1 Migliori Società di Elaborazione Carte di Credito per 2026

Le migliori società di elaborazione carte di credito da considerare

Le migliori società di elaborazione carte di credito ti aiutano ad accettare pagamenti senza intoppi, mantengono le commissioni trasparenti e ti fanno ricevere i soldi velocemente—il tutto integrandosi facilmente con i sistemi che già usi.

Scegli il fornitore giusto e ti eviterai spiacevoli sorprese sui costi, problemi di sicurezza e grattacapi tecnici.

Abbiamo passato anni a valutare fornitori, inseguire l’assistenza clienti e confrontare i costi, così non dovrai farlo tu. In questa guida ti indicherò le migliori società di elaborazione carte di credito per piccole imprese, per aiutarti a scegliere rapidamente e senza stress.

Perché Fidarti delle Nostre Recensioni sui Software

Testiamo e recensiamo software e servizi per il retail e l’e-commerce dal 2021. In quanto esperti del settore, sappiamo quanto sia critico e difficile prendere la decisione giusta nella selezione di un software. Investiamo in ricerche approfondite per aiutare il nostro pubblico a compiere scelte più consapevoli nella selezione dei software. Abbiamo testato oltre 2.000 strumenti per diversi casi d’uso in ambito finanziario e contabile e scritto più di 1.000 recensioni dettagliate sui software. Scopri come rimaniamo trasparenti e la nostra metodologia di recensione.

Confronto tra le migliori società di elaborazione carte di credito, fianco a fianco

u003cp data-id=u00229ccf7b55-2ccf-438a-b17d-1fb1a9770666u0022 data-type=u0022quote-blocku0022u003eEcco una tabella pratica che mette a confronto le nostre migliori società di elaborazione carte di credito su prezzi, dettagli sulle prove e punti di forza principali.u003c/pu003e

| Service | Best For | Trial Info | Price | ||

|---|---|---|---|---|---|

| 1 | Ideale per bassi costi di elaborazione carte di credito | Prova gratuita di 3 mesi | Da $79 | Website | |

| 2 | Ideale per le vendite al dettaglio omnicanale | Prova gratuita di 3 giorni | Da $29/mese (fatturazione annuale) | Website | |

| 3 | Ideale per trasparenza sui prezzi e supporto interno | Preventivo gratuito disponibile | Prezzi su richiesta | Website | |

| 4 | Ideale per l'elaborazione di carte di credito a costo 0% | Not available | Da $29/mese | Website | |

| 5 | Ideale per accedere a più processori di pagamento | Consulenza gratuita disponibile | Da $50/ora | Website | |

| 6 | Ideale per la versatilità, con POS incluso | Demo gratuita disponibile | Da 1,86% + $0,08 | Website | |

| 7 | Miglior combinazione di punto vendita e sistemi di pagamento | Prova gratuita di 30 giorni | Da $15/mese e 2,3% + 10¢ | Website | |

| 8 | Ideale per il finanziamento il giorno successivo | Preventivo gratuito disponibile | Prezzo su richiesta | Website | |

| 9 | Ideale per chi vende online a livello globale | Non disponibile | Da 2,9% + 30¢ | Website | |

| 10 | Ideale per aziende B2B | Demo gratuita disponibile | Da $15/mese | Website |

Le migliori società di elaborazione carte di credito, recensite

E ora la parte più interessante. Le recensioni di seguito illustrano funzionalità chiave, punti di forza e debolezze, nonché i prezzi, così da trovare la soluzione davvero adatta alla tua attività.

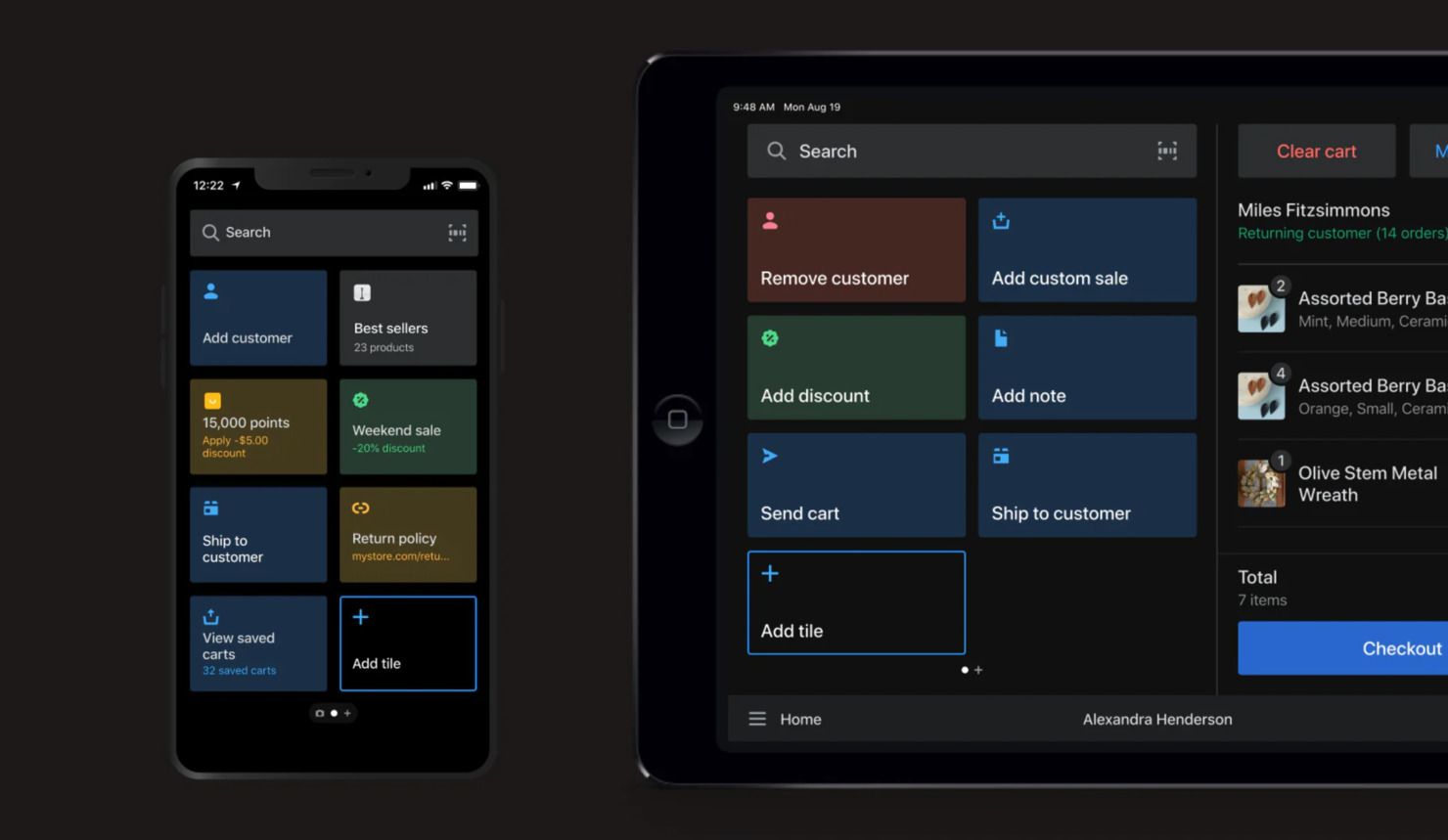

Per i rivenditori di medie dimensioni con un volume significativo, il modello di abbonamento di Payment Depot sostituisce i ricarichi percentuali con una tariffa mensile prevedibile—ottimo quando il valore medio delle vendite è elevato.

