sistema di checkout. Dopodiché, i clienti con un account PayPal esistente potranno richiedere il finanziamento Pay-in-Four se l’importo dell’acquisto è compreso tra $30 e $1.500.

Caratteristiche e integrazioni distintive di PayPal “Pay-in-Four”

Funzionalità includono analisi aziendali, reportistica, aggiornamenti automatici, elaborazione di carte di debito e credito, sistema POS, pagamenti ricorrenti, protezione acquisti, gestione delle fatture e checkout online.

Integrazioni includono BigCommerce, Wix, WooCommerce, GoDaddy, Adobe, Shift4Shop, XCart, Miva, Volusion, OpenCart, Cart.com e Vortx.

PayPal “Pay-in-Four” è un componente aggiuntivo gratuito per i commercianti che già utilizzano PayPal. Utilizzando la piattaforma, si pagherà solamente la normale commissione del 3,49% + $0,49 per transazione.

Pros and Cons

Pros:

- Organizzazione semplice.

- Facile da usare.

- Nessun costo aggiuntivo.

Cons:

- Alti tassi di interesse per i clienti.

- Porta i clienti fuori dal tuo sito web.

Zip Co è un'opzione conveniente per le aziende perché i clienti possono utilizzarlo ovunque nel mondo se usano una carta di credito Amex, Discover o Visa.

Perché ho scelto Zip Co: Precedentemente nota come Quadpay, Zip ti offre la possibilità di accettare pagamenti da clienti in qualsiasi parte del mondo, a patto che la tua azienda accetti pagamenti tramite Amex, Discover o Visa. La piattaforma ha anche una comunità di clienti a cui puoi collegare la tua attività per portare più traffico al tuo sito. Questa combinazione di una comunità globale e la possibilità di accettare i loro pagamenti significa che la tua azienda può beneficiare di un elevato valore medio degli ordini.

Zip Co consente alla tua azienda di mettere al primo posto i clienti offrendo rate comode che non influenzano il loro punteggio di credito. Zip Co permette ai tuoi clienti di controllare il proprio piano di rimborso e impostare pagamenti settimanali, bisettimanali o mensili. Quando i clienti scelgono di pagare a rate un acquisto, la tua azienda riceverà il pagamento lo stesso giorno dal fornitore.

Funzionalità e integrazioni principali di Zip Co

Funzionalità includono gestione degli ordini, gestione dei dati dei clienti, portale per esercenti, gestione riconciliazioni, marketplace della community, widget per siti web, elaborazione dei rimborsi ed elaborazione delle carte di credito.

Integrazioni includono Salesforce, Shopify, WooCommerce, Magento, BigCommerce, Oracle Commerce, Workarea e CartHook. Zip Co offre anche un'API per collegare la piattaforma ai tuoi sistemi attuali.

Zip Co offre prezzi personalizzati su richiesta.

Pros and Cons

Pros:

- Piattaforma reattiva.

- Aumenta il valore medio degli ordini.

- Facile da navigare.

Cons:

- Nessuna demo della piattaforma.

- Nessun report.

Wisetack consente alle aziende di offrire ai clienti opzioni di pagamento trasparenti per prodotti e servizi in abbonamento.

Perché ho scelto Wisetack: La piattaforma si integra con il tuo sito web e con il processo di checkout attuale, permettendo alla tua azienda di offrire ai clienti opzioni di pagamento rateali per servizi come box in abbonamento o servizi di streaming. Wisetack BNPL (Buy Now, Pay Later) è una soluzione di finanziamento che consente alle aziende ecommerce di offrire ai propri clienti la possibilità di pagare i loro acquisti a rate invece che in un'unica soluzione. Integrando Wisetack BNPL nella propria piattaforma ecommerce, le aziende possono offrire ai clienti la flessibilità di pagare nel tempo e potenzialmente aumentare la fedeltà e le vendite.