Ottieni l'elaborazione interchange-plus, un terminale virtuale per vendite telefoniche o inserite a mano e opzioni mobili per servizio sul marciapiede o eventi. È ideale per commercianti statunitensi che dispongono già di un POS o di una piattaforma ecommerce e desiderano costi di elaborazione più bassi e stabili.

Perché ho scelto Payment Depot

Ho scelto Payment Depot perché permette di controllare i costi delle carte tramite un abbonamento mensile fisso abbinato a tariffe interchange-plus—il risparmio deriva dall’eliminazione dei ricarichi gonfiati.

Offre anche strumenti pratici di vendita: un terminale virtuale per inserire manualmente le carte e inviare fatture, oltre ai pagamenti mobili tramite lettori compatibili per il checkout in movimento. Per la vendita in negozio, puoi utilizzare opzioni hardware largamente supportate, evitando di vincolare il team a dispositivi di nicchia.

I termini mensili riducono i rischi, consentendoti di verificare il risparmio senza un contratto a lungo termine. Se hai già investito in sistemi retail o ecommerce, si integra con gateway e piattaforme familiari per mantenere intatto il tuo flusso di lavoro.

Caratteristiche principali di Payment Depot

Oltre al modello di prezzo, ecco opzioni utili pensate per team di vendita impegnati.

- Terminale virtuale: Inserisci carte, gestisci ordini telefonici o per posta e invia fatture email da un browser.

- Pagamenti mobili: Accetta pagamenti contactless e con chip tramite lettori compatibili per eventi o servizio sul marciapiede.

- Diversi percorsi hardware: Utilizza configurazioni retail comuni (ad es. basate su Clover) per supportare corsie e back office.

- Accettazione di portafogli digitali: Permetti ai clienti di pagare con Apple Pay e Google Pay per un checkout più rapido.

Integrazioni di Payment Depot

Le integrazioni includono Authorize.Net, Shopify, WooCommerce, BigCommerce, Magento, QuickBooks, OpenCart e Zen Cart.

Pros and Cons

Pros:

- Supporta hardware retail comune per flessibilità in negozio.

- Il modello di abbonamento riduce le tariffe effettive a volumi elevati.

- Include un terminale virtuale per pagamenti inseriti manualmente e telefonici.

Cons:

- La tariffa mensile può superare i risparmi per chi vende a basso volume.

- Solo per account commerciante USA; onboarding internazionale non disponibile.

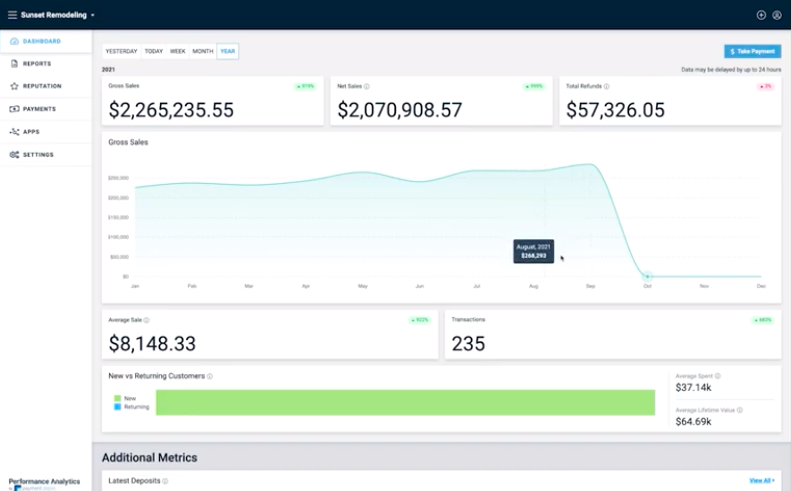

Per i rivenditori omnicanale, Shopify POS collega il checkout in negozio con il catalogo online, l'inventario e i dati dei clienti—così il tuo team non dovrà riconciliare i sistemi a mezzanotte.

Ottieni inoltre l'accettazione delle carte integrata (Shopify Payments) oltre a Tap to Pay su iPhone e Android, che riduce i costi dell'hardware per banchi più piccoli o pop-up. È ideale per i commercianti già su Shopify che vogliono inventario unificato, BOPIS (acquista online, ritira in negozio) e flussi di lavoro semplici per il personale.

Perché ho scelto Shopify POS

Ho scelto Shopify POS perché offre un inventario unificato tra online e vendita al dettaglio: il tuo personale può vendere dallo stock di qualsiasi sede ed evitare sovravendite grazie al tracciamento delle quantità in tempo reale.

Puoi offrire l'opzione acquista online, ritira in negozio tramite POS Pro, così i clienti prenotano online e il tuo team gestisce l'ordine direttamente dalla schermata POS. Tap to Pay su iPhone e Android permette di accettare carte e portafogli contactless senza hardware aggiuntivo, ottimo per eventi o per velocizzare le file.

La schermata principale smart grid velocizza il checkout posizionando prodotti, sconti e app più utilizzati su riquadri che il team può selezionare all'istante. Infine, Shopify Payments integrato significa che depositi, commissioni e report sui pagamenti sono disponibili sulla stessa dashboard già utilizzata dal vostro team finanziario.

Funzionalità principali di Shopify POS

Ecco alcuni strumenti pratici direttamente correlati ai motivi sopra elencati.

- Modelli Smart Grid: Crea e assegna layout di riquadri per ogni sede per accelerare i flussi di lavoro alla cassa.

- Acquista in negozio, spedizione al cliente: Effettua una vendita in uno store e spedisci da un'altra sede con disponibilità di stock.

- Report su inventario e finanze: Monitora vendite, tasse e pagamenti dalla stessa area amministrativa utilizzata quotidianamente dal tuo team.

- Ruoli e permessi dello staff: Limita sconti, rimborsi e visualizzazioni sensibili grazie a controlli di accesso basati sul ruolo.

Integrazioni di Shopify POS

Le integrazioni includono QuickBooks Online, Mailchimp, Klaviyo, LoyaltyLion, Yotpo, ShipStation, UPS, DHL Express e Canada Post.

Pros and Cons

Pros:

- BOPIS e resi in negozio sono integrati nel flusso di lavoro POS.

- Tap to Pay su iPhone/Android riduce i costi dell'hardware per i lettori di carte.