Wisetack BNPL offre inoltre diversi vantaggi alle aziende stesse, come la riduzione dell'abbandono del carrello e il miglioramento del flusso di cassa, poiché i clienti sono più propensi a completare l'acquisto quando viene data loro la possibilità di pagare a rate. Inoltre, Wisetack BNPL fornisce alle aziende preziose informazioni sulle abitudini di spesa dei clienti, aiutandole a prendere decisioni consapevoli su inventario, marketing e altre operazioni aziendali. In generale, Wisetack BNPL può essere uno strumento prezioso per le aziende ecommerce che cercano di aumentare le vendite, fidelizzare i clienti e migliorare la loro salute finanziaria complessiva.

Funzionalità e integrazioni principali di Wisetack

Funzionalità includono finanziamenti al consumo, approvazioni rapide per i clienti, elaborazione di pagamenti con carte di debito e credito e pagamenti immediati.

Integrazioni includono un'API che si integra con i sistemi già in uso.

Wisetack offre prezzi personalizzati su richiesta. Wisetack non offre informazioni su una prova gratuita.

Pros and Cons

Pros:

- Controllo delle condizioni di pagamento.

- Integrazioni semplici.

- Ottimo coordinamento con il fornitore.

Cons:

- È necessario attendere per ricevere i fondi.

- Le commissioni possono essere elevate.

Afterpay offre un limite di credito ai tuoi clienti per effettuare acquisti sul tuo negozio ecommerce e fornisce premi per una spesa responsabile.

Perché ho scelto Afterpay: La piattaforma stabilisce limiti di credito iniziali ragionevoli e trasparenti per chi è nuovo all'utilizzo di Afterpay nell'acquisto di prodotti. Questo limite iniziale può aumentare quando i clienti effettuano i loro pagamenti puntualmente. Il fornitore offre anche consigli per aiutare i clienti a spendere in modo responsabile.

Afterpay è adatto ai rivenditori con negozi online e opzioni di acquisto in negozio. Ha un'integrazione semplice e incorporata con Square, che rende facile offrire opzioni BNPL da un sistema POS Square. È inoltre possibile ordinare un kit di marketing da Afterpay per aiutare i tuoi clienti a sapere che accetti Afterpay come opzione di pagamento.

Caratteristiche e integrazioni principali di Afterpay

Caratteristiche includono elaborazione pagamenti ACH, rilevamento delle frodi, pagamenti elettronici, sicurezza dei dati, pagamenti mobili, elaborazione carte di credito, fatturazione ricorrente e cronologia delle transazioni.

Integrazioni includono Ecwid, CS-Cart, Shopify, Wix, WooCommerce, Synder, Magento, BigCommerce, Cloud Funnels, Propeller, BridgerPay e Salesforce Commerce Cloud.

Afterpay offre prezzi personalizzati su richiesta.

Pros and Cons

Pros:

- Eccellente supporto per i commercianti.

- Nessun controllo del credito sui clienti.

- Facile da usare.

Cons:

- Alti interessi sui pagamenti in ritardo.

- Alcuni rivenditori possono essere rifiutati.

Humm è una piattaforma BNPL che aiuta i clienti a suddividere acquisti di importo molto elevato.

Perché ho scelto Humm: Come affermato sul sito di Humm, questo servizio BNPL aiuta i tuoi clienti ad acquistare “grandi cose”. Permette di suddividere qualsiasi acquisto fino a $30.000! I tuoi clienti possono distribuire questi pagamenti in cinque o dieci rate ogni due settimane oppure fino a 60 mesi per acquisti più importanti.

Humm garantisce il saldo del pagamento anticipato alla tua azienda il giorno lavorativo successivo. Questo può essere fondamentale se sei una piccola impresa che dipende da questi pagamenti. Inoltre, se un cliente restituisce un articolo al tuo negozio, Humm restituirà la loro commissione sugli articoli.

Caratteristiche distintive e integrazioni di Humm

Caratteristiche includono rimborsi flessibili, verifiche di credito soft e gestione degli acquisti online e in negozio.

Integrazioni includono Salesforce, Shopify, WooCommerce, Magento, Striven POS, PrestaShop, OpenCart, Kitomba, Retail Directions, Shopify Plus, Intershop ed eStar.