- L'inventario unificato online e in negozio riduce le sovravendite e le mancanze di stock.

Cons:

- La disponibilità di Shopify Payments limita la piena funzionalità in alcuni paesi.

- Si applicano costi aggiuntivi quando si utilizzano gateway di pagamento esterni.

New Product Updates from Shopify POS

Shopify POS Adds Selling Environment Health Dashboard

Shopify POS introduces a unified connectivity screen that shows internet, Shopify service, and hardware connection health in one place. The update helps staff quickly identify issues and take recommended actions to keep sales running. For more information, visit Shopify POS's official site.

.

.

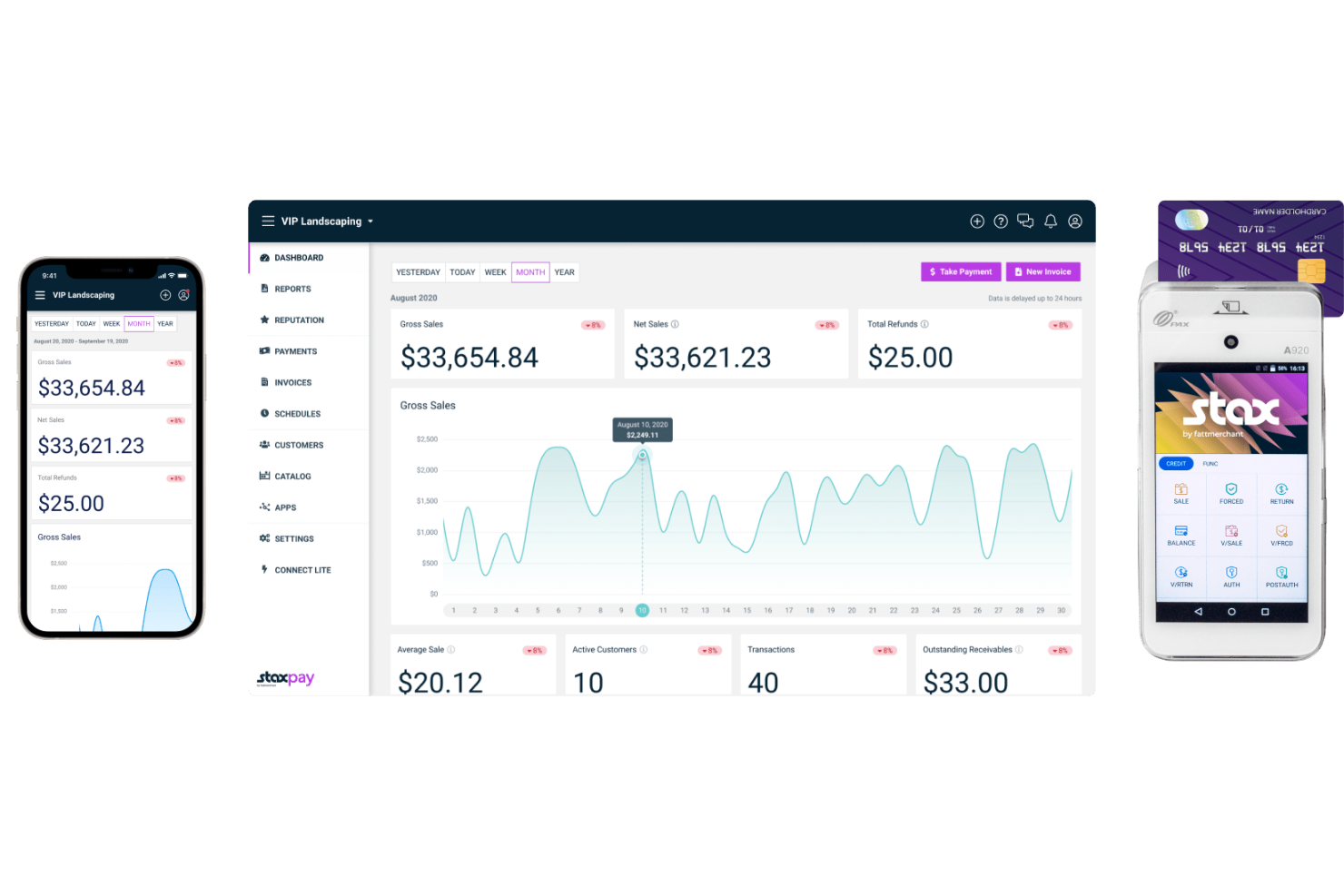

Per i commercianti statunitensi ad alto volume stanchi dei rincari nascosti, il modello di abbonamento di Stax Pay può rendere i costi di elaborazione più prevedibili—soprattutto se il valore medio delle transazioni è elevato.

Include anche il sovrapprezzo automatico tramite CardX per compensare le commissioni delle carte di credito dove consentito dalla legge, oltre a finanziamento il giorno successivo e un terminale virtuale per pagamenti telefonici o tramite fattura.

È ideale per commercianti già affermati e venditori B2B che apprezzano costi prevedibili e necessitano sia di accettazione in presenza sia online.

Perché ho scelto Stax Pay

Ho scelto Stax Pay perché il canone mensile fisso più lo schema interchange offre costi prevedibili su larga scala—i risparmi provengono da commissioni che puoi realmente pianificare.

Puoi inoltre proteggere i margini grazie al sovrapprezzo conforme con CardX, con strumenti di trasparenza e calcoli automatici che ti mantengono in linea con le regole dei circuiti delle carte. Per l’operatività quotidiana, il tuo team dispone di un terminale virtuale per pagamenti digitati e fatturazione, insieme a finanziamento il giorno successivo per migliorare la liquidità.

L’hardware è flessibile—puoi abbinare terminali compatibili per bancone, mobile o ritiro al volo senza vincolarti a un unico produttore. Apprezzo inoltre che sia disponibile ACH come opzione a costi inferiori per le fatture B2B di importo elevato.

Caratteristiche principali di Stax Pay

- Modello di prezzo ad abbonamento: Paga un canone mensile fisso più lo schema interchange per avere costi più prevedibili.

- Sovrapprezzo conforme (CardX): Applica un sovrapprezzo dove consentito con servizi di trasparenza e reportistica inclusi.

- Terminale virtuale e fatturazione: Inserisci manualmente le carte in sicurezza, invia fatture e ricevi pagamenti senza un POS.

- Finanziamento il giorno successivo: Accelera gli accrediti sulle transazioni idonee per fare girare le scorte.

Integrazioni Stax Pay

Le integrazioni includono QuickBooks Online, QuickBooks Desktop, WooCommerce e Magento (Adobe Commerce).

Pros and Cons

Pros:

- Finanziamento il giorno successivo disponibile per accesso più rapido ai fondi regolati.

- Il sovrapprezzo CardX aiuta a compensare i costi delle carte dove consentito dalla legge.

- Il prezzo ad abbonamento favorisce i volumi mensili elevati e transazioni di importo maggiore.