Humm offre prezzi personalizzati su richiesta.

Pros and Cons

Pros:

- Procedura di iscrizione semplice.

- API REST diretta.

- I clienti possono fare acquisti di grande valore.

Cons:

- Commissioni elevate per i clienti.

- Il supporto clienti necessita miglioramenti.

Splitit aiuta le aziende di ecommerce a offrire pagamenti a rate ai clienti direttamente dai loro siti web.

Perché ho scelto Splitit: Puoi utilizzare la piattaforma per gestire l'intero percorso d'acquisto grazie alle sue funzionalità white-label. La tua marca rimane al centro, permettendoti di aumentare la fedeltà del cliente. L'intero processo di acquisto ora-paga-dopo è integrato nel tuo sito.

Splitit non acquisisce i tuoi clienti per vendergli altri prodotti: i tuoi clienti restano tuoi, non loro. Puoi personalizzare l'esperienza dei clienti, incluso il controllo su quanto spesso desideri che effettuino i pagamenti e se richiedere un acconto. Splitit autorizza l'intero importo dell'acquisto sulla carta di credito del cliente e ne riserva il saldo fino al pagamento finale.

Funzionalità e integrazioni principali di Splitit

Funzionalità includono conformità PCI, reportistica e analisi, pagamenti in presenza, elaborazione di carte di debito e credito e punto vendita.

Integrazioni includono Shopify, PayPal, WooCommerce, BlueSnap, Magento, BigCommerce, PrestaShop, Authorize.net, WorldPay, Adyen e Wix.

Splitit costa a partire dall'1,5% di ogni transazione e $1,50 aggiuntivi per ogni rata. Ti inviano fattura ogni mese.

Pros and Cons

Pros:

- Dashboard facile da usare.

- Configurazione intuitiva.

- Basse commissioni per i commercianti.

Cons:

- Problemi con banche estere.

- I clienti devono avere credito disponibile prima dell'acquisto.

{kind=link}

Altre recensioni di software ecommerce

Se non hai ancora trovato ciò che cerchi qui, scopri questi strumenti ecommerce correlati che abbiamo testato e valutato.

- Piattaforme Ecommerce

- Software per la gestione dell'inventario

- Software per l'elaborazione dei pagamenti

- Soluzioni per il carrello elettronico

- Sistemi per la gestione degli ordini

- Software per la gestione del magazzino

Come valuto le piattaforme BNPL

Valuto le piattaforme BNPL su due livelli: i requisiti di base come il pagamento anticipato al commerciante e la valutazione del credito in tempo reale, e gli elementi distintivi che rendono una piattaforma più adatta alla tua attività al dettaglio.

Funzionalità di base (requisiti necessari per questa lista)

Quando seleziono gli strumenti per la mia lista, valuto ciascuno su una scala da 0 (non offre la funzionalità) a 5 (eccelle in quest'area) per ciascuna funzionalità di base elencata di seguito. Poi calcolo il punteggio totale dello strumento in percentuale. Ogni strumento deve raggiungere un punteggio totale minimo del 65% per essere considerato per l'inclusione.

- Piani di pagamento rateale: Verifico quali tipi di piani sono disponibili—Pagamento in 4 rate, piani mensili, finanziamenti a più lungo termine—e se i commercianti possono configurare la durata dei piani per diverse categorie di prodotto.

- Valutazione del credito del consumatore: L'approvazione in tempo reale al checkout è fondamentale, quindi valuto come ogni piattaforma gestisce la velocità decisionale, i tassi di approvazione e il supporto per acquirenti con scarso storico creditizio.

- Pagamenti e liquidazioni ai commercianti: Esamino quanto rapidamente i rivenditori vengono pagati e se il fornitore si assume completamente il rischio di insolvenza del consumatore, poiché pagamenti ritardati o parziali vanificano lo scopo.

- Integrazione Ecommerce & POS: La copertura della piattaforma è fondamentale—controllo la presenza di plugin nativi per Shopify, WooCommerce, Magento e BigCommerce, oltre alla compatibilità con POS in-store per venditori omnicanale.