Cons:

- Supporta principalmente commercianti statunitensi; disponibilità globale limitata.

- Il canone mensile può superare i risparmi per le attività a basso volume.

Per i rivenditori che desiderano compensare l'aumento delle commissioni di interscambio senza dover inseguire regole statali variabili, CardX by Stax consente di trasferire le commissioni ammissibili delle carte di credito ai clienti—bloccando automaticamente i supplementi sulle carte di debito.

È una soluzione intelligente per i commercianti statunitensi con vendite in negozio o online che vogliono proteggere i margini e garantire la conformità senza doverla gestire costantemente.

Perché ho scelto CardX by Stax

Ho scelto CardX by Stax perché abbina la protezione dei margini a una reale tecnologia di conformità—consente il rilevamento automatico del tipo di carta, applicando le commissioni solo alle carte di credito e non alle carte di debito, così da rispettare le regole delle reti di carte e dei singoli stati.

Il tuo team riceve subito scontrini e avvisi conformi alle normative, il che significa meno problemi in caso di audit e meno contestazioni al banco.

Per configurazioni omnicanale, puoi accettare pagamenti online, in ufficio o di persona utilizzando la stessa logica dei supplementi, così le politiche restano coerenti su tutti i canali. La disponibilità copre la maggior parte degli Stati Uniti e gli obiettivi di uptime pubblicati sono di livello enterprise, quindi non rischi interruzioni nei fine settimana più impegnativi.

In sintesi: tieni più margine da ogni vendita con carta di credito idonea, supportato da strumenti che fanno rispettare realmente la politica, non solo la promettono.

Caratteristiche principali di CardX by Stax

Oltre alla conformità sui supplementi, ecco strumenti pratici che i rivenditori useranno davvero.

- Rilevamento automatico della debito: Identifica le carte di debito all’inserimento e rimuove automaticamente i supplementi.

- Scontrini e segnaletica conformi: Genera le segnalazioni delle commissioni riga per riga e gli avvisi richiesti per gli audit.

- Accettazione omnicanale: Applica le stesse regole sui supplementi a vendite online, in ufficio e di persona.

- Reportistica e riconciliazione: Monitora il risparmio sulle commissioni, i depositi e le tendenze da una singola dashboard.

Integrazioni di CardX by Stax

Le integrazioni includono Stax Pay, Stax Connect, Stax Bill e Stax Processing.

Pros and Cons

Pros:

- Aiuta a proteggere i margini sulle transazioni con carta di credito idonee su larga scala.

- Le informative sugli scontrini riducono il rischio di non conformità al punto vendita.

- La logica automatica dei supplementi applica le regole su solo credito su tutti i canali.

Cons:

- Le transazioni con carta di debito comportano comunque costi di elaborazione per il commerciante.

- Non disponibile per commercianti in Connecticut o Massachusetts.

Per i rivenditori che desiderano avere leva sui processori—non essere vincolati—Swipesum abbina competenze sulle commissioni a una piattaforma indipendente dal processore.

Riceverai assistenza nell'auditing delle rendicontazioni, nella scelta del processore giusto e nella gestione delle controversie—ideale per team con più sedi, B2B e omnicanale che si preoccupano del costo totale, non solo di una tariffa promozionale.

Perché ho scelto Swipesum

Ho scelto Swipesum perché ti permette di mantenere il controllo—il suo approccio indipendente dal back-end consente di scegliere tra i principali processori senza dover rivoluzionare la tua infrastruttura. Riduci davvero il tuo tasso effettivo tramite audit delle rendicontazioni e controlli periodici sulle tariffe, non con promesse vaghe.

Gestori di account dedicati si occupano delle parti più complesse—negoziazioni, rinnovi e cambi di fornitore—così il tuo team non deve decifrare tabelle di sovrapprezzo alle 22 di sera. Quando superi un provider, puoi cambiarlo restando sempre attraverso il layer Swipesum, riducendo i rischi operativi.

Mi piace anche che supportino ambienti complessi, dal retail + ecommerce alla fatturazione B2B.

Caratteristiche principali di Swipesum

Ecco gli strumenti pratici che assicurano questa flessibilità.

- Monitoraggio delle Commissioni: Usa l'analisi automatica delle rendicontazioni per individuare commissioni gonfiate e variazioni di tariffa prima che aumentino troppo.

- Assistenza nella Gestione dei Chargeback: Offre supporto concreto per identificare le cause, inviare prove e migliorare i tassi di vittoria.

- Configurazione Gateway Gratuita: Imposta un gateway di pagamento per i nuovi utenti, riducendo il tempo prima della prima transazione.

- Supporto Tecnico: Aiuta con integrazioni personalizzate e casi complessi su POS, ERP ed ecommerce.

Integrazioni Swipesum

Le integrazioni includono Shopify, BigCommerce, WooCommerce, Magento, Stripe, Square, Clover, Lightspeed, NetSuite e QuickBooks.

Pros and Cons

Pros:

- Il modello agnostico rispetto ai processori consente di scegliere e cambiare fornitore.

- Gli audit automatici delle rendicontazioni individuano costi nascosti e variazioni delle tariffe.

- Il supporto diretto per i chargeback riduce le perdite e il tempo impiegato dal personale.

Cons:

- Non è indicato se desideri un sistema completamente self-service.

- Le soluzioni personalizzate possono richiedere più tempo per essere implementate.

Per i rivenditori che desiderano tariffe trasparenti interchange-plus senza costi mensili, Helcim offre pagamenti in negozio, online e tramite fattura in un unico posto.

Ottieni un terminale virtuale gratuito, POS integrato con inventario di base, ACH/EFT per pagamenti bancari a basso costo e sovrapprezzo opzionale per proteggere i margini—ideale per commercianti negli Stati Uniti e in Canada che danno valore alla trasparenza dei costi e a strumenti pratici.

Perché ho scelto Helcim

Ho scelto Helcim perché offre una tariffazione interchange-plus con margini basati sui volumi, quindi la tua percentuale effettiva può diminuire man mano che elabori più transazioni. Puoi accettare pagamenti inseriti manualmente, con carta presente e ACH tramite il Terminale Virtuale gratuito, il che aiuta con ordini telefonici e clienti con conto aperto.

Per le vendite in presenza, lo Smart Terminal include un'app POS e la stampa delle ricevute, così il tuo team può effettuare vendite senza bisogno di software aggiuntivi. Se hai bisogno di proteggere i margini sulle carte di credito, Helcim Fee Saver ti permette di abilitare il sovrapprezzo conforme sulle transazioni idonee.

Apprezzo anche che i profili clienti—carte salvate, dettagli ACH memorizzati e fatture precedenti—siano gestiti in un CRM integrato, rendendo più rapide le operazioni ripetute.

Caratteristiche Principali di Helcim

Oltre alle tariffe e ai terminali citati sopra, ecco le funzionalità di pagamento che i team utilizzano realmente ogni giorno.

- Pagine & Link di Pagamento: Crea velocemente pagine di checkout o link ospitati per ricevere pagamenti senza sviluppo personalizzato.

- Fatturazione Ricorrente & Fatturazione: Pianifica abbonamenti, invia fatture e riscuoti automaticamente via carta o ACH.

- Gestione Clienti (Vaulting): Archivia in modo sicuro carte e conti bancari per velocizzare gli addebiti ripetuti.

- Report & Riconciliazione Pagamenti: Tieni traccia di commissioni, depositi e rendiconti per mantenere la contabilità ordinata.

Integrazioni di Helcim

Le integrazioni includono QuickBooks Online, Xero, WooCommerce, Magento 2, Foxy.io, WHMCS e Drupal.

Pros and Cons

Pros:

- Accettare ACH/EFT riduce i costi per B2B, servizi e ordini di alto importo.

- Lo Smart Terminal include app POS e stampa ricevute per vendite al banco.

- Tariffe interchange-plus con sconti sul volume che riducono il costo effettivo nel tempo.

Cons:

- L'interchange-plus può risultare più caro sui micro-pagamenti rispetto ad alcune soluzioni a tariffa fissa.

- Non disponibile per molti settori ad alto rischio; la selezione è conservativa.

Per i rivenditori in crescita che desiderano punto vendita e pagamenti in un unico luogo, Clover abbina hardware da banco a strumenti web realmente utili—terminali virtuali, soluzione mobile e controlli per più sedi.

È l'ideale per negozi piccoli e medi e punti di ristorazione veloce che hanno bisogno di elaborazioni affidabili di persona oggi, oltre a semplici soluzioni per il checkout online e la contabilità domani.

Perché ho scelto Clover

Ho scelto Clover perché permette di gestire le vendite quotidiane—con chip, contactless, inserimento manuale e fatture—mentre il tuo team vede le vendite serali sincronizzate in contabilità, così la riconciliazione non ti ruba le mattine.

Hai a disposizione un terminale virtuale via browser per ordini telefonici, supportato dall’archiviazione tokenizzata delle carte per velocizzare i clienti abituali. L’app mobile ti permette di effettuare vendite e visualizzare i depositi ovunque, utile quando il personale è ridotto.

Per i rivenditori con più sedi, una dashboard centrale invia aggiornamenti su menu, prezzi e tasse a tutti i dispositivi, così i cambiamenti avvengono una sola volta—invece che negozio per negozio. Termini e prezzi sono trasparenti sul sito, e hai supporto telefonico 24/7 quando qualcosa va storto cinque minuti prima della chiusura.

Funzionalità principali di Clover

Oltre a quanto già detto, ecco alcuni strumenti pratici a cui i rivenditori spesso fanno affidamento.

- Terminale Virtuale: Inserisci i pagamenti da qualsiasi browser per ordini telefonici e via posta.

- Depositi Rapidi: Accedi anticipatamente ai fondi idonei, per una piccola commissione, quando la liquidità scarseggia.

- Controlli Multi-Sede: Aggiorna articoli, prezzi e tasse in tutti i negozi da una sola dashboard.

- Gestione delle Dispute: Monitora i chargeback e rispondi con i documenti richiesti dal tuo portale merchant.

Integrazioni di Clover

Le integrazioni includono QuickBooks, Xero, Homebase, Gusto, Shopify, BigCommerce, WooCommerce e Yelp.

Pros and Cons

Pros:

- L'App Market estende il punto vendita a payroll, pianificazione turni e strumenti fiscali.

- Gli aggiornamenti centralizzati su più sedi fanno risparmiare tempo e prevengono incongruenze nei prezzi.

- Il terminale virtuale gestisce gli ordini telefonici senza hardware aggiuntivo.

Cons:

- Prezzi e opzioni dei piani possono risultare complessi per chi acquista per la prima volta.

- Le tariffe per le transazioni online sono più alte rispetto a quelle in presenza.

Per i rivenditori che danno importanza al flusso di cassa, Merchant One dà priorità ai depositi rapidi—finanziamento il giorno successivo per i conti idonei—e offre modi pratici per accettare carte in negozio, online e in mobilità.

È adatto ai commercianti statunitensi che desiderano le opzioni hardware Clover, un terminale virtuale con fatturazione ricorrente e accettazione mobile senza dover ricostruire il proprio POS o stack ecommerce.

Perché ho scelto Merchant One

Ho scelto Merchant One perché consente di proteggere il flusso di cassa tramite finanziamento il giorno successivo, supportato da bonifici batch a livello di processore (verificare scadenze ed eleggibilità).

Include anche un terminale virtuale per pagamenti inseriti manualmente e transazioni card-not-present, compresa la fatturazione ricorrente e la memorizzazione delle carte—utile per abbonamenti o fatturazione. Se hai bisogno di mobilità, puoi accettare pagamenti EMV e contactless tramite lettori supportati come Clover Go o Swift B250.

Per i punti vendita fisici, le opzioni POS di Clover e i terminali da banco coprono chip, contactless e banda magnetica con strumenti dedicati alla sicurezza PCI. L’installazione dedicata e l’assistenza 24/7 aiutano i team meno tecnici a iniziare velocemente senza bisogno di sviluppo personalizzato.

Caratteristiche principali di Merchant One

In aggiunta alla velocità dei fondi e alle opzioni hardware, ecco strumenti che utilizzerai davvero ogni giorno.

- Terminale virtuale e fatturazione ricorrente: Inserisci manualmente i pagamenti e imposta addebiti automatici da un browser sicuro.

- Customer Vault: Conserva le carte dei clienti in sicurezza per acquirenti abituali e checkout più veloci.

- Generatore di fatture e pulsanti Acquista Ora: Invia fatture o aggiungi link di pagamento ospitati senza plugin aggiuntivi.

- Plugin QuickBooks: Sincronizza i depositi e riduci il lavoro manuale di riconciliazione.

Integrazioni di Merchant One

Le integrazioni includono Authorize.net, Payeezy Gateway, Payflow Pro, Paytrace Gateway, USAePay, Aloha, Micros e Maitre’D.

Pros and Cons

Pros:

- Terminale virtuale con fatturazione ricorrente, fatturazione e plugin QuickBooks.

- Opzioni Clover POS più lettori EMV da banco e mobili.

- Finanziamento il giorno successivo disponibile per commercianti idonei per depositi più rapidi.

Cons:

- Prezzi a livelli e commissioni possono risultare poco trasparenti senza tabelle dettagliate.

- Contratti pluriennali e penali di recesso anticipato segnalate dagli utenti.

Per i rivenditori orientati al globale, Stripe elimina le complicazioni dell'accettazione delle carte a livello internazionale: prezzi in multivaluta, alte percentuali di autorizzazione e robusti strumenti antifrode.

È la soluzione ideale per i team che vendono principalmente online e desiderano fatturazione ricorrente, gestione delle fatture e la possibilità di aggiungere pagamenti in presenza senza cambiare processore.