- Strumenti per il checkout: L'adozione del BNPL dipende molto dalla visibilità, quindi valuto la messaggistica sul sito, i widget nelle pagine prodotto e quanto controllo hanno i commercianti su branding e posizionamento.

- Dashboard di reportistica per commercianti: Cerco dashboard che vadano oltre i registri transazionali, includendo il tracciamento delle liquidazioni, la gestione delle controversie e metriche di performance come aumento del valore medio d'ordine (AOV) e dati sulle conversioni.

Una volta che ho una lista di strumenti che soddisfano questi criteri, considero cosa distingue ogni piattaforma.

Fattori differenzianti (Cosa distingue i fornitori)

Ecco come confronto e metto a confronto i diversi fornitori:

Caratteristiche distintive

Strumenti di marketing co-branded fanno davvero la differenza. Cerco fornitori le cui app per i consumatori e le directory di marketplace portino nuovi acquirenti al tuo negozio. Questo trasforma il BNPL in un canale di acquisizione clienti, non solo in un metodo di pagamento. Per i retailer omnicanale, funzionalità in-store come l'emissione di carte virtuali e il checkout tramite QR-code estendono il BNPL ai punti vendita fisici. Conta anche il supporto internazionale—piani di pagamento localizzati e liquidazioni in più valute ti permettono di vendere in diverse regioni senza dover gestire fornitori di finanziamento separati.

Oltre alle funzionalità

La trasparenza delle commissioni è fondamentale. Valuto se la tariffazione MDR varia in base all’importo dello scontrino e alla durata del piano, e se i commercianti possono finanziare offerte promozionali a TAEG 0% senza costi nascosti per chargeback. Anche la conformità normativa ha un peso importante—le norme BNPL stanno diventando più stringenti a livello globale, quindi verifico le informative di credito e le certificazioni sulla gestione dei dati di ciascun fornitore, come PCI-DSS e SOC 2. La compatibilità tecnologica completa il quadro. Un fornitore BNPL che si collega alla tua piattaforma ecommerce ma non al tuo POS, OMS o CRM genera lacune nelle operazioni omnicanale.

Come scegliere la migliore piattaforma BNPL

Il BNPL non è una soluzione uguale per tutti. La piattaforma migliore per il tuo negozio dipende dal tuo modello di business, dal tech stack, dalla clientela—e da quanto dai importanza a fattori come copertura globale o prestiti responsabili. Ecco come restringere il campo.

| Fase | Cosa fare | Perché è importante |

|---|---|---|

| 1. Definisci il vero problema | Vuoi risolvere l’abbandono del carrello, aumentare il valore medio dell’ordine o solo offrire maggiore flessibilità agli acquirenti? Chiarisci il “perché”. | Ti aiuta a restare concentrato ed evita la sindrome della funzionalità luccicante. |

| 2. Scopri chi lo usa | Serve solo al tuo team ecommerce, oppure ne hanno bisogno anche assistenza, finanza e personale in negozio? | Influenza le esigenze della UI, l’onboarding e il numero di utenti da gestire. |

| 3. Controlla la tua infrastruttura | Verifica che la piattaforma si integri con POS, CRM, ERP e la tua piattaforma ecommerce. | Nessuno vuole rivoluzionare tutto o improvvisare una soluzione che non comunica. |

| 4. Pensa locale + globale | Hai bisogno di copertura globale? Cerca piattaforme con disponibilità regionale, supporto multi-valuta e conformità localizzata. | Non tutti i BNPL sono ovunque. Zip, ad esempio, copre più paesi rispetto ad Affirm. |

| 5. Guarda sotto il cofano | Chiedi informazioni su controlli di credito soft vs. hard, approvazioni automatiche e opzioni di personalizzazione. | Impatta l’esperienza utente e il tasso di conversione. Aiuta anche a evitare problemi normativi. |