Perché ho scelto Stripe

Ho scelto Stripe perché garantisce alte percentuali di accettazione grazie a funzionalità come Adaptive Acceptance, che ritenta automaticamente le transazioni rifiutate utilizzando segnali informati dall’emittente: trattieni più vendite già concluse.

Puoi avviare nuovi canali rapidamente con Payment Links e Checkout, così il tuo team accetta carte senza dover scrivere codice. Se vendi in negozio, Terminal e Tap to Pay su iPhone rendono i pagamenti in presenza facilmente integrabili, senza bisogno di nuovo gateway o conto commerciante.

La vendita globale è davvero praticabile qui: puoi impostare prezzi in più di 135 valute e ricevere pagamenti nella tua valuta locale, evitando complicazioni di riconciliazione dovute all’accettazione di carte internazionali.

Funzionalità principali di Stripe

Oltre a quanto sopra, ecco alcune funzionalità operative di pagamento che i rivenditori utilizzano realmente.

- Radar Rilevamento Frodi: Valutazione dei rischi basata su ML e regole personalizzabili per bloccare attività fraudolente con le carte.

- Protezione contro i chargeback: Componente aggiuntivo opzionale che copre automaticamente le controversie ammesse sulle carte, limitando le perdite.

- Token di rete e aggiornamento carta: Mantieni aggiornati i dati delle carte e riduci i rifiuti con aggiornamenti automatici delle credenziali.

- Rendicontazione finanziaria e pagamenti: Report unificati, riconciliazione dei depositi e pianificazione dei pagamenti configurabile.

Integrazioni di Stripe

Le integrazioni includono WooCommerce, Squarespace, Wix, BigCommerce, Salesforce, NetSuite, Xero, DocuSign e Mailchimp.

Pros and Cons

Pros:

- Aggiungi le vendite in presenza tramite Terminal e Tap to Pay senza cambiare gateway.

- Adaptive Acceptance e i token di rete migliorano i tassi di autorizzazione delle carte.

- Accettazione di carte a livello globale con oltre 135 valute e metodi locali.

Cons:

- Il prezzo a tariffa fissa può risultare costoso per i rivenditori con alti volumi e vendita in presenza.

- Non disponibile per i commercianti in alcuni paesi (es. Cina).

Per i team B2B che lavorano all'interno di un ERP, EBizCharge elimina le attività ripetitive legate ai pagamenti: il personale può gestire carte e bonifici ACH direttamente dove emette le fatture, e i pagamenti vengono contabilizzati automaticamente.

È ideale per aziende statunitensi e canadesi che desiderano strumenti di gestione crediti come link di pagamento e un portale clienti collegati direttamente alla contabilità, con risparmi Level 2/3 per carte aziendali.

Perché ho scelto EBizCharge

Ho scelto EBizCharge perché consente di accettare carte e ACH direttamente in sistemi come NetSuite, Acumatica, QuickBooks, Sage e Dynamics: i pagamenti vengono applicati alle fatture e aggiornano i crediti senza esportazioni manuali.

Ricevi inoltre strumenti pratici per l'AR: collegamenti di pagamento via email, un portale clienti personalizzato e pagine di checkout ospitate che ti permettono di incassare più velocemente senza sviluppo su misura. Per il B2B, supporta dati Level 2/3 così le transazioni qualificanti hanno costi di interscambio minori, aspetto importante per importi elevati.

La sicurezza è gestita tramite tokenizzazione e 3D Secure, così puoi memorizzare le carte riducendo il rischio. Se serve tutelare il margine, il modulo di surcharging integrato rileva i pagamenti con carta di debito e applica commissioni solo alle transazioni di credito idonee.

EBizCharge: Caratteristiche principali

Ecco alcune funzionalità extra che si integrano perfettamente al flusso di lavoro nativo ERP.

- Checkout ospitati: Lancia pagine di pagamento personalizzate e conformi PCI per ricevere pagamenti online senza programmare.

- Terminale virtuale: Inserisci ordini telefonici e postali dal browser, collegati a fatture e ordini di vendita.

- Report avanzati: Cerca ed esporta dati delle transazioni per riconciliare gli incassi e monitorare i chargeback.

- Programma di Surcharge: Applica automaticamente commissioni di carta di credito conformi e blocca quelle di debito dal sovrapprezzo.

Integrazioni EBizCharge

Le integrazioni includono Acumatica, NetSuite, QuickBooks Desktop, QuickBooks Online, Microsoft Dynamics 365 Business Central, Sage 100, SAP Business One, Salesforce, Magento e BigCommerce.

Pros and Cons

Pros:

- Il supporto Level 2/3 riduce le commissioni di interscambio sulle transazioni B2B idonee.

- Il portale clienti con carte memorizzate accelera l'incasso e riduce il DSO.

- Registra automaticamente i pagamenti nell'A/R dell'ERP — meno lavoro di riconciliazione.

Cons:

- Il surcharging si applica solo al credito; le transazioni di debito restano soggette a commissioni.

- Prezzo su preventivo — nessuna tariffa pubblica per un confronto rapido.

Altre società di elaborazione carte di credito

u003cp data-id=u002274edfb36-2a3f-4654-b601-a1f0f16165afu0022 data-type=u0022quote-blocku0022u003eEcco alcune altre società di elaborazione carte di credito che non sono entrate nella mia lista principale, ma che meritano comunque attenzione:u003c/pu003e

- Podium

Ideale per le imprese artigiane locali

- ProMerchant

Ideale per la protezione antifrode avanzata

- Square Online

Ideale per l'elaborazione dei pagamenti ecommerce

- Payline Data

Ideale per accordi mensili

- Dharma Merchant Services

La scelta migliore per la flessibilità POS

- Chase

Migliore soluzione finanziaria tutto-in-uno

- Flagship Merchant Services

Ideale per piccoli rivenditori

- STAX

Ideale per venditori ad alto volume

- QuickBooks Online

Ideale per utenti QuickBooks

{kind=link}

I nostri criteri di selezione per le società di elaborazione carte di credito

Quando si tratta di classificare le migliori società di elaborazione carte di credito, le valuto secondo gli stessi standard che applicherei alle mie attività. Ecco come ho analizzato ogni fornitore:

Servizi principali (25% del punteggio totale)

Ogni fornitore in questa lista doveva coprire perfettamente le basi—senza eccezioni.

- Deve offrire un gateway di pagamento affidabile per transazioni online sicure.

- Fornire sistemi POS robusti per pagamenti di persona.

- Aprire conti commerciante senza complicazioni o ritardi.

- Includere una forte protezione antifrode come requisito imprescindibile.

- Offrire strumenti di reportistica e analisi per la massima trasparenza.

Servizi aggiuntivi distintivi (25% del punteggio totale)

Per distinguere i buoni dai veri migliori, ho cercato fornitori che offrissero qualcosa in più.

- Offrire soluzioni di pagamento mobile per vendite in movimento.

- Supportare l’elaborazione di pagamenti internazionali per attività transfrontaliere.

- Fornire sicurezza avanzata dei dati oltre gli standard minimi di settore.

- Consentire la personalizzazione delle soluzioni di pagamento per adattarsi a esigenze particolari.

- Integrarsi perfettamente con piattaforme e strumenti ecommerce.

Esperienza nel settore (10% del punteggio totale)

Vuoi un partner solido e duraturo, non una meteora.

- Anni di attività che dimostrano stabilità.

- Un’ampia base clienti indica una diffusa adozione.

- Il possesso di certificazioni di settore accresce la fiducia.

- Solide partnership con istituzioni finanziarie testimoniano credibilità.

- Una storia costante di innovazione.

Onboarding (10% del punteggio totale)

Un processo di onboarding fluido può determinare il successo o il fallimento dei primi mesi con un fornitore.

- La configurazione dell’account dovrebbe essere rapida e intuitiva.

- Le risorse formative devono essere disponibili e utili.

- Il supporto pratico deve guidare i nuovi clienti.

- Un tempo rapido alla prima transazione è fondamentale.

- Un’interfaccia intuitiva riduce le difficoltà.

Assistenza clienti (10% del punteggio totale)

L’assistenza è la tua rete di sicurezza—ecco cosa conta di più.

- La disponibilità 24/7 garantisce aiuto quando ne hai bisogno.

- La possibilità di contattare il supporto tramite diversi canali (telefono, chat, email) è importante.

- I tempi di risposta rapidi prevengono interruzioni delle attività.

- Personale con competenze tecniche reali, non solo lettori di script.

- Recensioni costantemente positive sul servizio clienti.

Rapporto qualità-prezzo (10% del punteggio totale)

Mi interessa il ROI—ed è lo stesso per te.

- Prezzi trasparenti e chiari—nessuna sorpresa.

- Commissioni competitive che non erodono i margini.

- Nessun costo nascosto scritto in piccolo.

- Sconti sul volume per aziende con alti volumi di transazioni.

- Chiaro ritorno sull’investimento.

Recensioni dei clienti (10% del punteggio totale)

Niente batte il feedback di utenti reali.

- I punteggi di soddisfazione generale raccontano la storia.

- I commenti su affidabilità e tempi di attività sono fondamentali.

- I feedback sinceri sull’assistenza sono importanti.

- Resoconti concreti sulla facilità d’uso.

- Percezione del valore rispetto al prezzo pagato.

Cosa Sono le Società di Elaborazione Carte di Credito?

Le società di elaborazione carte di credito sono fornitori che gestiscono i pagamenti elettronici per le aziende, abilitando transazioni sicure e in tempo reale con carte di credito e di debito.

Le loro piattaforme si occupano di tutto: dall’accettazione dei pagamenti in negozio e online, alla protezione contro le frodi e al rispetto degli standard di sicurezza.

La maggior parte delle aziende si affida a queste società per snellire la fase di pagamento, ridurre gli errori manuali e offrire ai clienti un’esperienza di acquisto fluida. Casi d’uso comuni includono negozi al dettaglio che necessitano di sistemi POS robusti, attività ecommerce che cercano integrazioni semplici con i gateway di pagamento e fornitori di servizi che vogliono strumenti per l’addebito ricorrente.

Scegliendo il processore giusto, le aziende possono aumentare la soddisfazione dei clienti, ridurre i rischi nei pagamenti e ricevere il denaro più rapidamente—il tutto rimanendo conformi ai requisiti del settore.

Come Scegliere una Società di Elaborazione Carte di Credito

È facile perdersi tra caratteristiche e tariffe. Ecco una tabella di riferimento rapido per aiutarti a concentrarti su ciò che conta davvero quando restringi la tua shortlist:

| Azione | Cosa fare/considerare |

|---|---|

| Identifica le esigenze aziendali | Elenca le funzionalità necessarie come POS, pagamenti da mobile, fatturazione ricorrente |

| Analizza le strutture tariffarie | Esamina tutte le commissioni, i termini contrattuali e i possibili sconti sul volume |

| Conferma l’integrazione | Assicurati della compatibilità con ecommerce, contabilità o piattaforme POS |

| Verifica gli standard di sicurezza | Cerca la conformità PCI e la protezione antifrode avanzata |

| Valuta il supporto clienti | Valuta i tempi di risposta e la competenza attraverso interazioni reali |

| Controlla il feedback dei clienti | Dai priorità ai fornitori con elevata affidabilità e soddisfazione del cliente |

Consiglio pro: Prima di firmare, chiedi un preventivo personalizzato e fatti spiegare dal fornitore ogni dettaglio del contratto, punto per punto.

Servizi Chiave delle Società di Elaborazione Carte di Credito

Ogni processore di alto livello dovrebbe includere questi servizi, indipendentemente dalle dimensioni o dal settore della tua azienda:

- Integrazione del gateway di pagamento. Collega il tuo sito web o app alle reti di pagamento per vendite online senza intoppi.

- Rilevamento e prevenzione delle frodi. Utilizza il monitoraggio in tempo reale per individuare e fermare transazioni sospette prima che ti costino.

- Elaborazione pagamenti da mobile. Ti permette di accettare pagamenti da smartphone e tablet—ovunque concludi un affare.

- Soluzioni POS (point-of-sale). Fornisce hardware e software per gestire i pagamenti in negozio e le vendite sul posto.

- Fatturazione e addebiti ricorrenti. Automatizza i pagamenti regolari e gli addebiti in abbonamento per mantenere costante il flusso di entrate.

- Gestione multi-valuta. Accetta pagamenti da clienti internazionali nella loro valuta locale, senza complicazioni.

- Assistenza clienti. Ti offre accesso diretto all'aiuto e al supporto tecnico quando qualcosa si rompe.

- Analisi e report dei dati. Analizza le vendite e i dati dei clienti così sai cosa funziona—e cosa no.

- Gestione dei chargeback. Ti aiuta a tracciare, contestare e risolvere i chargeback per proteggere i tuoi introiti.

- Strumenti di conformità alla sicurezza. Mantiene la tua attività allineata con PCI DSS e le normative di settore, riducendo i rischi.

Vantaggi delle società di elaborazione carte di credito

Ecco cosa fa davvero la differenza quando utilizzi il processore giusto:

- Maggiore volume di vendite. Accettare carte ti permette di raggiungere clienti che non vogliono usare contanti o assegni.

- Flusso di cassa più rapido. Vieni pagato velocemente—di solito entro uno o due giorni—anziché inseguire fatture per settimane.

- Clienti più soddisfatti. Più opzioni di pagamento al checkout equivalgono a meno carrelli abbandonati e clienti scontenti.

- Rischio di frode ridotto. I processori affidabili offrono veri strumenti di sicurezza che tengono lontani i truffatori e riducono i chargeback.

- Decisioni aziendali più intelligenti. Ottieni dati e report sulle transazioni che ti aiutano davvero a pianificare, non solo a guardare i fogli di calcolo.