| 6. Allinea ai valori del tuo brand | Vuoi un fornitore attento? Cerca iniziative a impatto sociale, limiti etici sui prestiti e strutture di commissioni trasparenti. | I clienti ci tengono. Anche il tuo checkout dovrebbe. |

| 7. Fai i conti | Valuta le commissioni per transazione, eventuali costi mensili fissi e cosa ottieni (ad esempio co-marketing). | I fornitori a basso costo potrebbero lesinare su assistenza o copertura. Fai bene i calcoli. |

| 8. Definisci subito il successo | Stabilisci come misurerai il successo: più conversioni, carrelli più grandi, checkout più veloce? | Imposta i benchmark subito per evitare rimorsi in seguito. |

Tendenze delle piattaforme BNPL per 2026

Il BNPL sta crescendo in fretta. Ma le tendenze più rumorose non sono sempre le più importanti. Ecco cosa dovrebbero davvero monitorare gli operatori ecommerce nel 2026:

- I round di finanziamento stanno portando a un’esplosione di funzionalità. I grandi player del BNPL sono pieni di risorse dai venture capitalist—e si vede. Molti puntano su partnership vistose e dashboard accattivanti anziché sulle reali performance del checkout. I merchant devono andare oltre il rumore e testare ciò che fa davvero crescere le conversioni.

- Le piattaforme diventano di nicchia, non generaliste. Invece di voler essere tutto per tutti, i nuovi BNPL si focalizzano su settori specifici—come Sunbit nei servizi essenziali o Wisetack negli abbonamenti. Scegliere un player generalista può significare perdere funzionalità pensate per il tuo settore.

- L’etica nel prestito è un vantaggio competitivo. I giovani non vogliono solo flessibilità di pagamento, ma anche sentirsi a proprio agio nell’usarla. Fornitori come Afterpay introducono limiti e formazione per responsabilizzare senza penalizzare il cliente.

- La localizzazione sostituisce l’espansione globale. I player più smart non si limitano a lanciare in nuovi paesi: si adattano. UX differenziata per regione, supporto locale e piani di pagamento modellati sulle abitudini culturali, non solo sui cambi valuta.

- I marketplace BNPL sono il nuovo canale affiliato. Klarna, Zip e altri stanno promuovendo marketplace selezionati per indirizzare traffico verso i merchant delle loro piattaforme. Per i brand ciò significa visibilità gratuita, ma anche maggiore dipendenza da ecosistemi di terzi.

- La pressione normativa sta cambiando il prodotto. In mercati come UK ed Europa, le regole costringono i BNPL a semplificare i termini, limitare le commissioni e rendere i rischi più evidenti. Per i brand ecommerce, meno sorprese—ma meno margine di personalizzazione delle condizioni.

- I migliori fornitori stanno puntando sul B2B. Il BNPL per acquisti business—come acquisti all’ingrosso, abbonamenti SaaS o forniture per PMI—è in crescita. Se i tuoi clienti non sono consumatori finali, questa nuova ondata può essere un’opportunità.

- La solvibilità diventa dinamica e in tempo reale. I tradizionali punteggi FICO cedono il passo a valutazioni AI immediate basate sul comportamento, non solo sulla storia creditizia. Più approvazioni—e meno insoluti—scegliendo un provider intelligente.

Caratteristiche principali delle piattaforme BNPL

Una buona piattaforma BNPL non si limita a frazionare i pagamenti: deve aumentare le conversioni, ridurre gli attriti e rispecchiare i valori del tuo brand. Ecco cosa valutare:

- Approvazione del credito immediata. I clienti possono ottenere l'approvazione sul momento grazie a controlli del credito soft, rendendo il processo di acquisto rapido e senza attriti.

- Piani di pagamento flessibili. La maggior parte dei servizi BNPL offre diverse opzioni, come 4 pagamenti senza interessi o finanziamenti estesi fino a 60 mesi.

- Integrazione fluida con la piattaforma. I principali fornitori offrono supporto plug-and-play per Shopify, Magento, sistemi POS e persino stack personalizzati tramite API.