- Assistenza affidabile. Quando qualcosa si rompe (succede), hai un team pronto a risolvere—senza inutili attese al telefono.

Costi e strutture di prezzo delle società di elaborazione carte di credito

Nessun processore applica la stessa tariffa—e se lo dichiara, probabilmente ti sfugge qualcosa scritto in piccolo. Ecco come si presentano i principali modelli di prezzo:

| Struttura dei prezzi | Come funziona |

|---|---|

| Tariffa fissa | Paga una percentuale unica e fissa per ogni transazione—semplice e prevedibile |

| Prezzi a scaglioni | Le tariffe variano in base al tipo di transazione; paghi commissioni diverse per carte "qualificate" e "non qualificate" |

| Interchange plus | Paghi la commissione della rete della carta più un ricarico trasparente del processore |

| Prezzo in abbonamento | Una quota mensile più piccoli costi per transazione—spesso più conveniente per chi gestisce tanti incassi |

| Prezzi misti | Combina elementi di vari modelli per adattarsi a esigenze di vendita complesse o variegate |

Fattori chiave che influenzano il prezzo

Nel conto mensile incide ben più della sola tariffa. Ecco cos’altro può cambiare sensibilmente i costi:

- Requisiti hardware e software incidono. Sistemi POS speciali o integrazioni specifiche significano spesso costi aggiuntivi.

- Il volume delle transazioni influisce sulle tariffe. Più processi, più puoi contrattare costi più bassi.

- Il livello di rischio del settore può aumentare i costi. Le aziende ad alto rischio (come viaggi, cannabis, adult) di solito pagano di più.

- Il tipo di carta fa la differenza. Carte aziendali e con premi comportano normalmente commissioni di interscambio maggiori rispetto alle carte di debito.

- I metodi di pagamento hanno prezzi diversi. Le transazioni online sono spesso più rischiose (e costose) rispetto ai pagamenti in presenza.

- La durata del contratto può fissare i prezzi—o farti restare bloccato. Contratti a lungo termine talvolta prevedono tariffe più basse, ma attenzione alle penali di uscita.

- La storia dei chargeback influisce sulla tua reputazione. Troppi chargeback possono far salire le tariffe o causare l’esclusione dal servizio.

Domande frequenti sulle società di elaborazione delle carte di credito

Stai ancora cercando di capire come funziona l’elaborazione delle carte di credito? Ecco le risposte ad alcune delle domande più comuni.

Quanto costa in genere una commissione per l'elaborazione delle carte di credito?

Aspettati di pagare tra l’1% e il 4% per ogni pagamento con carta. Questa percentuale copre elaborazione, interchange, assessment e talvolta una commissione per ogni passaggio (pensate da 5 a 50 centesimi). Le vendite online solitamente costano di più rispetto ai pagamenti con chip e pin. Se vedi tariffe al di fuori di questo intervallo, dovresti pensare a negoziare—o anche cambiare processore.

Come posso ridurre le commissioni di elaborazione delle carte di credito per il mio negozio?

Inizia comprendendo il tuo estratto conto. Poi chiedi al tuo processore se hai diritto a tariffe più basse o a una riduzione delle commissioni di interchange, specialmente se il valore medio degli scontrini o il volume delle vendite è alto. Le carte di debito di solito costano meno delle carte di credito.rnrnL’aggiornamento delle apparecchiature può ripagarsi da solo se spinge più clienti a utilizzare carte chip o pagamenti contactless, che spesso comportano commissioni inferiori. Puoi anche trasferire le commissioni ai clienti in alcuni stati, ma verifica prima le regole.

Che attrezzatura serve per i pagamenti con carta di credito in negozio?

Avrai bisogno di un terminale di pagamento conforme allo standard PCI—qualcosa che legga chip, strisciate e, idealmente, che accetti pagamenti contactless (Apple Pay, Google Pay). La maggior parte dei negozianti abbina questo terminale a un sistema POS che si interfaccia con il processore.rnrnSe gestisci un temporary shop o uno stand mobile, puoi cavartela con uno smartphone e un buon lettore di carte, ma non risparmiare sull’hardware. Fermarsi durante l’ora di punta non vale i pochi euro risparmiati.

Cos'è un payment service provider e conviene ai negozi?

Considera i payment service provider come l’opzione ‘plug-and-play’: ti iscrivi e sei attivo in poche ore, condividendo un gigantesco conto merchant con migliaia di altri negozianti.rnrnMarchi che conosci: Square, PayPal, Stripe. Configurazione rapida, tariffe fisse, meno burocrazia. Il lato negativo? Possono bloccare i conti al minimo sospetto, impongono limiti mensili e pagherai un extra per ogni transazione rispetto a un contratto personalizzato.

Posso usare il mio attuale sistema POS con un nuovo processore di pagamento?

A volte. Molti sistemi POS sono vincolati a un unico processore (soprattutto quelli ‘omaggiati’), ma alcuni sono compatibili con più processori. Prima di cambiare, chiedi sia al fornitore del POS sia al nuovo processore informazioni sull’integrazione. Un aggiornamento può essere una seccatura, ma rimanere bloccati in un pessimo contratto per anni lo è ancora di più.

Quanto tempo serve per ricevere i fondi sul mio conto?

La maggior parte delle società liquida il batch entro 1–3 giorni lavorativi. Alcune offrono accrediti in giornata, ma dovrai pagare per questo privilegio—come se ti prestassero i tuoi stessi soldi.rnrnChiedi sempre quali sono gli orari limite per l’accredito; perdere il batch per cinque minuti può significare aspettare un giorno in più. Tieni conto delle scadenze, come la data dell’affitto. Organizzati di conseguenza.

Come influisce la conformità PCI sul mio negozio?

La conformità PCI non è solo un fastidio tecnologico: tiene i dati delle carte dei tuoi clienti lontani dal dark web. Se accetti pagamenti con carte, ne sei responsabile, punto.rnrnLa maggior parte dei terminali e sistemi POS moderni incorpora le basi, ma devi comunque compilare la documentazione annuale e correggere tutto ciò che viene segnalato dal provider. Se trascuri questi aspetti, rischi multe, cause legali e guai di reputazione. Noioso, ma essenziale.

Scegli il miglior processore

Trovare il giusto processore per carte di credito non è scienza spaziale, ma può sembrare un appuntamento al buio: tante opzioni, mille clausole e solo poche meritano una richiamata.

Scegli con criterio e ottimizzerai i pagamenti, tratterrai più guadagni e semplificherai la vita a te, al tuo team e ai clienti. Se invece ti accontenti, passerai più tempo a combattere contro le commissioni e a risolvere problemi che a far crescere davvero la tua attività.

Il retail non si ferma mai—e nemmeno tu dovresti. Iscriviti alla nostra newsletter per ricevere gli ultimi approfondimenti, strategie e risorse carriera dai principali leader del settore retail.