- Prontezza globale. Le piattaforme leader includono il supporto multivaluta, metodi di pagamento locali e l'adeguamento alla normativa di ciascuna regione.

- Prestiti etici e responsabili. Cerca limiti di spesa, trasparenza sulle commissioni di mora e strumenti educativi integrati che favoriscono una finanza al consumo più intelligente.

- Esperienze ottimizzate per mobile. Un design mobile-first e app dedicate facilitano ai clienti la richiesta, la gestione dei pagamenti e nuovi acquisti.

- Commissioni trasparenti per i commercianti. Dovresti sapere esattamente quanto paghi per transazione e cosa ottieni in cambio.

- Pagamenti e promemoria automatici. Le piattaforme automatizzano le detrazioni e inviano notifiche intelligenti per ridurre i mancati pagamenti (e i crediti deteriorati).

- Approfondimenti e analisi sui clienti. Ottieni dati sui comportamenti di acquisto, sui modelli di rimborso e sull'impatto dell'AOV—da utilizzare per ottimizzare il funnel.

- Strumenti di marketing co-branded. Alcune piattaforme (come Klarna o Afterpay) offrono kit di strumenti per commercianti, campagne di co-marketing e posizionamento nei marketplace.

Principali Vantaggi delle Piattaforme BNPL

Le piattaforme BNPL sono strumenti di performance. Migliorano le conversioni, sbloccano nuovi segmenti di clientela e rendono il checkout più smart e flessibile. Ecco cos'altro offrono:

- Aumento del valore medio del carrello e dei tassi di conversione. Suddividere i pagamenti riduce lo shock del prezzo e accresce la fiducia nell'acquisto, soprattutto su articoli costosi.

- Pagamenti immediati per i commercianti. Vieni pagato subito. Il rischio di incasso viene gestito dal provider BNPL, non da te.

- Accesso a consumatori non bancarizzati e più giovani. Queste piattaforme servono acquirenti senza carte di credito tradizionali o punteggi creditizi elevati—aiutandoti a raggiungere nuovi pubblici.

- Espansione transfrontaliera semplificata. Le piattaforme BNPL con copertura globale gestiscono compliance, valute e specificità locali—così non dovrai occupartene tu.

- Migliore percezione post-acquisto. I clienti apprezzano opzioni senza interessi e senza attriti—favorendo esperienze più positive e maggiore fidelizzazione.

- Strumenti integrati per la salute finanziaria. Alcuni fornitori includono promemoria di pagamento, limiti e funzionalità di budgeting che aiutano i consumatori a mantenere il controllo.

- Approvazioni più intelligenti con dati in tempo reale. Le valutazioni del rischio basate su AI ampliano le approvazioni senza aumentare i default, anche per i nuovi clienti.

- Maggiore visibilità di marketing. Klarna, Zip e altri offrono marketplace integrati, co-branding e campagne che riportano traffico sul tuo sito.

Costi e Tariffe delle Piattaforme BNPL

Le piattaforme BNPL presentano strutture tariffarie diverse a seconda del provider e delle esigenze del tuo business.

La maggior parte delle piattaforme addebita una commissione percentuale sulle transazioni; alcune prevedono anche commissioni aggiuntive per commercianti di piccole dimensioni o con volumi bassi.

Ecco una panoramica delle attuali tendenze dei prezzi BNPL e il confronto tra alcune piattaforme popolari:

| Piattaforma | Commissione di transazione | Tasso di interesse (consumatore) | Ideale per |

|---|---|---|---|

| Sezzle | 6% + $0.30 per transazione | 0% per "Pay in 4" | Ideale per aiutare i clienti a costruire il credito, soprattutto i consumatori più giovani che desiderano creare una storia creditizia. |

| Klarna | 3,29% a 5,99% + $0.30 per transazione | 0% per "Pay in 4" e "Pay in 30"; 19,99% per piani più lunghi | Ideale per marchi di moda e di lusso grazie alla sua forte base clienti e integrazione nel marketplace. |

| PayPal Pay Later | 1,9%-3,49% + $0.49 per transazione | 0% per "Pay in 4"; 9,99%-35,99% per pagamenti mensili | Consigliato per le aziende che utilizzano già PayPal come gateway di pagamento. |

| Uplift | 2-4% per transazione | 0% di interesse; termini personalizzati fino a 24 mesi | Consigliato per attività nel settore dei viaggi, permettendo grandi prenotazioni con opzioni di rimborso flessibili. |

| Zip (precedentemente Quadpay) | 4-5% per transazione | 0% per "Pay in 4" | Ideale per pagamenti globali, soprattutto per commercianti che desiderano servire clienti internazionali. |

| Humm | 3-6% per transazione | 0% per rate; piani personalizzati fino a 60 mesi | Ottimo per acquisti di importi elevati (fino a $30.000) in settori come arredamento o beni di lusso. |

| Afterpay | 4-6% + $0.30 per transazione | 0% per "Pay in 4" | Ideale per i rivenditori che si rivolgono a consumatori giovani e attenti al budget, con limiti di spesa responsabili. |

Considerazioni chiave:

- Commissioni di transazione: La maggior parte delle piattaforme, come Sezzle, Afterpay e Zip, applica il 4-6% per transazione. Le commissioni di Uplift tendono ad essere inferiori, 2-4%, soprattutto per acquisti legati ai viaggi.

- Tassi di interesse per i consumatori: Opzioni senza interessi sono comuni per i piani a breve termine, ma quelli a lungo termine possono arrivare fino a il 36%, a seconda della piattaforma e del profilo di credito del cliente.

- Ideale per: Ogni piattaforma si rivolge a tipologie di aziende specifiche. Ad esempio, Sezzle è ottima per consumatori giovani in cerca di credito, mentre Uplift è perfetta per beni di alto valore in settori come viaggi e beni di lusso.

Quando scegli un fornitore BNPL, bilancia commissioni di transazione e costi aggiuntivi rispetto alle funzionalità della piattaforma e a quanto si adatta al tuo pubblico target.

FAQ sulle piattaforme BNPL

A questo punto hai letto molto (oppure hai solo dato una scorsa veloce). In entrambi i casi, abbiamo ipotizzato alcune domande che potresti avere ancora e ci siamo impegnati a rispondere per la tua comprensione.

Quali sono i fornitori BNPL più popolari?

I nomi più importanti nel settore BNPL includono Afterpay, Klarna, Affirm, PayPal Pay Later e Zip. Queste piattaforme si distinguono per piani di pagamento flessibili, integrazioni solide e fiducia dei clienti.rnrnOperatori regionali come Clearpay (Regno Unito) e Sezzle (USA) stanno crescendo rapidamente. Klarna è leader nella moda e nel lusso, mentre Affirm è nota per gli acquisti di alto valore come elettronica o arredamento. Nuovi operatori come Splitit si concentrano sull’offerta di piani rateali direttamente tramite carte di credito senza nuove linee di credito.

Cosa succede se un cliente salta un pagamento su un piano BNPL?

La maggior parte delle piattaforme BNPL applica commissioni di mora se un cliente salta un pagamento, ma le politiche variano:rnu003culu003ern tu003cliu003eu003cstrongu003eAfterpayu003c/strongu003e applica una penale di $10 per ogni pagamento mancato, fino a un massimo del 25% del valore dell’ordine.u003c/liu003ern tu003cliu003eu003cstrongu003eKlarnau003c/strongu003e addebita penali dopo un periodo di tolleranza, ma l’importo dipende dalla regione.u003c/liu003ern tu003cliu003eu003cstrongu003eAffirmu003c/strongu003e non applica penali, ma segnala i pagamenti mancati alle agenzie di credito, il che potrebbe influenzare il punteggio di credito del cliente.u003c/liu003ernu003c/ulu003ernI commercianti possono ridurre i mancati pagamenti comunicando chiaramente i termini di rimborso fin dall’inizio e inviando promemoria via email o SMS. In questo modo si garantisce un’esperienza cliente più fluida e si mantiene la fidelizzazione.

In che modo il BNPL può migliorare i miei tassi di conversione?

Il BNPL può aumentare significativamente i tassi di conversione e il valore medio dell’ordine. Offrendo ai clienti la possibilità di pagare a rate, si riduce lo shock del prezzo per acquisti di importo elevato. I clienti sono più propensi all’acquisto quando non devono pagare l’intero importo anticipatamente, portando così a meno carrelli abbandonati e maggiori entrate. Molti commercianti riscontrano un aumento nelle conversioni, a volte fino al 20-30%, dopo aver integrato le opzioni BNPL.

Posso negoziare commissioni di transazione più basse con i fornitori BNPL?

Sì, è possibile negoziare commissioni di transazione più basse—soprattutto se la tua azienda gestisce volumi di transazione elevati. Per rafforzare la tua posizione:rnu003culu003ern tu003cliu003eDimostra il volume e la costanza delle tue vendite.u003c/liu003ern tu003cliu003eEvidenzia come le tue offerte siano in linea con i settori target del fornitore BNPL.u003c/liu003ern tu003cliu003eValuta la possibilità di includere commissioni marketing o co-promozioni per ottenere condizioni migliori.u003c/liu003ernu003c/ulu003ernSe generi un fatturato significativo tramite BNPL, non esitare a negoziare per migliorare i tuoi margini.

Quali sono i costi nascosti dell’offerta BNPL?

Se da un lato il BNPL può aumentare le vendite, è importante essere consapevoli dei costi nascosti:rnu003culu003ern tu003cliu003eu003cstrongu003eCommissioni di transazione:u003c/strongu003e Generalmente tra il 4-6%, possono ridurre i margini.u003c/liu003ern tu003cliu003eu003cstrongu003eCommissioni di marketing:u003c/strongu003e Piattaforme come Klarna applicano costi aggiuntivi per mostrare il tuo brand nel loro marketplace.u003c/liu003ern tu003cliu003eu003cstrongu003eInsoddisfazione del cliente:u003c/strongu003e Le penali di mora possono generare esperienze negative, riducendo la fedeltà.u003c/liu003ernu003c/ulu003ernPer compensare questi costi, monitora attentamente il ROI delle vendite con BNPL, negozia le commissioni di transazione e comunica con chiarezza ai clienti le condizioni di rimborso.

Come gestiscono i rimborsi le piattaforme BNPL?

Le politiche di rimborso variano a seconda della piattaforma, ma di solito i commercianti effettuano i rimborsi direttamente al fornitore BNPL. Il fornitore poi adegua il piano di pagamento del cliente o rimborsa gli importi già versati. È importante che i commercianti comprendano le politiche di rimborso del proprio partner BNPL per evitare ritardi o confusione nei clienti.

Quali tipi di aziende traggono più vantaggio dal BNPL?

Il BNPL è particolarmente efficace per settori con acquisti ad alto valore o discrezionali, come elettronica, moda, arredamento, viaggi e sanità. Può inoltre essere adatto per aziende che si rivolgono a un pubblico giovane o a persone restie all’utilizzo del credito tradizionale.

Recensioni aggiuntive sui software di pagamento ecommerce

Se stai cercando una soluzione BNPL, potresti essere interessato anche a queste recensioni di software correlati. Tutte queste soluzioni si concentrano su finanza, pagamenti o gestione fiscale per l’ecommerce.

- Software per punti vendita (POS)

- Soluzioni di pagamento mobile

- Software per la gestione della tassa sulle vendite ecommerce

- Software per la prevenzione delle frodi ecommerce

Cosa succederà ora?

Se stai cercando piattaforme "compra ora, paga dopo", contatta gratuitamente un consulente SoftwareSelect per ricevere suggerimenti personalizzati.

Compila un modulo e fai una breve chiacchierata durante la quale si approfondiscono le tue esigenze specifiche. Poi riceverai un elenco ristretto di software da esaminare. Ti supporteranno anche durante tutto il processo d'acquisto, comprese le negoziazioni sui prezzi.